Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFunds for income drawdown

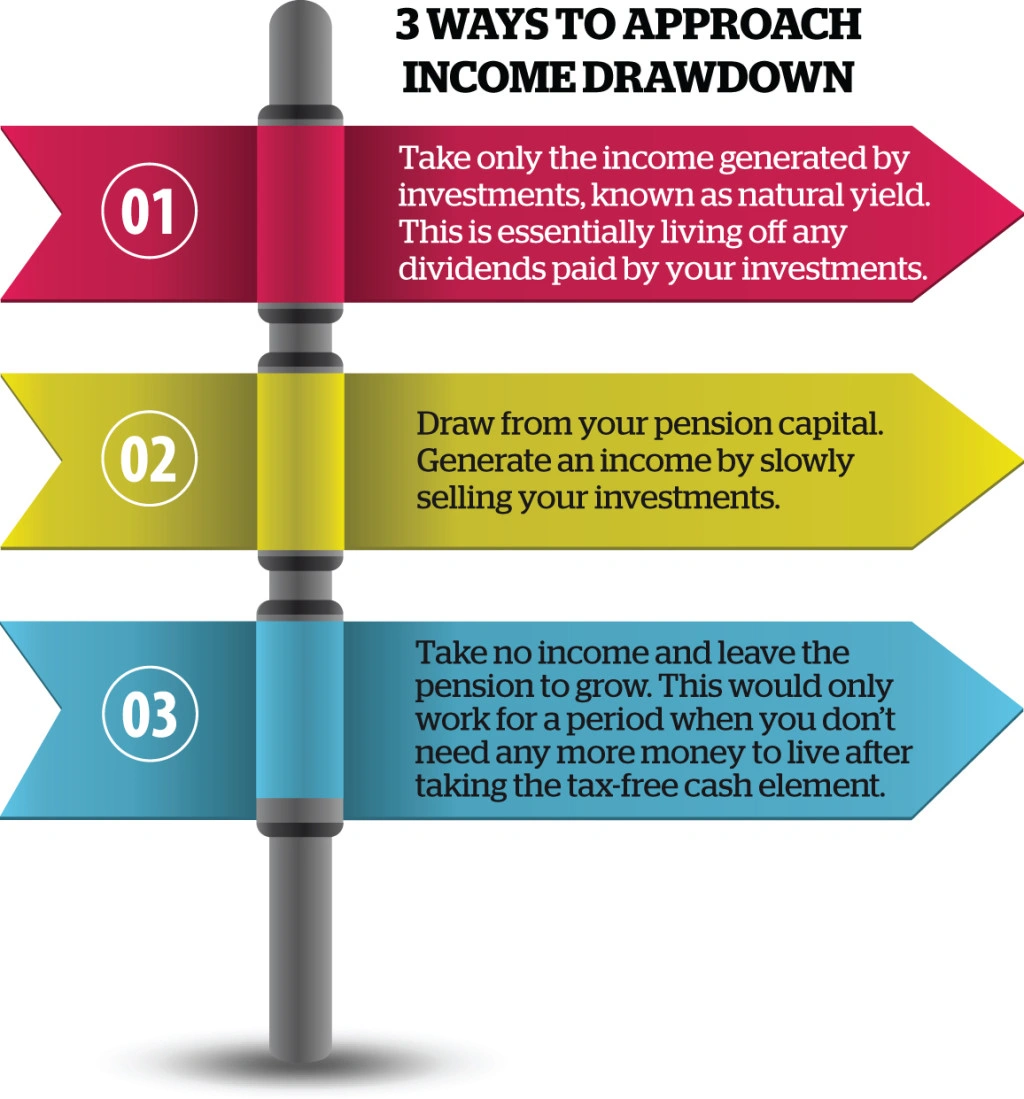

People in retirement are increasingly turning to income drawdown as a means of generating an income rather than buying an annuity.

You can either draw income generated by the underlying investments such as dividend payments; or you can sell small chunks of your investments to create cash for withdrawals.

The downside with the latter method is that your investment pot is gradually shrinking, unless the underlying asset value grows fast enough to offset the chunks being withdrawn.

Therefore you should choose your investments wisely with a view to picking assets that pay decent dividends such as top-quality funds. We provide some fund ideas in this article.

More control, more risk?

Drawdown gives people more control and creates the opportunity to grow their capital for longer, but it leaves them exposed to market risk and could mean they run out of money early.

A safer option for retirees is to invest in relatively low risk funds that pay a high enough yield to meet their income requirements.

‘Income drawdown offers investors flexibility in terms of the withdrawals, but it runs the risk that the withdrawals can’t be maintained in the long-term due to unsustainable income levels or adverse market conditions,’ says Martin Bamford, managing director of financial planning group Informed Choice.

Asset management groups were quick to spot the opportunity and have launched a number of new funds to target the drawdown market, but the low yield environment has created real challenges and resulted in mixed performance.

Under the spotlight

A good example is Jupiter Enhanced Distribution (GB00BZ0PF042), which was created in September 2015 and aims to provide a monthly income with the prospect of long-term capital growth by investing in a diversified range of assets.

It is a small fund with just £17.9m of assets under management, but has generated a total return of 5.2% in the last year and is yielding 3.6% with equal monthly distributions.

The £14.5m Rathbone Strategic Income Portfolio (GB00BY9BSL83) was launched around the same time. It attempts to generate a long-term total return of CPI inflation plus 3% to 5% each year as measured over a minimum period of five years, subject to a targeted minimum annual yield of 3%.

It invests in different asset classes and has produced a total return of 9% in the last 12 months with a 2.88% yield and variable monthly dividends.

Inflation protection

David Coombs, the fund manager, says that for any sterling income investor, the largest risk at the moment is an inflation shock in the UK. ‘To protect ourselves against this scenario, we are focusing on short-term bonds, which are less sensitive to changes in interest rates than the benchmark 10-year.

‘Our bias to high-quality equities also helps with an inflation shock, as companies that can raise prices in-line with inflation because of their competitive position or brand offer safe harbours in inflationary times.’

Aviva Investors Multi-Strategy Target Income (GB00BQSBPF62) was launched in December 2014 and aims to generate a target annual income yield of 4% above the Bank of England base rate in all market conditions with monthly distributions.

The four-man management team also seeks to preserve capital, while keeping the volatility to less than half of that of global equities over rolling three year periods.

In order to achieve this threefold objective the managers use a multi-strategy approach that includes the extensive use of derivatives. The £1.7bn fund has generated an historic yield of 5% with reasonably consistent monthly distributions, but has made a small capital loss in the last 12 months.

More established alternatives

Adrian Lowcock, investment director at Architas, recommends Fidelity Enhanced Income (GB00B87HPZ94), an equity fund that uses derivatives to boost the yield which stands at 7.76% yield, according to Morningstar.

He also likes Troy Trojan Income (GB00B01BNW49) which has a diversified portfolio that targets total return and inflation protection. It has a 4% yield.

‘Another good option is Newton Real Return (GB0006780323), where manager Iain Stewart’s first objective is capital preservation, which is an important consideration for drawdown investors as any money lost cannot easily be replaced. Beyond this he looks for growth and a return above inflation.’

Fixed income route

Drawdown investors may wish to consider a fixed income fund as these normally offer a decent yield with a fair degree of capital stability.

The £153m Henderson Diversified Income (HDIV) investment trust has a more flexible mandate than most of its peers and aims to generate a high level of income with long-term capital growth. Its net asset value is up 59.9% over the last five years and it is currently yielding 5.79% with quarterly distributions.

Fund manager John Pattullo flags a reasonably large allocation to secured loans that are senior in the event of a default and pay floating interest rates. He also likes US high yield bonds and some investment grade corporate debt, but warns of a tougher outlook for bond managers in the short-term. ‘We are going to keep liquid, be sensible, and look for opportunities, but not force it.’ (NS)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.