Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineLook to January for clues on the coming year’s stock market performance

There is a saying that a good start in January means the year as a whole is likely to see positive returns.

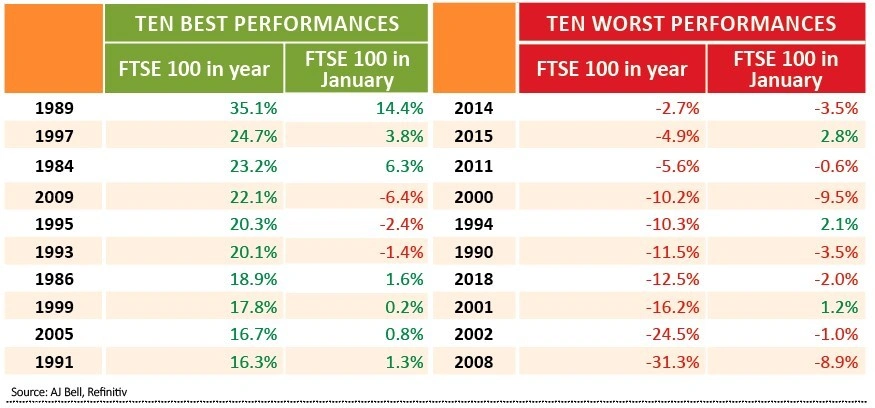

Looking at the history of the FTSE 100 since its inception in 1984, seven of the index’s 10 best years came when it got off to a flyer in January and seven of its 10 worst showings came after a drop in the first month of the year.

Investors could be forgiven for fearing the worst after the heavy sell-off in the last two days of January 2020 left the FTSE 100 down 3.8% for the month. That is the weakest start to a year since 2014.

The January stumble means the FTSE 100 has, at the time of writing, lost all of the gains made in the immediate aftermath of last December’s general election result.

This loss of confidence can also be seen in how the yield on the benchmark UK 10-year government bond (also known as a Gilt) slumped from a high of 0.87% to just 0.55% in January, as investors piled into fixed-income.

But what the fresh drop in Gilt yields (and increase in Gilt prices) and latest fall in share prices all mean is that UK stocks look even cheaper relative to bonds than they did before, especially on a yield basis.

This column’s data only goes back to the mid-1990s for UK Gilts, but the premium offered by the FTSE 100 relative to the 10-year Gilt stands at 3.9 percentage points, or 390 basis points.

Research from the fund management group Man GLG suggests the premium is the highest it has been since 1939, when Europe was preoccupied with an imminent war.

The dividend yield remains a key part of the investment case for UK equities, although sceptics will counter that there are three good reasons why the UK offers a premium yield – and the main one is the risk associated with owning UK equities.

Investors are demanding a premium yield to compensate for three perceived dangers:

1 – The risk of economic upset in a post-Brexit world, thanks to Brexit itself, the coronavirus or some other event.

For the moment, the viral outbreak is the biggest worry and it is to be hoped that Chinese efforts to contain it prove effective. Equally, it seems likely that Chinese GDP will take a hit and since we are talking about the world’s second-biggest economy the wider the spread of the disease, the greater the economic damage, since the effects will surely linger.

2 – The combination of relatively low dividend cover and relatively high debt.

Based on analyst forecasts, dividends are covered just 1.62 times by earnings across the FTSE 100 in 2020, some way below the comfort level of twice covered that provides a buffer against unexpected events. In addition, net debt has more than doubled since 2007, according to Man GLG, to further limit executives’ room for manoeuvre.

3 – Dividend concentration.

More than half of the FTSE 100’s dividend payments come from just 10 stocks so investors need to be comfortable with the business prospects, cash flows and balance sheets of Royal Dutch Shell (RDSB), HSBC (HSBA), BP (BP.), British American Tobacco (BATS), GlaxoSmithKline (GSK), Rio Tinto (RIO), AstraZeneca (AZN), Lloyds (LLOY), BHP (BHP) and Vodafone (VOD) in particular, especially as few of them look to offer compelling growth narratives.

Investors were also demanding a premium to help compensate them for the risk – as it was seen – of a Labour government. That risk has passed for five years (in theory) and as a result, share prices initially gained and the dividend yield came down.

It therefore stands to reason that share prices could go higher again, further decreasing the yield, if these new fears are assuaged and investors become more confident in the prospects for UK stocks.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Education

Exchange-Traded Funds

Feature

Great Ideas

Great Ideas Update

Money Matters

News

- China trusts under pressure from coronavirus fears

- Sales growth challenges weigh on Diageo and Unilever shares

- The key challenges facing new BP boss

- Surging stock prices mask concerns about a US economic slowdown

- The companies in the race to find a coronavirus cure

- Burford Capital shares gain despite earnings warnings