Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineNow is the ideal time to invest in Wilmington

We see an attractive value opportunity at professional information specialist Wilmington (WIL). Admittedly investors may have to be patient; although a 3.3% prospective dividend is a sweetener while you wait.

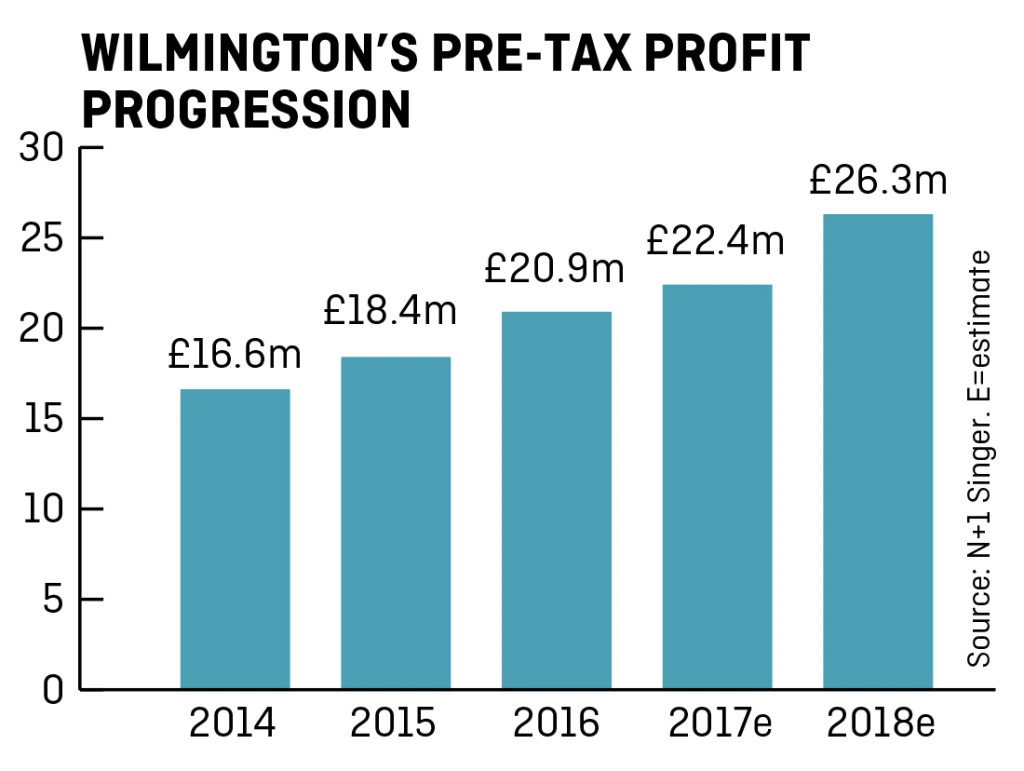

Based on forecasts from N+1 Singer, Wilmington trades on a June 2017 price-to-earnings ratio of 12.9 times but this falls to 10.9 times for the year to June 2018 as the benefits of its recent £19m acquisition of the Health Service Journal start to be realised.

The rating looks too cheap for a company with consistent profit growth. Indeed, N+1 Singer analyst Johnathan Barrett implies now is the ideal time to buy the shares for the first time or top up an existing holding.

Furthermore, we also note the stock has proved to be very resilient in the face of many market headwinds. For example, its shares didn’t collapse last year like many others amid Chinese debt concerns, Brexit or the election of Donald Trump.

Regulatory driven business

The company provides training and information services to highly regulated professions like law, finance, insurance and pharmaceuticals.

In the first half of its June 2017 financial year, 78% of its revenue came from subscription and repeatable information sales which helps support earnings visibility.

Under chief executive Pedro Ros, appointed in late 2014, the company has been pursuing a more integrated strategy with growing digital and international exposure (43% of sales are now derived overseas).

Restructuring strategy

We think its beefed-up ‘Sixth Gear’ programme of focusing on three key markets – risk and compliance, professional and healthcare – and abandoning its underperforming legal business makes sense and could help get the share price moving.

The company plans to dispose of its Ark division, which provides legal support services, and a formal sale process has commenced.

The aforementioned purchase of Health Service Journal, the UK’s leading health information, insight and networking business, from Ascential (ASCL) at the start of 2017 is expected to be earnings enhancing in its first full year.

A rise in net debt as a result of this acquisition will be partly mitigated by the £7m disposal of the leasehold on its previous head office in London (announced 4 May) and a move into a new site to be used by all of Wilmington’s businesses in the capital. (TS)

Wilmington (WIL) 252.02p

Stop loss: 200p

Market value: £220m

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.