Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBargain opportunity as Artemis fund sharpens focus

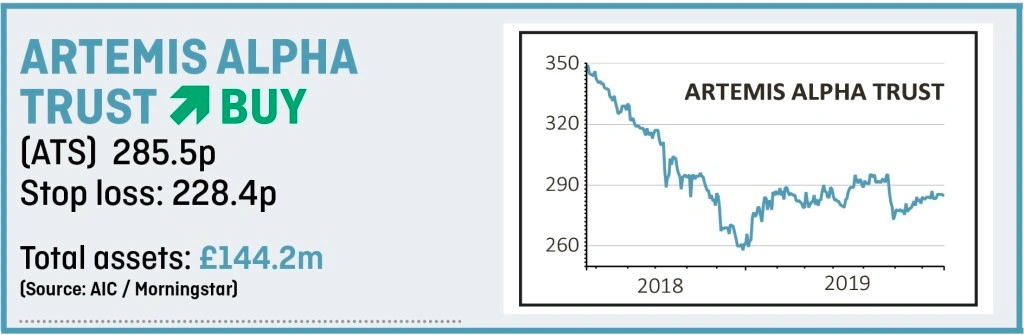

A steep 19.3% discount to net asset value (NAV) on Artemis Alpha Trust (ATS) should pique the interest of contrarian value investors.

A thorough portfolio restructuring and potential relief if Brexit is sorted out quickly offer catalysts for an improved performance and re-rating of the trust, steered by experienced investor John Dodd and up-and-coming stock picker Kartik Kumar.

Launched in 1998, Artemis Alpha Trust aims to provide long term capital and income growth by investing in listed companies. It wants to achieve a net asset value total return greater than that of the FTSE All-Share index while growing dividends at a rate greater than UK CPI inflation.

A revised investment strategy was announced in 2018 and subsequent changes have been made to the portfolio. A bit more work is needed and then hopefully the benefits will feed through to performance.

The fund managers are now seeking quality companies with competitive advantages and attractive industry characteristics, trading on compelling valuations and steered by what they deem to be outstanding management. This strategy is long term in focus and will involve a relatively low turnover of investments.

During a transitional year to 30 April 2019, the NAV and share price fell by 8.6% and 8.9% respectively on a total return basis, thus underperforming a 2.6% increase for the benchmark FTSE All-Share. However the poor performance reflected disappointing showings from some unquoted investments and declines for quoted companies with sensitivity to the UK economy.

Dodd and Kumar are confident a portfolio repositioning will result in improved returns for shareholders. They have dramatically reduced the fund’s exposure to illiquid unquoted investments while putting money to work with more liquid mid and large cap stocks.

Unquoted holdings have been reduced to 8.7%, down from 21.6% at the previous year end and this number will come down further in the future. The portfolio has been rationalised from 91 to 49 holdings, while the exposure to mid and large caps has risen from 35.1% to 60.3%.

Top 10 holdings include groceries giant Tesco (TSCO), the internet business conglomerate Rocket Internet, serviced office operator IWG (IWG) and Mike Ashley’s Sports Direct International (SPD).

The managers have also used weakness at Plus500 (PLUS) to increase the holding in the online trading platform, having seen further evidence of its strong technology and culture following a visit to Tel Aviv.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.