“With its shares trading at a huge discount to their tangible net asset value (TNAV), it is easy to see why the board of Standard Chartered may be considering a share buyback, according to newspaper reports,” says Russ Mould, AJ Bell investment director.

“Among the UK’s Big Five banks, only Barclays trades at a lower multiple of net asset value, or book, value and continued debate over the long-term merits of its investment banking operations make that understandable.

“To judge whether a share buy-back truly makes sense for shareholders, they can apply the two tests once outlined by legendary investor Warren Buffett, whose Berkshire Hathaway investment vehicle has bought back just under $1 billion of its own shares so far this year, the first such move for several years.

“In his 2012 Letter to Shareholders, the Sage of Omaha wrote:

“Charlie [Munger] and I favour repurchases when two conditions are met: first, a company has ample funds to take care of the operational liquidity and needs of its business; second, its stock is selling at a material discount to the company's intrinsic business value, conservatively calculated.”

“The big discount to book value may well mean Standard Chartered passes the second test, providing investors do not fear another global recession or debt bust is just around the corner.

|

|

2018E |

|||

|

|

P/E |

Price/book |

Dividend yield |

Dividend cover |

|

HBSC |

11.7 x |

1.26 x |

6.1% |

1.4 x |

|

Lloyds |

7.3 x |

1.07 x |

5.9% |

2.3 x |

|

Royal Bank of Scotland |

7.6 x |

0.74 x |

3.2% |

4.1 x |

|

Standard Chartered |

11.4 x |

0.64 x |

2.7% |

3.3 x |

|

Barclays |

7.5 x |

0.63 x |

3.9% |

3.4 x |

Source: Consensus analysts’ forecasts for earnings and dividends, Digital Look, company accounts for historic book value per share figures, Refinitiv data

“The issue of whether Standard Chartered’s putative share buyback makes sense from a strategic point of view is less clear.

“Management will argue that a common equity tier one (CET1) ratio of 14.5% means it has ample capital buffers on its balance sheet should there be an unexpected economic downturn in its key markets, since Article 92 of the (European) Capital Requirement Regulations stipulate that a 4.5% CET1 ratio is required by the end of 2019.

“However, shareholders may be wise to point out to them that the financial markets are becoming more wary of buybacks for two reasons.

“First, markets’ faith in the synchronised global recovery seems to be ebbing again, judging by the autumn volatility.

“Second, there is little evidence that even huge buybacks have done share prices any good and gathering commentary that they have done harm. GE and IBM have lavished tens of billions on dollars on share buybacks without helping their share price at all and GE is now in crisis-management mode as it tries to cope with the debts it has accumulated to fund the buybacks.

“Standard Chartered would at least be buying its shares after they have fallen to levels that look cheap, unlike GE and IBM which seemed to buy stock irrespective of price or valuation, and the bank is unlikely to pile up debt to fund any scheme.

“But even Lloyds and HSBC have seen little share price benefit result from their share buyback programmes over the past year.

Source: Refinitiv data

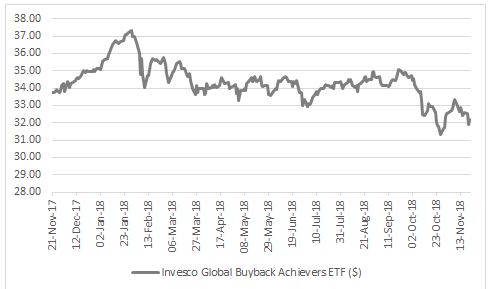

“In addition, the London-listed exchange-traded fund (ETF) which is dedicated to tracking a basket of companies who are carrying out buybacks, the Invesco Markets Global Buyback Achieve ETF, has been a poor performer of late.

Source: Refinitiv data

“This suggests that investors are approaching buybacks with a more critical eye.

“If Standard Chartered does take the plunge, it shareholders will be quite within their rights to ask whether the cash would not be better used to invest in the business and grow long-term earnings through the patient development of the business rather than short-term financial engineering.”