Vodafone dials up another disappointing quarter

Archived article: Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

“It was legendary investor Jim Slater who noted, ‘elephants don’t gallop,’ as he explained his preference for small caps over large ones, and the pedestrian progress shown by megacap plodder Vodafone would only reinforce the strength of his convictions,” says AJ Bell investment director Russ Mould.

“The telco’s third-quarter update reveals a further slowdown in organic revenue growth and although the company is sticking to its previously downgraded earnings and cashflow targets, the shares trade no higher now than they did in December 1997. No doubt Mr Slater would have just nodded and moved on.

Source: Refinitiv data

“Hemmed in by regulators on one side and competition on another, Vodafone may still be fighting on too many fronts in too many countries, especially as it remains saddled by an awful lot of debt. The latest increase in the liabilities came in calendar 2019 (the fiscal year to March 2020) as a result of the purchase of Liberty Global’s German, Czech, Hungarian and Romanian operations for an all-in price, including their borrowings, of €18.4 billion.

Source: Company accounts. Financial year to March

“Then chief executive Nick Read described the deal as completing Vodafone’s ‘transformation into Europe’s leading converged operator,’ and that dreaded word ‘transformation’ was all investors needed to hear. It is usually code for ‘we know we’ve overpaid for this, but we really wanted to have it’ and quite often transformational deals transform the fortunes of the buyer in quite unintended ways.

“This could be the case again at Vodafone and is all a bit reminiscent of the turn of the century, when the huge Mannesmann deal, also in Germany, proved a step too far as Vodafone ultimately overpaid for its prey.

“The debt burden makes it harder for Vodafone to invest and compete on so many fronts, especially as the interest payments will siphon off cash that could be otherwise used to buttress the company’s competitive position.

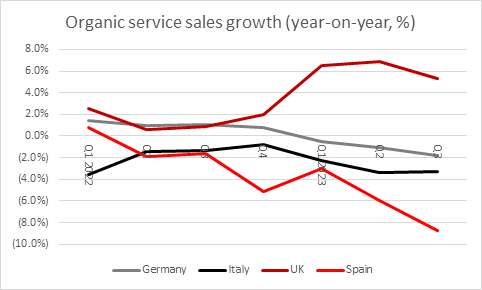

“In addition, the German market, already competitive, is tougher still following the introduction of the new Telecommunications Act in 2021, which made it easier for consumers to cancel contracts and harder for providers to automatically renew them. Vodafone continues to flag Germany an area of difficulty and organic revenues have now shrunk year-on-year for three straight quarters. Only the UK, of Vodafone’s four big European markets, is showing any real momentum.

Source: Company accounts. Financial year to March

“As a result, Vodafone’s organic growth rate is plodding along in an ungainly, elephantine way.

Source: Company accounts. Financial year to March

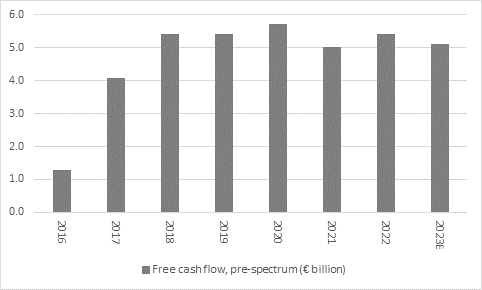

“It is not all bad news. Interim chief executive officer Margherita Della Valle is sticking to the company’s earnings and free cash flow targets for fiscal 2023, although they had been downgraded by Mr Read before his departure and hardly show much momentum either, even as the company tries to conjure it up with further wheeler-dealing.

Source: Company accounts, Marketscreener. *2023E based on mid-point of company guidance. Fiscal year to March

“The sale of Hungary, withdrawal from Egypt and transfer of control of the majority-owned Vantage Towers could help the balance sheet, and that is a step forward, as less debt means less risk and less risk can mean a higher rating for the stock (and thus share price), all other things being equal.

Source: Company accounts, management guidance for 2023E. Financial year to March

“But such asset shuffling does still leave Vodafone open to accusations that it looks like an investment trust of telecoms assets that is offering nothing much by way of sales, profit or dividend growth.

Source: Company accounts, Marketscreener, analysts’ consensus forecasts. Fiscal year to March

“At least the €0.09 annual dividend, usually paid in two €0.045 instalments, seems secure enough as Vodafone is generating cash and free cash flow cover for the payment looks good, even if earnings cover seems skinny by comparison. At current exchange rates that comes in at just under 8p a share, enough for a dividend yield of nearly 9%.

| € millions | 2018 | 2019 | 2020 | 2021 | 2022 |

|---|---|---|---|---|---|

| Sales | 46,571 | 43,666 | 44,974 | 43,809 | 45,580 |

| Operating profit | 4,298 | -951 | 4,099 | 5,097 | 5,664 |

| Depreciation & amortisation & impairments | 10,884 | 13,320 | 15,859 | 14,101 | 13,845 |

| Net working capital | (858) | (577) | (70) | (216) | (416) |

| Capital expenditure | (7,321) | (8,151) | (7,605) | (9,139) | (7,807) |

| Operating Cash Flow (OpFcF) | 7,003 | 4,795 | 12,283 | 9,843 | 11,286 |

| OpFcF from discontinued operations | 858 | (372) | 0 | 0 | 0 |

| Operating Cash Flow | 7,861 | 4,423 | 12,283 | 9,843 | 11,286 |

| Tax | (1,010) | (1,131) | (930) | (1,020) | (925) |

| Interest / leases | (753) | (2,088) | (3,549) | (1,027) | (1,964) |

| Pension contribution | 0 | 0 | 0 | 0 | 0 |

| Licensing and spectrum spend | (1,123) | (181) | (837) | (1,221) | (896) |

| Free Cash Flow | 4,975 | 1,023 | 6,967 | 6,575 | 7,501 |

| Dividend | 3,920 | 4,064 | 2,296 | 2,427 | 2,474 |

| Free cash flow cover | 1.27 x | 0.25 x | 3.03 x | 2.71 x | 3.03 x |

Source: Company accounts

“It will be interesting to see if that yield and the ongoing share buyback programme, provides support to the stock, as investors demand such a high figure to compensate themselves for the apparent lack of underlying sales, earnings and dividend momentum.”

These articles are for information purposes only and are not a personal recommendation or advice.