Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBurford Capital reveals surge in earnings

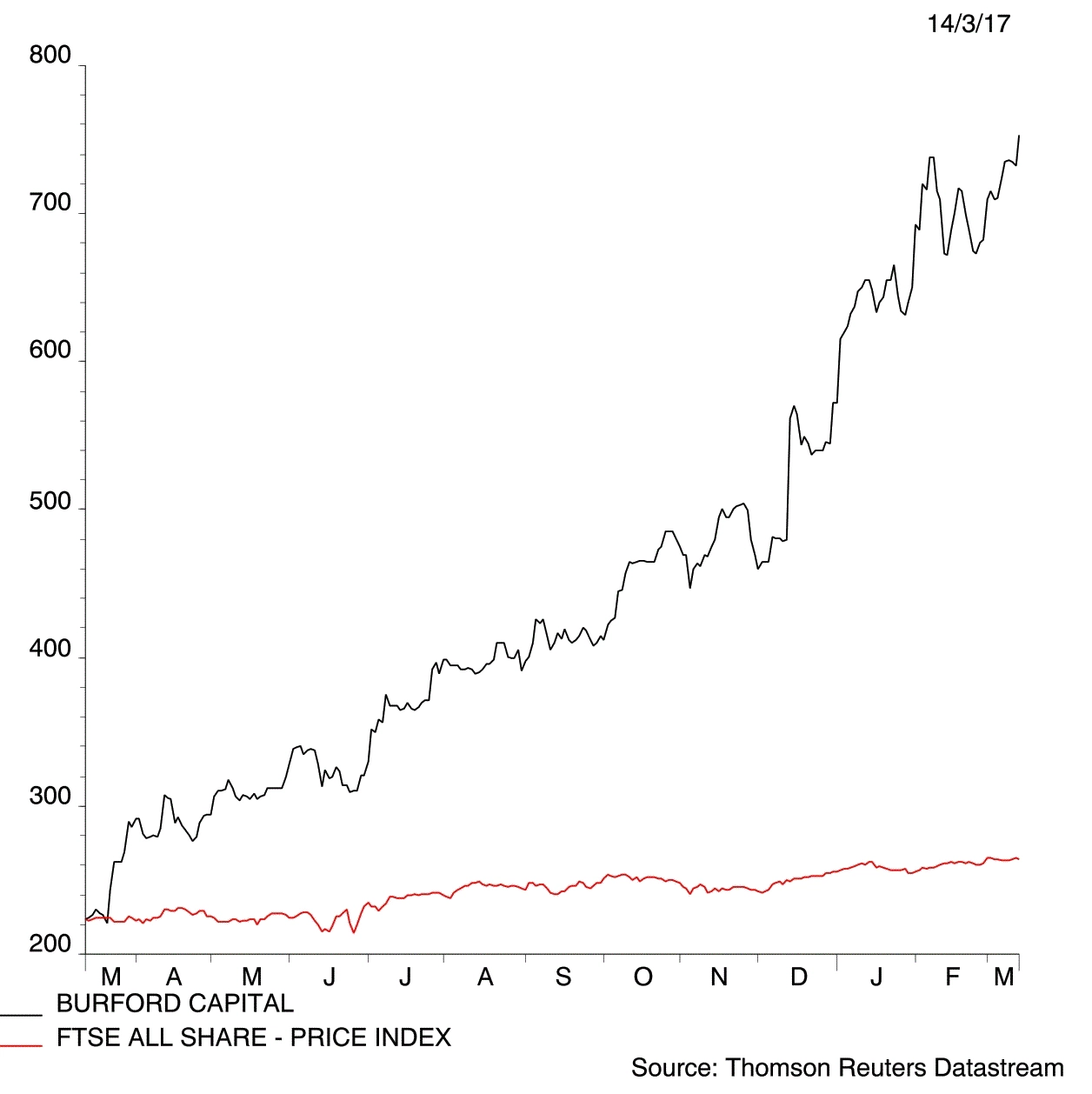

Burford Capital (BUR:AIM) 782p

Gain to date: 6.5%

Original entry point: 734p, 9 March 2017

Our positive call on litigation finance provider Burford Capital (BUR:AIM) is off to a good start as the company reports an extremely strong set of 2016 results (14 Mar 2017).

Revenue is up nearly 60% to $162.9m and adjusted earnings per share gains 78% to 56c. The dividend is hiked 14% to 9.15c but this translates into a 38% increase in sterling terms.

Alongside the results themselves Burford announces a further sale of its interest in the Petersen V Argentina case – litigation involving Spanish investment group Petersen which faced insolvency after the Argentine government summarily renationalised oil company YPF.

The company has now sold 10% of its interest in the case for $40m, which implies a total market value for its investment of $400m or 20 times what it initially put in.

The transaction leads N+1 Singer to upgrade 2017 earnings per share expectations by 43% to 63.3 cents. This implies a forward price-to-earnings ratio of 15 times which does not seem overly expensive for such a unique business.

The big upgrade from Singer reflects the inherent unpredictability of earnings which is an ongoing risk investors need to consider.

We remain comfortable with our bullish stance. Keep buying at 782p. (TS)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

Editor's View

Funds

Great Ideas

Great Ideas Update

Investment Trusts

Larger Companies

Main Feature

Smaller Companies

Story In Numbers

- AIM Stocks Ranking

- UK Pharma & Biotech Stocks

- Esure escapes Ogden damage

- 3-month low: Oil slips as US activity ramps up

- 7.9%: Investment trust’s big bet on Sports Direct

- 76%: Percentage of money going into European tech firms by US and Asian investors

- 25%: Ramsdens on the rise

- 500 tonnes: Morrisons is in good shape