Investing early: What does the maths tell us?

We ran some numbers based on investing £1,000 in a typical global fund every year from 1999, when ISAs began*.

If you’d diligently invested on the first day of each tax year, you could now have £4,150 more than someone who had invested on the last day of every tax year. That’s despite putting in exactly the same amount: £26,000.

Last-minute ISA investors could have turned that £26,000 into £71,525, while early birds wcould now be sitting on £75,675.

The reason for this loftier return? Early birds invest their money for that bit longer. Markets, of course, go up and down, but they generally rise more than they fall. Since 1999, the global stock market** has risen in 18 out of 25 tax years. So around two-thirds of the time you would have bought in at a lower price by investing at the start of the tax year, rather than waiting until the end. And that translates into better returns for your ISA.

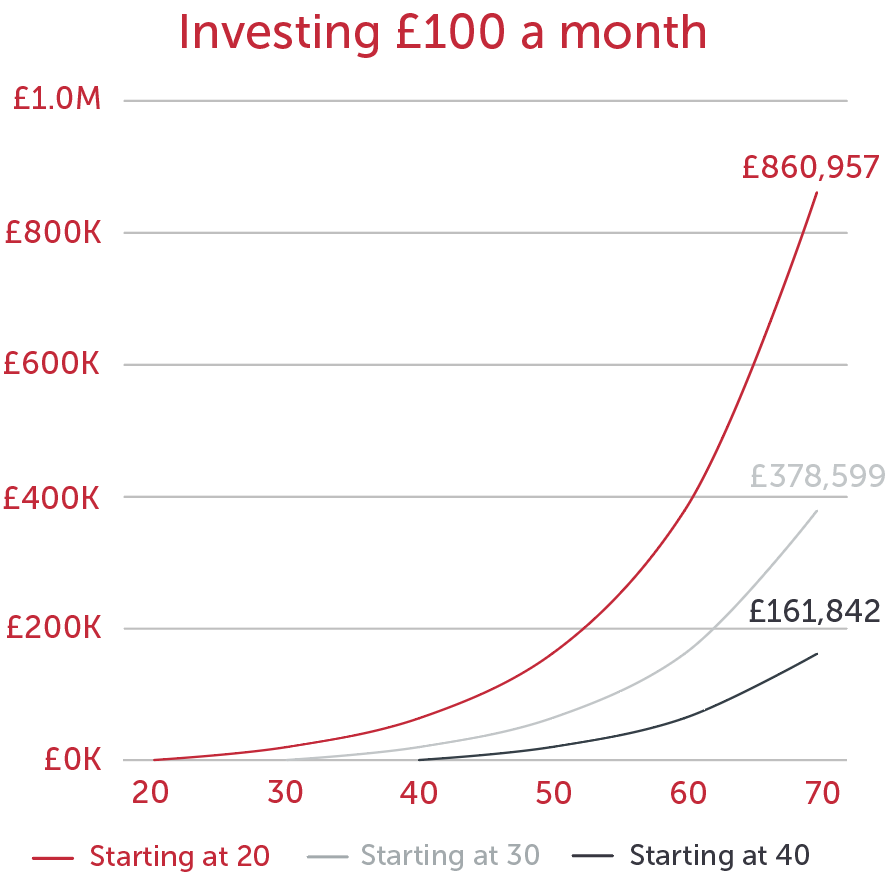

What is compound interest?

One of the benefits of early investing is it allows you to build your pot through compounding. Compound interest is the cumulative interest your savings and investments can build up over time, so the return is applied not just to the initial amount you save, but any returns you also reinvest.

This can create a snowball effect, which makes your investment grow exponentially over time (assuming the rate of return is positive).

For illustrative purposes only, based on a £1,000 initial investment, then £100 a month. 8% annual return, exclusive of platform and dealing fees.

Investing every month

Another popular way to invest in your ISA is through monthly instalments.

If you’d invested £1,000 into your ISA every year since 1999 – but split it into monthly instalments – you could have turned your £26,000 overall investment into £74,680. That’s a bit less than an early bird, but £3,155 ahead of a last-minute ISA investor.

Again, the same principle is at play. Drip-feeding your money means it’s in the market longer than if you wait to invest all of it on 5 April – giving it longer to grow. And there’s another advantage to investing regularly. Because your money is transferred from your bank account automatically each month, it’s hassle-free and takes the emotion out of investing. So, it can be a simple and smart way to invest.

Of course, whether you’re a regular saver, an early bird or a last-minute ISA investor, you’re still streets ahead of someone who isn’t contributing to an ISA at all. But if you want to make your money go even further, history shows us that more often than not, it’s the early bird that catches the juiciest worm.

Example: £1,000 invested in an ISA each year since 1999

| Type of ISA investor | Amount saved | Current value |

|---|---|---|

| Early bird | £26,000 | £75,675 |

| Last minute | £26,000 | £71,525 |

| Regular saver | £26,000 | £74,680 |

Sources: AJ Bell, FE, Morningstar, total return of IA Global Sector Average in GBP to 5 April 2025.

Methodology: current value of a £1,000 annual ISA contribution made since 1999 on the first day of each tax year (early birds), on the last day (last-minute ISA investors), or spread across 12 regular monthly payments of £83.33 each year (regular savers).

Is it a good time to invest?

By investing your money in the market, there's a chance for your savings to grow at a quicker rate than simply what you would make through cash interest. Though these returns aren’t guaranteed, and cash can feel like a safer option, investing has historically outpaced holding your money in cash. In the past decade, an investment of £1,000 in the average global index fund would have turned into £2,600. If that same money was kept in cash, that investment instead would be £1,154.*

Learn more about saving versus investing

Ready to invest?

If you’re ready to take the plunge into investing, one of the most popular ways is through using an ISA. An ISA is a savings wrapper that protects your money from tax and allows you to contribute £20,000 each year. If you plan to invest your money, you can do this through a Stocks and shares ISA for example.

Read more about which ISA account is best

*Source: FE Analytics and BOE database, to 1 July 2025

**Based on the MSCI World index