Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineAbzena poised for big growth

Numis is excited about life sciences group Abzena (ABZA:AIM) ahead of its full year results on 13 June 2017, which is expected to reveal strong top-line growth of 40%.

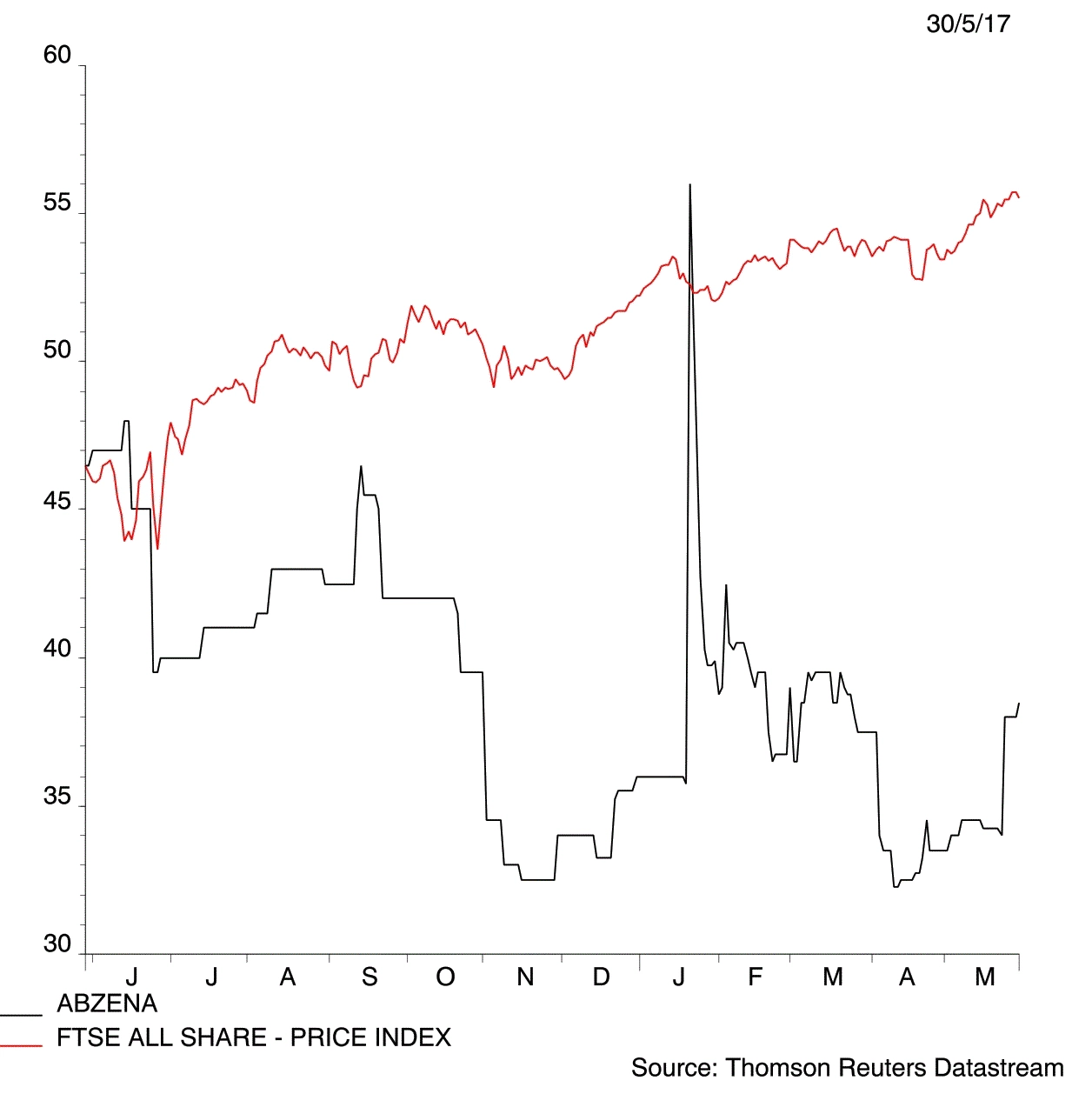

Stefan Hamill from Numis believes that investors can more than double their money over the next year with a target price of 93p. Abzena currently trades at 38.8p (26 May).

The company enhances the properties of pharmaceutical products to make them work more effectively through its Inside programme.

A popular programme

The programme is popular with twelve therapeutic antibodies currently being produced using its antibody humanisation technology. The antibodies are owned and progressed to clinical development by Abzena’s partners.

In April, the company raised £25m to upgrade its US biomanufacturing facilities so it can supply more products, as well as enhance its biology and chemistry offering in the US and UK.

Hamill predicts the expansion will increase its manufacturing capacity three-fold in 2018 and add further capabilities to help it deal with customer demand.

As a result, he has brought forward his forecast for a maiden profit to 2020.

The analyst is also optimistic that a ‘clear path to profitability’ will start to emerge when Abzena announces interim results in November.

On 24 May, one of Abzena’s partners, a clinical-stage biotech firm True North Therapeutics was acquired by Bioverativ for up to $825m.

True North produced its haemolytic blood disorder treatment TNT009 using Abzena’s antibody humanisation technology.

The acquisition is welcome news for Hamill as he estimates the overall sales potential from the Abzena Inside programme currently in the clinic will be approximately $10bn, up from $9bn.

One of the potential risks that Hamill highlights is pressure on earnings in the near-term as the company invests in its manufacturing capacity.

FinnCap analyst Alex Pye sees benefits from the acquisition of True North by Bioverativ and also sees potential for investors to double their money with a target price of 80p.

If True North successfully commercialises TNT009, Abzena will receive a small royalty, which Pye estimates is 1%.

A mark of quality

The analyst says: ‘TNT009 is the fourth Abzena inside product that has changed ownership through acquisition, with the last being Roche’s acquisition of Adheron Therapeutics in October 2015.’

The acquisitions of Abzena’s partners implies the quality of the products they are producing using the firm’s tech is attracting buyers. (LMJ)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.