Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineEpwin should be attractive to income seekers

We’re generally cautious about companies with high dividend yields, as it tends to represent disbelief by the market that the money will be paid. One exception, in our view, is building products business Epwin (EPWN:AIM) which has a handsome 6.5% prospective dividend yield.

We view Epwin as having a resilient business and note it has limited debt and excellent cash generation.

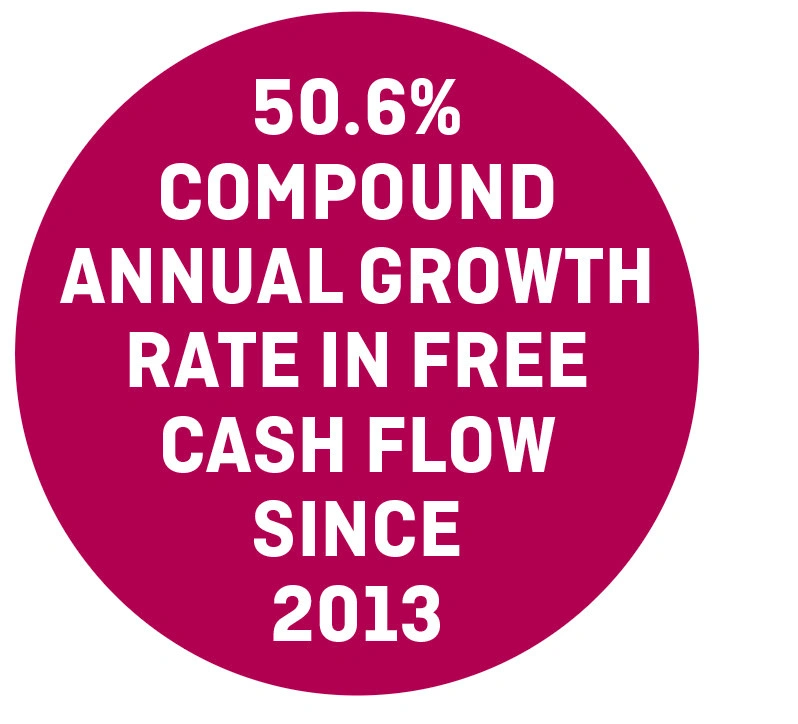

Panmure Gordon analyst Adrian Kearsey says investors have overlooked positive progression in free cash flow. As a reminder, dividends are paid out of free cash flow, so strength in the latter is good for the former.

Operational efficiencies and smart acquisitions have helped boost free cash flow from £6m in 2013 to £20.5m in 2016. The company now has plenty of cash to fund organic investment, dividends and further deals in a fragmented market.

UK-focused Epwin specialises in extrusions, mouldings and fabricated low maintenance building products. In the last 18 months it has acquired three businesses for a combined initial consideration of £42.2m.

The business derives around 70% of its business from the renovation, maintenance and improvement (RMI) market and the rest from new build and social housing.

Chief executive Jon Bednall notes the company has grown the bottom line every year since he joined in 2008. More recently Epwin has been able to manage an increase in cost inputs due to the devaluation of sterling.

Panmure has a price target of 185p which implies 63% upside from the 113.25p price at the time of writing.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

Editor's View

Exchange-Traded Funds

Feature

Great Ideas Update

Investment Trusts

Larger Companies

Money Matters

Smaller Companies

Story In Numbers

- 10 bagger: London Stock Exchange

- Most Popular Investment Trusts

- Most Popular Funds

- 255: WH Smith’s ever-increasing overseas exposure

- Zero: Hunting cannot provide earnings guidance

- Have UK employment levels peaked?

- Record ETF flows in the first quarter of 2017

- 76,230: Tesla largest US car maker by market cap