Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

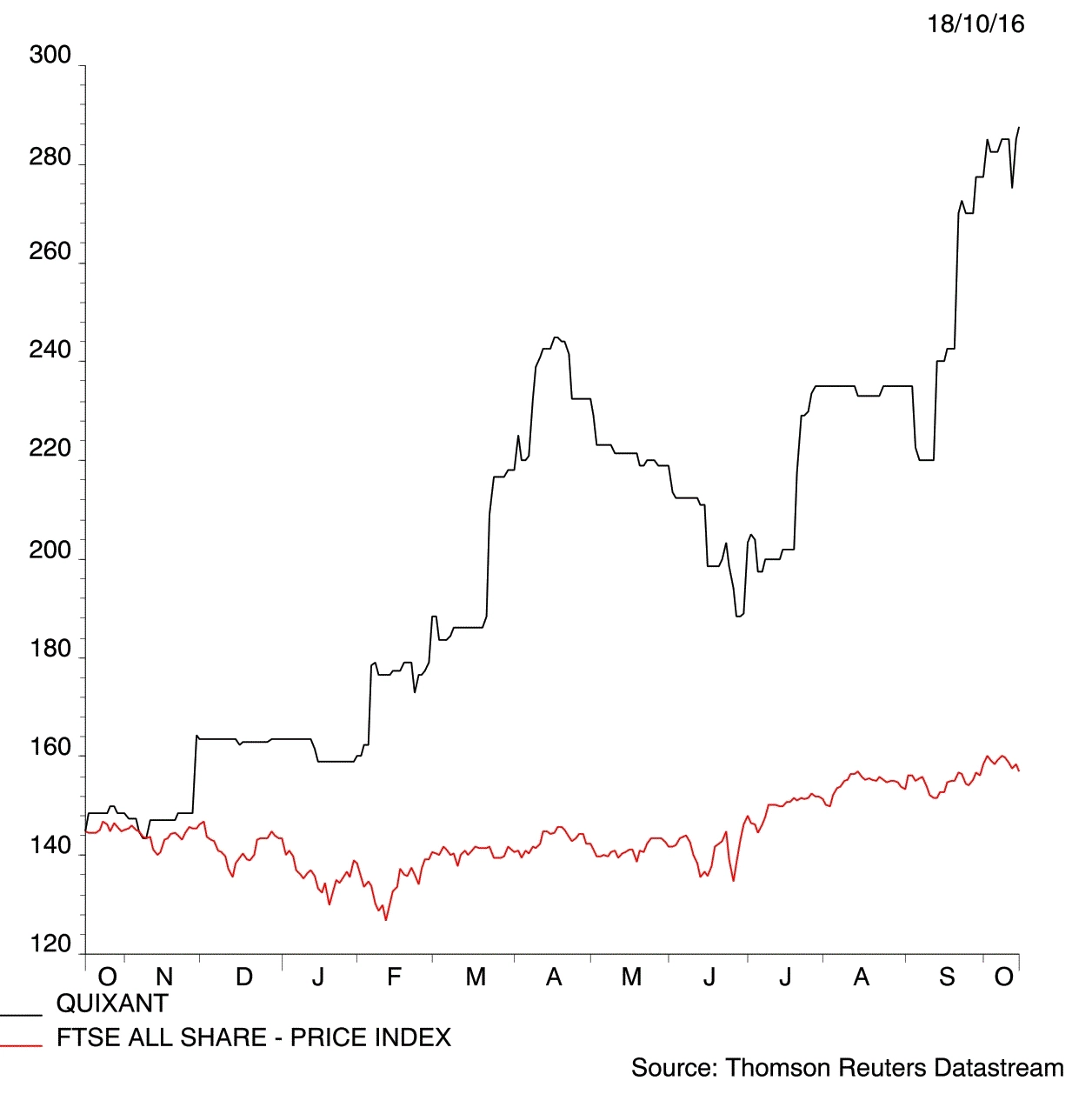

magazineQuixant is in the growth slot

The next year or so should transform gaming platform designer Quixant (QXT:AIM). Enjoying rapid growth, a technological edge and reasonable pricing power, we firmly believe this is a must-have stock for your ISA or SIPP.

The Cambridge-based company designs the logic boxes that control pay-to-play digital gaming machines – one arm bandits, quizzes, casino; it is the brains behind the games.

It’s a winner

Outsourced logic boxes are fast becoming the accepted norm across the vast and highly competitive gaming machine industry. Quixant’s all-in-one boxed solution offers a low-cost, high-quality and innovative product that increasingly appeals to manufacturers keen to concentrate their own research and development (R&D) efforts on game design and development, the core differentiator in attracting players from one terminal to another.

This is a niche but large market. Estimates suggest around 8m gaming machines installed worldwide but very few gaming platform suppliers. Most production is in-house and there are clear drivers to outsource, such as the increasing cost of development and an ever-changing legislative environment.

There are five major (or tier-1 as they are called) gaming machine designers in the world; a couple in the US, one in Australia, two more in central Europe. All operate globally and Quixant has long-standing relationships with them all. This small group owns about 90% of the gaming machines worldwide.

Rising through the tiers

So far Quixant’s main customers have been smaller tier-2 operators, such as Ainsworth Game Technology based in Australia, with whom Quixant signed a new multi-year deal in May. Earlier still Ainsworth sold a majority stake in its business to Novomatic of Austria, one of the tier-1 players, effectively giving Quixant an even bigger foot in the door to volume orders.

The potential difference could be massive. According to Quixant management, a typical tier-2 contract would be for 10,000 logic boxes – in a good year, a tier-1 order would be 10 times that amount.

Sealing a meaningful tier-1 agreement has taken longer than hoped, but for good reasons. Over the last 18 months or more there have been quite a few takeovers in this space, with bigger players hoovering up the small.

Analysts believe this corporate activity may have put outsourcing on hold temporarily, a dynamic that is likely to change through 2017 as customers extract value from their own operations. In the meantime, Quixant has worked at cementing its place at the negotiating table with proof-of-concept-type deals. (SF)

Quixant (QXT:AIM) 285p

Stop loss: 228p

Market value: £185.8m

Prospective PE Dec 2017: 19.7

Prospective PE Dec 2018: 13.2

Dividend yield: 1.4%

Analyst price target: 250p

(FinnCap)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.