Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineRecord levels of corporate debt is not good news

The failure of Thomas Cook is a timely reminder of the destructive power that excessive debt can have on shareholder value. Investors have been wiped out by the strain of the package holiday firm’s £1.5bn borrowings.

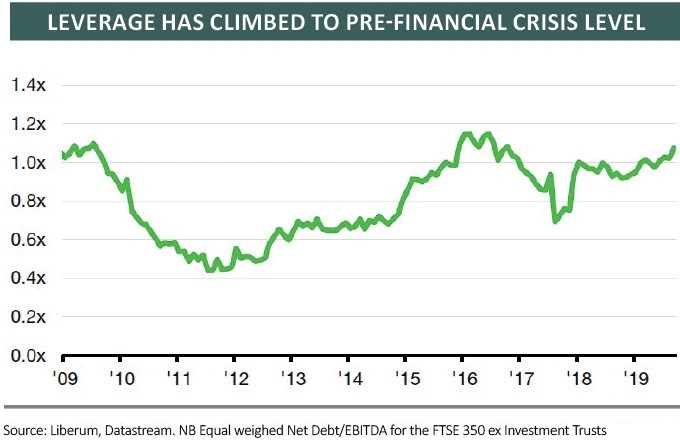

A decade on from the global financial crisis and UK corporate leverage is back at pre-crisis highs, having risen steadily since 2012.

Andrew Coury, an analyst at investment bank Liberum, says corporate debt came off sharply in the wake of the financial crisis but has since steadily climbed. ‘The current level of leverage in the UK is now in line with pre-financial crisis levels,’ he adds.

This adds up to a record £443.2bn for UK plcs, according to the September Link Group Debt Monitor 2019, which tracks borrowings for UK listed companies, following eight consecutive years of growth.

While the change in debt has varied widely, very few sectors have managed to reduce their leverage over the past 10 years. ‘Only the housebuilding, staffing and technology sectors had an improved net debt-to-earnings before interest, tax, depreciation and amortisation (EBITDA) ratio over the last 10 years,’ reveals Coury. ‘Leverage of debt-heavy sectors, such as telecoms, leisure and pharma has worsened.’

CHEAP TO BORROW

This situation is not altogether surprising given the loose monetary policy of successive UK governments since 2009, when a string of quantitative easing programmes combined with the lowest base interest rates in generations made borrowing very cheap.

‘Borrowing will always rise over the long term because debt is almost always a cheaper means of raising capital for investment than equity,’ says Michael Kempe, chief operating officer of Link Market Services, which produces the Debt Monitor.

‘As companies grow, their capacity to take on new loans to finance their expansion increases.’

This is all well and good as long as decent growth can be maintained, but that is not the case at present. The Profit Watch UK’s second quarter report shows that UK plc revenues inched only 1.6% ahead between April and June, with a third of companies reporting lower sales year-on-year.

The same report shows profits for UK companies rose 3.1% between April and June, yet only because they were puffed up by the weak pound, and propped up by above-average profit from the top 40 UK-listed multi-nationals.

‘Those outside the top 40 saw profits drop by a third, the fifth consecutive quarter of declines,’ Profit Watch UK says. More than half of companies reported lower profits thanks to a widespread and dramatic margin squeeze since 2007, meaning an extra £787bn of revenue only generated £16bn more in profit.

MANAGING THE EARNINGS IMPACT

Brexit bickering and parliament’s prorogue paralysis has left the Bank of England loathe to raise rates and run the risk of plunging the UK into a damaging recession.

Last week the Bank of England left its base rate unchanged at 0.75%, a decision widely anticipated by the markets as interest rate policymakers juggle keeping inflation in check versus stimulating growth.

This gives the Bank of England room to cut rates in the event of a no-deal Brexit, but it has previously taken the view that a tightening of policy may be necessary post-Brexit.

If the Bank of England lifts the base rate, current levels of debt could weigh heavily on corporate earnings and share prices as companies bear increased costs of servicing debt.

But there is little reason to panic now. ‘Considering UK plc’s debt pile in isolation doesn’t tell the whole story,’ says Link Market Services’ Michael Kempe. ‘Despite debts reaching new records, the measures of debt burden and sustainability are not yet stretched.’

He adds: ‘It’s really important to consider the burden of debt, and how sustainable it is as well. This is why the increase in borrowing in 2018/19 isn’t a cause for concern.

‘It’s well backed by assets, and easily serviced at present by the profits companies are making. There are companies and sectors under strain, but the overall picture is reasonably comfortable.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.