Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

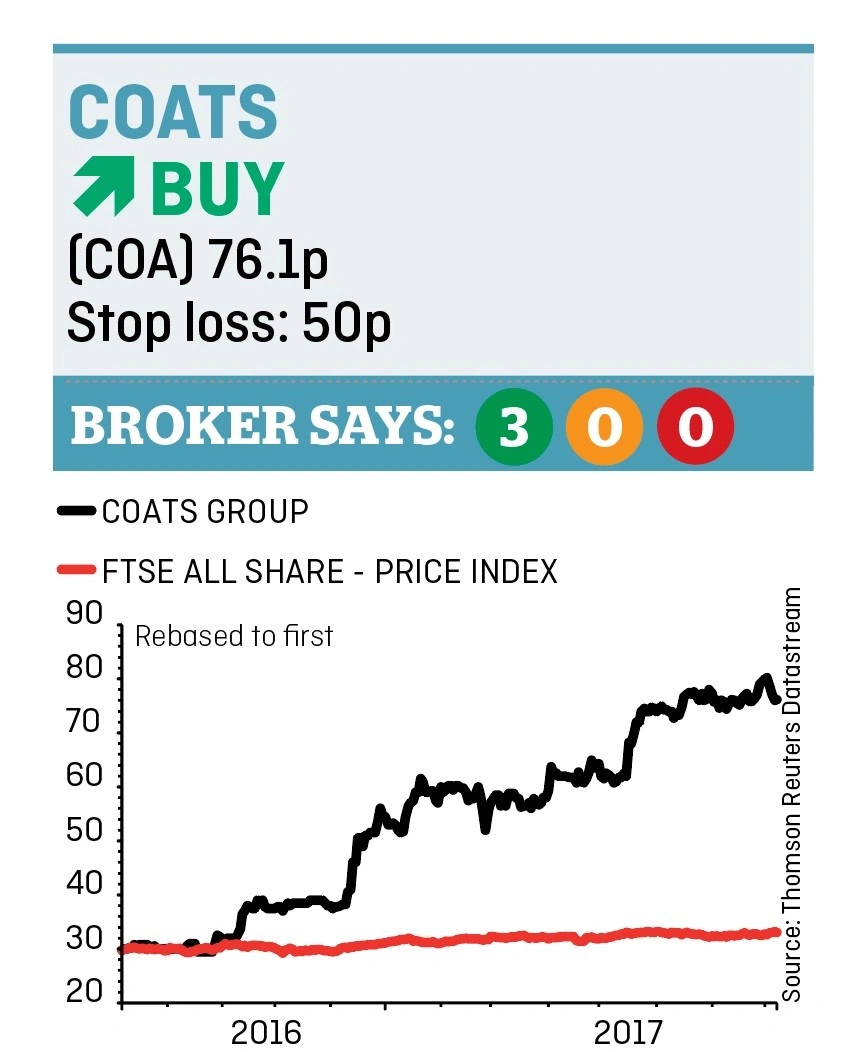

magazineThreads maker Coats is a superb investment

We’re confident the re-rating at industrial threads and consumer textile crafts firm Coats (COA) still has legs, so buy at 76.1p.

Sorting out a major pension problem and joining the FTSE 250 index have helped to propel the share price by three-fold in the past 18 months. The focus is now on driving up margins and driving down debt.

What does it do?

Coats is embedded in millions of people’s lives, even though they don’t know it. It provides the threads used to stitch shoes; its zips are used in trousers, jackets and dresses. It even provides threads and strings used in tea bags and also materials for vehicle seat belts.

This is a superb company growing profit each year and delivering a superior return on the money it invests in the business.

Return on capital employed has progressed from 24% in 2014 to 39% two years later. That’s well ahead of the 15% minimum level that many investors desire from a good business.

Its customers include Nike, Adidas, Ikea, Levi’s and Michelin. Coats has around 20,000 staff working across 60 countries.

Operating margins have been lifted from c7% to 11% and could reach even higher, according to investment bank Berenberg. It believes Coats could benefit from increased manufacturing automation, greater performance material thread sales and various self-help measures such as better procurement.

Berenberg believes Coats could sell its crochet-to-knitting yards Crafts division for potentially $80m to $120m. The division generates approximately 7% of group earnings before interest and tax and is viewed by the investment bank as non-core to the group.

We presume any proceeds from a sale, should it happen, could potentially be used for acquisitions or given back to shareholders.

What's the deal with the pension?

Coats earlier this year recommenced the payment of dividends after a five-year absence predominantly enforced by the UK Pensions Regulator.

The latter had concerns about Coats’ ability to fund its pension schemes and prevented it from returning capital to shareholders until a settlement had been made with the schemes. That’s now been sorted out, effectively drawing a line under one of the biggest distractions for management.

Operations are going well. Half year results published on 31 July were slightly ahead of forecasts at the pre-tax profit level. Notable strong performers were the apparel/footwear and performance materials divisions.

‘Coats continues to trade on an undemanding 8.5 times enterprise value to earnings before interest, tax, depreciation and amortisation (EV/EBITDA), which we do not believe reflects the potential in the business,’ says Berenberg. (DC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.