Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

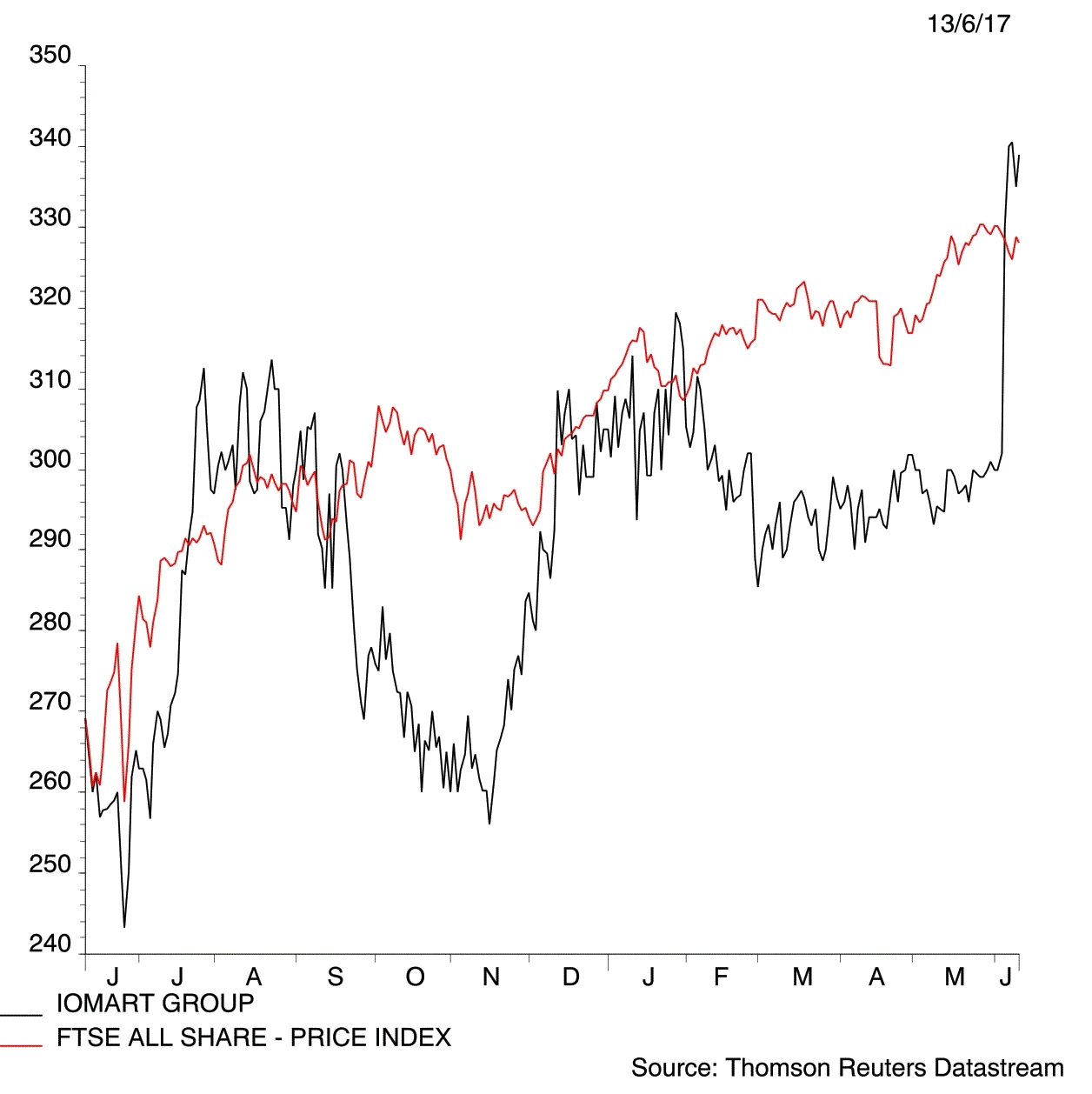

magazineIomart flexes value muscles again

Iomart (IOM:AIM) 325.25p

Gain to date: 25.8%

Original entry point: Buy at 258.5p, 23 June 2016

Another valuable bolt-on acquisition (Dediserve in Ireland), organic growth momentum, super cash generation and a 90% jump in the dividend are key stand outs of another excellent trading year for Iomart (IOM:AIM).

‘Textbook delivery,’ and ‘cash machine’ were among the remarks made by analysts and the company is comfortably on track to hit its £100m revenue and 40% EBITDA (earnings before interest, tax, depreciation and amortisation) margins by the end of the year to 31 March 2018 (EBITDA margin was 40.8% last year).

A dip in gross margins from 68% to 64% is most likely due to a modest fall off in consulting income and third-party cloud services supply (Amazon Web Services, for example) but we do not see this as a major concern.

Still among best cloud plays on the UK market. (SF)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

Editor's View

Great Ideas Update

Investment Trusts

Larger Companies

Main Feature

Money Matters

Smaller Companies

Story In Numbers

- 30% Shoe Zone’s sure-footed digital steps

- 72: WPP needs to plan for life after Sorrell

- Worst Performing FTSE Small Cap Stocks

- FTSE Small Cap Stocks

- Shareholders owning 18.4% of Gem Diamonds try to oust CEO

- Toople has lost three quarter of its value in a year

- 46,595 AIM stocks in demand

- Boohoo founder and family cash in £80m of stock