Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineCineworld is ‘lone shining star’ in leisure sector

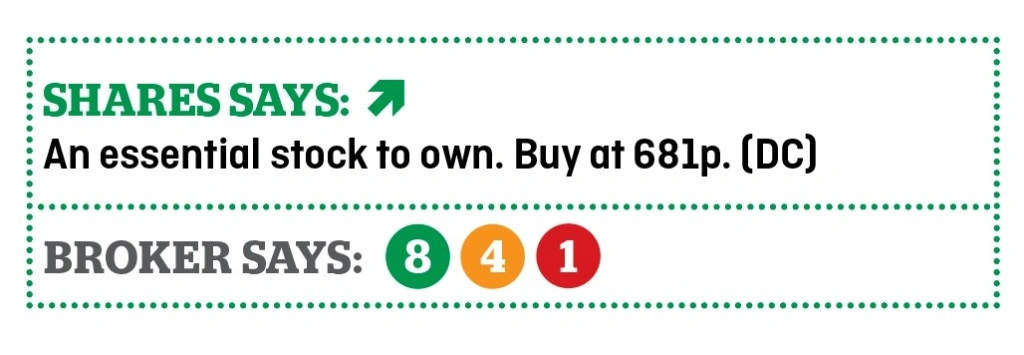

Cineworld (CINE) 681p

Gain to date: 7.8%

Original entry price: Buy at 632p, 16 March 2017

‘In a dull leisure sector Cineworld continues to be a lone shining star,’ says N+1 Singer analyst Sahill Shan. We agree, yet find it perplexing that the shares have drifted downwards since a very impressive set of half-year results on 10 August.

In those numbers, Cineworld reported 57.5% rise in pre-tax profit to £48.2m and a 15.4% increase in the dividend to 6p per share. Net cash generated from operating activities increased to £65.9m from £44.4m a year earlier.

Of great interest to us is the fact that Cineworld’s non-UK business had higher earnings before interest, tax, depreciation and amortisation (EBITDA) than the UK for the first time, showing a £44.3m performance versus £40m from the domestic territory.

Many people forget Cineworld operates in multiple countries and is not entirely dependent on UK consumer spending. It has overseas operations in Poland, Israel, Hungary, Czech Republic, Bulgaria, Romania and Slovakia.

‘Management has a stated ambition to continue consolidating the European cinema market with select accretive acquisitions. At 1.6x, net debt/EBITDA is well below the 2.5x that management is comfortable with, suggesting that M&A could be on the cards,’ says investment bank Berenberg.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.