“A surge in the yield on the US 10-year Treasury to 3.2%, their highest level since 2011, is understandable for three reasons, says Russ Mould, AJ Bell investment director:

1. The American economy seems to be booming

2. The US Federal Reserve is raising interest rates and unwinding Quantitative Easing (which removes a natural, large buyer of US Government bonds)

3. The Trump tax cuts are, in the short-term at least, taking the US annual budget deficit back towards $1 trillion a year, or some 5% of GDP (way beyond the 2.4% figure that is causing such a fuss in Italy right now)

“Investors must now ask themselves three questions:

• Is the bond bull market that dates back to the early 1980s finally over?

• Are the surge in US Treasury yields and rising interest rates a threat to the US economic upturn?

• Is the rise in US government bond yields a threat to the global equity bull market?

Game over for Government bonds?

US 10-year Treasuries have fallen in price by 16% since yields bottomed (and prices peaked) two-and-half years ago, inflicting nasty capital losses on anyone who bought then. Technical analysts may also argue that the chart for the US 2 and 10-year Treasury yields shows that a longstanding downtrend has been broken.

Source: Thomson Reuters Datastream

Unemployment is low, wage growth is picking up and the US Federal Reserve appears to be planning one more interest rate increase for 2018 and three more for 2019. That would take the Fed Funds rate to 3.25%, a fraction above where the benchmark 10-year yield is now.

But Treasury yields are by no means certain to surge.

It may be that the prospect of a 2.8% yield over two years, and around 3.2% over 10, to be received in the world’s reserve currency, the dollar, which itself is rising in value, starts to appeal to more risk-averse investors and for that matter pension funds with liabilities to meet.

Game over for the US economy?

Increases in US interest rates have dragged the benchmark US 30-year mortgage rate to 4.72%, the highest mark since summer 2011, just when oil prices have surged, to further squeeze consumers’ spending power.

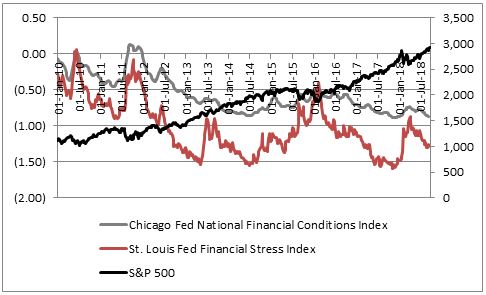

However, this is not showing up yet in the indicators of consumer or corporate confidence, or two other indicators of American financial health, the Chicago Fed’s National Financial Conditions index and the St. Louis Fed’s Financial Stress index.

If increased borrowing costs for consumers and corporations do start to create problems it should show up in these indicators fairly quickly.

Source: Thomson Reuters Datastream, FRED – St. Louis Federal Reserve database

The good news is that neither reading has followed through on a spike seen this year in Spring.

In the past a score of 0.00 on the National Financial Conditions index and a reading of 1.00 on the St. Louis Fed’s indicator have warned of trouble ahead for stocks, compared to the latest readings of -0.87 and -1.29, so there is no sign (yet) of a spill-over from rising rates into the US economy and thus corporate earnings.

Game over for global equities?

Equity market accidents tend to happen when interest rates are rising (as now), valuations are full (which remains a matter of furious debate) and earnings and the economy disappoint.

There is no sign of the later thankfully, although the upcoming third-quarter earnings season in the USA will be a key test. Throughout the first half of the year, earnings estimates continued to rise, which is usually a positive sign, although it is noticeable how the forecast for Q4 2018 has just started to flatten out, a trend which must be watched:

|

|

Dec-17 |

Mar-18 |

Jun-18 |

Sep-18 |

Change in 2018 |

|

EPS estimate for Q2 2018 |

$ 33.97 |

$ 35.64 |

$ 36.54 |

$ 38.65 |

13.8% |

|

EPS estimate for Q3 2018 |

$ 35.95 |

$ 38.49 |

$ 38.65 |

$ 40.05 |

11.4% |

|

EPS estimate for Q4 2018 |

$ 38.51 |

$ 41.84 |

$ 42.16 |

$ 42.14 |

9.4% |

Source: Standard & Poor’s Research

If earnings momentum peters out then there could be trouble ahead, especially if the prospect of a 3.2% yield in dollars from the US Government starts to persuade investors to reduce their allocation to the riskier option of equities in search of yield and capital gain at the same time.

It is by no means certain that the bond and equity bull runs are over. But this shift in the momentum in US 10-year Treasury yields could be heralding a change in the market’s mood music. We have already seen risky areas such as cryptocurrencies, low-volatility strategies and emerging markets blow up in 2018 and this may be a subtle indication of a decrease in investor risk appetite and a growing preference for assets that are perceived to be safer, such as developed market equities and companies with either strong earnings momentum, sound finances and a well-covered dividend yield (or even all three).

There are few signs of out-and-out risk aversion (such as a dash into defensive stocks, bonds or cash) but investors must stay alert, especially if Government bond yields keep rising (and therefore prices keep falling), especially after a near-decade long bull in most asset classes.”