• Chancellor Rishi Sunak will reportedly set out plans to scrap the much-criticised Retail Prices Index (RPI) inflation measure in tomorrow’s spending review

• RPI could be phased out between 2025 and 2030, and replaced with alternative Consumer Prices Index measure (CPIH)

• Insurers have previously estimated the move could wipe £122 billion from the value of Brits’ pensions and investments

• Investors in index-linked gilts, defined benefit pension (DB) scheme members and annuity holders could be among those hit if RPI is abolished; while those with student loans and rail passengers stand to benefit

Tom Selby, senior analyst at AJ Bell, comments:

“Proposals to abolish the RPI inflation measure have barely created a ripple in 2020 but risk causing colossal damage to people’s pensions and investments. This is because, as things stand, RPI-linked increases are written into millions of financial services contracts.

“There are, for example, defined benefit (DB) schemes where scheme rules require members’ retirement incomes to rise in line with RPI.

“Annuities have also been sold on the promise of RPI protection, while index-linked gilts, which are held by huge numbers of investors either individually or via their pensions, are also pegged to RPI inflation.

“If these contracts are to effectively be torn up and RPI replaced with CPIH, millions of savers and investors stand to lose out as a result.”

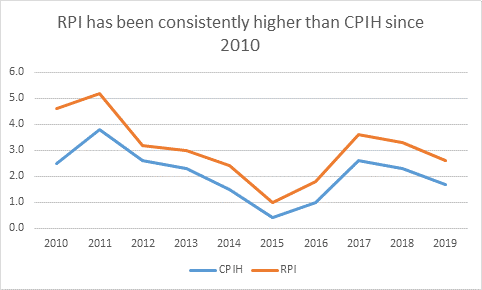

RPI to CPIH: the £122 billion index switch

“Because CPIH tends to be around 0.8 percentage point lower than RPI, over time investments or pension incomes linked to CPIH will grow more slowly than they would if they were linked to RPI.

“Estimates published earlier this year by the Association of British Insurers (ABI) suggest the overall negative impact of a switch from RPI to CPIH could be somewhere north of £100 billion. The hit would not come overnight, however, but rather through a slow grinding down of the real value of people’s pensions and investments.

“The key question now is whether the Chancellor will provide any sort of easement to protect existing contracts. One option would be for the ONS to keep publishing RPI so companies can continue to honour contracts written prior to the change.”

Winners and losers

“Ditching RPI could be good news for some young people and commuters, however. The Government has doggedly, and some would say cynically, continued to link things like rail fare increases and student loan repayments to RPI, ensuring a quiet and creeping boost to Treasury coffers.

“Conversely, the state pension, benefit payments and tax thresholds have been linked to the lower CPI measure, leading to accusations of ‘index shopping’ by successive administrations.

“Moving away from RPI to CPIH could precipitate an end to this approach and provide a much-needed boost for indebted students and rail passengers.”

How swapping RPI with CPIH could affect someone with a £20,000 a year pension

“The impact of linking people’s retirement incomes to a lower inflation measure will be felt over the course of decades.

“Take someone who has a £20,000 annual pension which is linked to RPI. Over the course of a 30-year retirement, if RPI rose by 2.8% a year they would have received a total income of £947,000.

“However, if instead it rose in line with CPIH at 2%, over the same 30-year retirement they would receive total income of roughly £828,000.

“This means a simple switch from RPI to CPIH could cost someone in this position £119,000 in lost retirement income.”

Source: ONS