Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineCranswick’s tasty performance

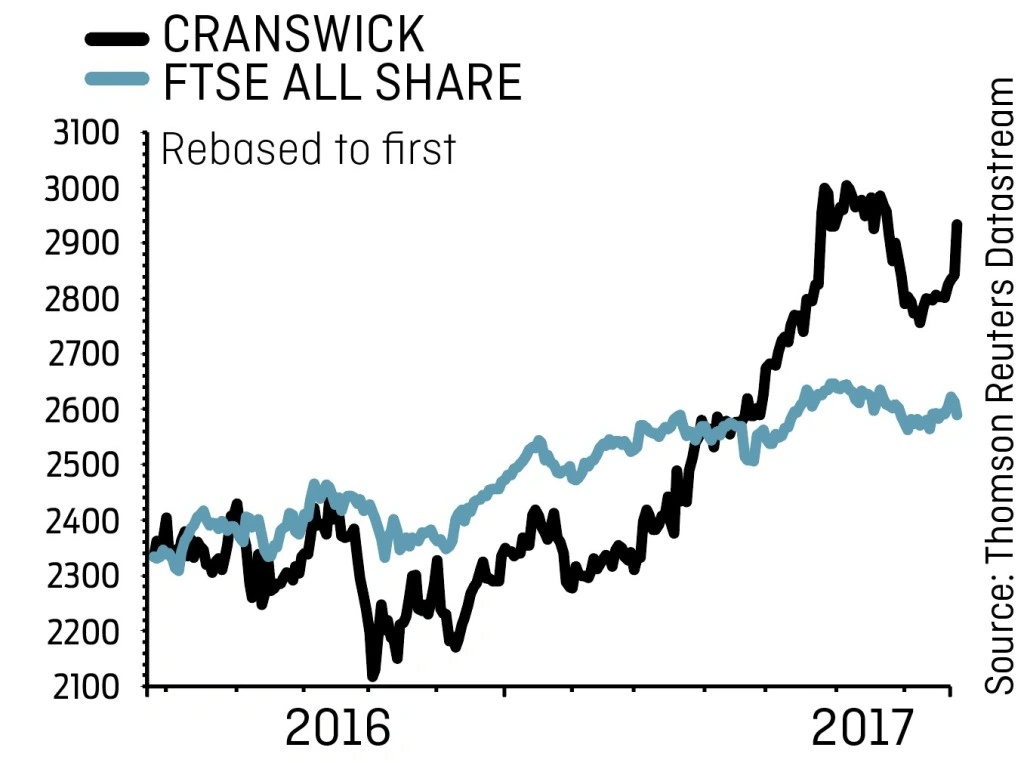

CRANSWICK (CWK) £29.32

Gain to date: 32.3%

Original entry point:

Buy at £22.16, 17 Nov 2016

Our bullish call on gourmet sausages-to-gammon supplier Cranswick (CWK) is now 32.3% in the money. The £1.48bn cap’s first quarter trading update (24 Jul) highlighted outperformance in a difficult UK grocery market over the three months to 30 June.

Total sales were up 27% and like-for-like revenue rocketed 21% higher, driven by strong domestic volume growth with all product categories making positive contributions.

Cranswick benefitted from the return of inflation in the pork category as well as from a new pastry contract and a new poultry contract, while the impact of rising pig prices was ‘partially mitigated during the period’.

With strong volume momentum continuing and new business wins expected to support growth in the second quarter and beyond, Shore Capital has upgraded its pre-tax profit forecast for the year to March 2018 by 2.2% to £83.3m.

The broker’s 2019 pre-tax profit estimate rises from £86.2m to £87.8m. Cranswick, a high-quality food producer whose dividend growth track record is formidable, is forecast to hike the payout to 48.9p (2017: 44.1p) this year ahead of 51.6p next.

We remain bullish about the high-quality food producer’s growth and income prospects.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.