Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineInvesting under the cloud of Brexit

With just over a month to go until the UK’s scheduled departure from the European Union and, just like everyone else, investors are none the wiser on whether we face further Brexit delay, no deal or a negotiated exit.

Which of these three potential outcomes comes to pass is likely to be determined at a crunch EU summit on 17 and 18 October.

And, barring a vote of no confidence by MPs for which there is precious little time, prime minister Boris Johnson looks set to be leading the negotiations with the EU.

Heading into that event Johnson appears to have suffered a setback in his arm wrestle with MPs over the destiny of Brexit following a damaging decision from the Supreme Court on his decision to prorogue parliament.

But still there are considerable uncertainties over how we arrive at deal, no deal or delay. To help you navigate what could be a choppy end to 2019 this article will examine the potential scenarios in turn and what the likely market impact will be.

LIFE AT THE CLIFF EDGE

Uncertainty is the key issue for markets rather than Brexit itself. Panmure Gordon chief economist Simon French says: ‘Part of the frustration with Brexit is that it is neither a single issue, nor does leaving the EU in itself codify what type of UK economy will emerge.

‘The decisions over regulation, immigration, tariffs, standards and industrial strategy will be of far larger significance for the economic outlook than the simple act of being outside the EU’s legal and political order.

‘That Brexit enables more flexibility to frame these issues in the UK’s image is a potential upside for economic growth, but that upside can also be squandered if the UK chooses to diverge from its biggest trading partner with no obvious objective.’

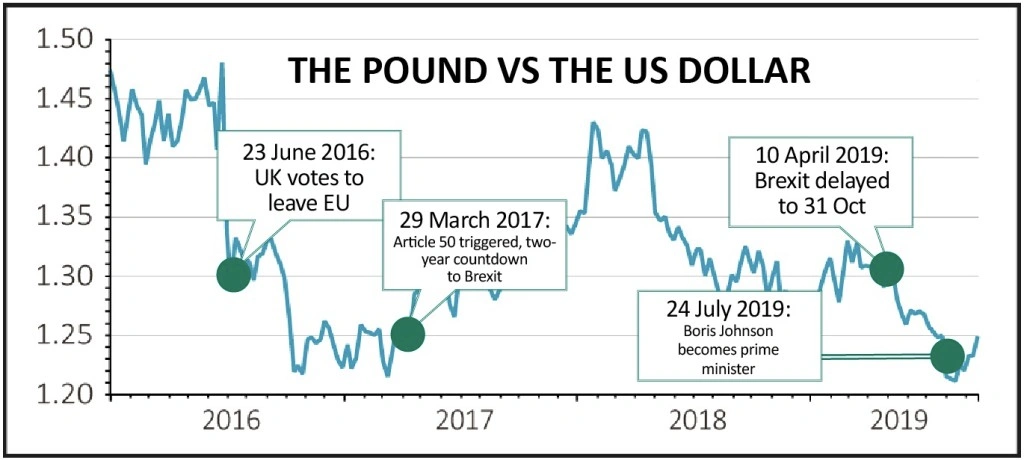

The main barometer for Brexit will be sterling and how it performs against other major currencies such as the euro and the US dollar.

Since the June 2016 vote to leave the EU sterling has traded in a rough range between $1.20 to $1.40 against the dollar, having been at around $1.50 immediately before the vote amid expectations for a remain result. (See chart on next page)

More recently, and since the election of Johnson as Conservative Party leader and ultimate elevation to Number 10 this summer, it has traded much closer to the $1.20 mark. This reflects Johnson’s apparent greater willingness to accept a no deal outcome than his predecessor Theresa May.

Nigel Green, chief executive of wealth management firm deVere, says: ‘Since Boris Johnson succeeded Theresa May in July, our consultants have registered a 35% increase in investors – both UK domestic and international – seeking to reduce their exposure to UK assets, including UK pensions, bonds and sizeable holdings of sterling. The only exception is UK property.’

FOREIGN PREDATORS SWOOP FOR UK FIRMS

The weakness in the UK’s currency has also made its companies less expensive for foreign suitors and we’ve seen several high profile deals since the Brexit vote.

For example, UK technology champion ARM was snapped up by Japanese firm Softbank as early as July 2016. Comcast snared pay-TV broadcaster Sky for £30bn in 2018 and London Stock Exchange (LSE) was recently the target of a blockbuster bid from its Hong Kong counterpart – a proposal which has been firmly rebuffed for now.

WHAT A BREXIT DEAL COULD MEAN FOR INVESTORS

HOW WOULD WE GET THERE?

In some ways this is the simplest outcome to unpick. The short-term possibility is that Boris Johnson secures a deal at the EU summit, perhaps with some adjustment to the key sticking point of the backstop.

European Commission president Jean-Claude Juncker remarked last week that a new Brexit deal could still be reached before 31 October, triggering a small rally in the pound.

Given the limited time available to ratify a deal there might be a brief extension to allow this process to be completed.

Or in the face of an imminent no deal scenario MPs could vote for a version of the deal Theresa May agreed with the EU but tried and failed to get through the House of Commons.

Alternatively a different government formed in the wake of a general election could negotiate its own deal. Or a freshly negotiated deal could be put to voters in a second referendum and win a majority.

WHAT WOULD BE THE IMPACT?

Panmure Gordon’s Simon French says: ‘Brexit is so multi-layered that the impacts on companies and households will vary significantly. However a sensible starting point is to assume that a deal with the EU will remove some of the near-term uncertainty and lead to a short, but significant boost in business investment, export orders and appetite for big ticket purchases.’

This sounds like good news for the UK retail sector and housebuilders, property stocks, banks and other domestic firms could get a boost. Fidelity Special Values (FSV) – a recent addition to our Great Ideas portfolio and which focuses on undervalued domestic stocks – is a good example of a fund that could benefit from a Brexit deal.

WHAT A NO-DEAL BREXIT COULD MEAN FOR INVESTORS

HOW WOULD WE GET THERE?

Berenberg senior economist Kallum Pickering recently put the chance of a no-deal outcome on (or before) 31 October at 2.5% following MPs’ move to legislate against this outcome. The fact there is a slim chance, rather than none at all, of having a no-deal reflects the belief that Johnson could find a loophole in this legislation.

There is now insufficient time for a general election before 31 October but an election seems almost certain at some point soon given Johnson is currently operating without a majority in the House of Commons.

If he were able to secure a majority in an election, he would be free to pursue a no-deal outcome presumably at the end of January 2020 based on the three-month extension described in the Benn bill blocking no deal.

Alternatively MPs could approve a second referendum with no deal as one of the options presented to voters, and this option could prevail.

Finally, and perhaps the most likely of these scenarios, the EU could refuse an extension, although the potential impact on member state Ireland might count against this.

WHAT WOULD BE THE IMPACT?

In the short-term no-deal Brexit is likely to mean significant disruption, despite more concerted efforts on the part of the UK Government to prepare for such an outcome.

Panmure’s Simon French says: ‘A no deal will, at a scale that is hard to know for certain, introduce additional costs for households and businesses and mute economic growth. Given the current rate of growth is quite modest, a technical recession is possible.’

The OECD is forecasting a 3% hit to UK GDP and a recession in 2020 under a no-deal Brexit.

French adds that further weakness in the pound seems inevitable. ‘The scale of this drop will depend on how long the disruption persists for – but a move down towards $1.15 and parity with the euro is not out of the question,’ he says.

This outcome could hurt domestic-facing stocks like housebuilders, real estate owners and banks the hardest.

Counter-intuitively the FTSE 100 might benefit, barring some short-term volatility, because weaker sterling boosts the relative value of earnings in other currencies.

Logistics businesses and warehouse owners might benefit from stockpiling as corporations look to deal with the short-term disruption.

In the longer term no deal is unlikely to result in a clean break but instead lead to further negotiations as the UK and EU grapple with movement of goods and the thorny issue of the Irish border.

WHAT A BREXIT DELAY COULD MEAN FOR INVESTORS

HOW WOULD WE GET THERE?

The least complicated route is that Boris Johnson steps away from his ‘dead in a ditch’ rhetoric and asks for an extension, as MPs have mandated, and the EU agrees.

If he cannot find another route out, and still refuses to contemplate a delay, he would probably have to resign and somebody else would have to form a government.

Whether a ‘unity’ candidate or the leader of the official opposition Jeremy Corbyn – this individual’s first act would be to ask for an extension.

WHAT WOULD BE THE IMPACT?

A delay in market terms would probably prolong the current limbo situation. Bank of England governor Mark Carney recently warned a further delay would hurt the economy by extending the uncertainty for companies and workers.

Longer term either a government emerges which takes the UK out of the EU under no deal or through a hard Brexit deal. The alternatives include a rival administration agreeing a softer Brexit with stronger ties to the EU or there is a second referendum which results in the country remaining in the EU.

The Liberal Democrats have said they would revoke Article 50 and cancel Brexit if they form a majority government after an election.

WHAT COULD HAPPEN UNDER A LABOUR GOVERNMENT?

Some market observers have characterised the current situation as a choice between two paths, a no-deal exit under Boris Johnson or remaining in the EU under a government led by Labour leader Jeremy Corbyn.

The situation is not that simple. Current polling suggests Corbyn would be unlikely to form a majority government, but the political winds are very unpredictable at present and some of Corbyn’s stated policies would likely have a material impact on investors.

There is always a chance he might get some of them through with the help of partners in a coalition. Corbyn heading a coalition government seems a much more live possibility.

A pledge to renationalise the UK’s utilities and transport system would be bad news for shareholders in these sectors.

More broadly, higher taxes would likely pressure how much you have to invest and there has to be a risk a Labour government would be less generous with the investment tax breaks available through ISAs and SIPPs.

Greater spending could provide a boost for infrastructure firms, depending how contracts were awarded, but could damage public finances particularly when you consider the costs of renationalisation.

Artur Baluszynski, head of research at asset manager Henderson Rowe, says this is not fully appreciated by the market. He adds: ‘The market is using the pound as a Brexit risk gauge in the short term, but the risk no one is talking about is the UK gilt market.

‘Even if we manage to avoid a no-deal Brexit, but end up with a fiscally irresponsible Labour government which tries to undermine London’s status within the global financial system, the UK’s credit quality could come under pressure.

‘This would mean the UK’s ability to run external deficits for an extended time without serious negative consequences could be questioned.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.