Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy Asia Pacific may appeal to income investors

Global economic power has moved decidedly eastward to the world’s most populous region over the past few decades, China and India in particular. Growth and income hungry investors should therefore take a good look at the Asia Pacific region to see if it fits their risk profile, also factoring in investment time horizon.

Far East earnings are seeing their best trend in seven years. Equity valuations are attractive versus world markets and relative to the region’s own history, and dividend payments are growing at a rapid clip.

Asian companies have undergone a change; while growth in many instances has moderated, cash flow is strengthening and, in many cases, is being returned to shareholders in a rising tide of dividend payments that continues to boost regional returns.

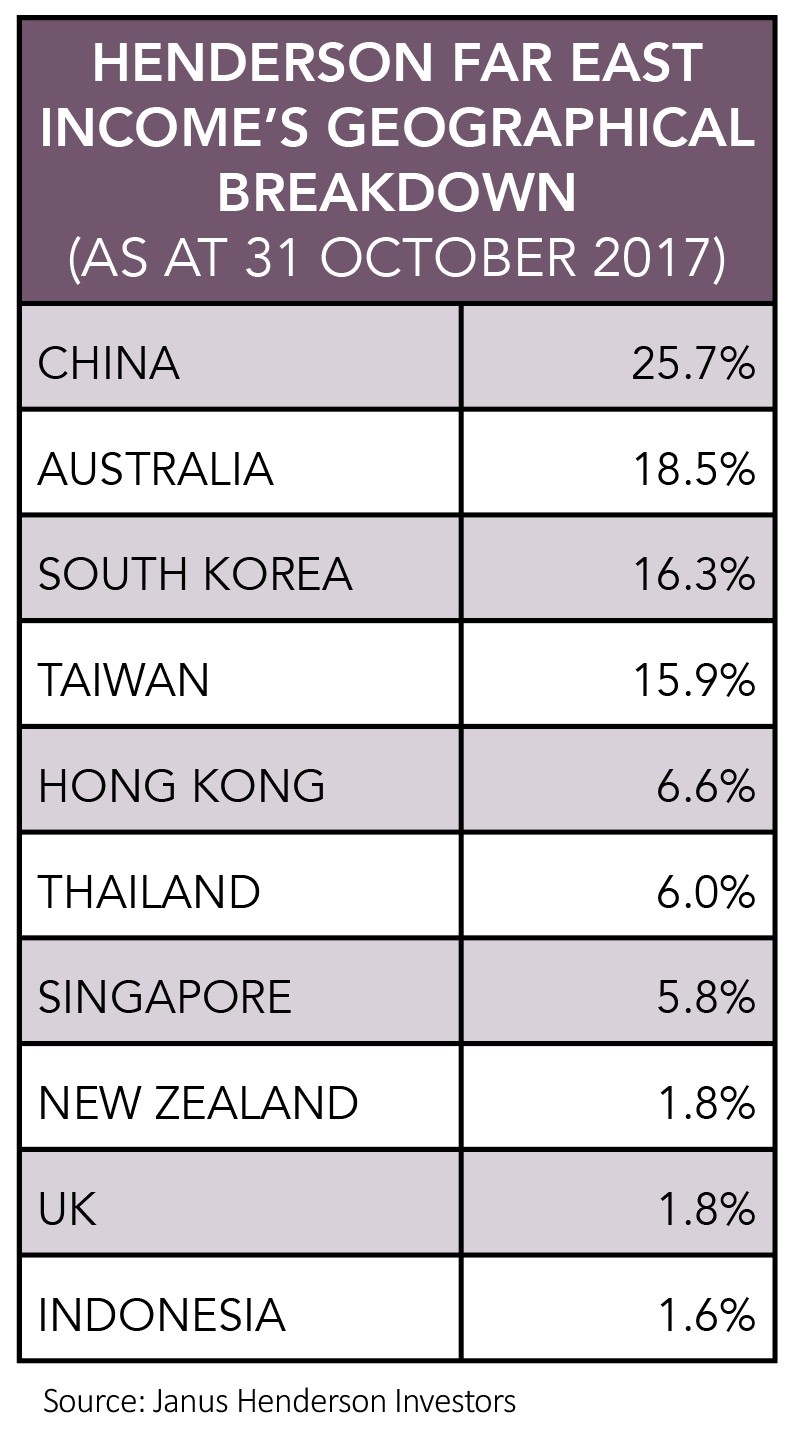

This is positive news for Henderson Far East Income (HFEL), a Janus Henderson Investors-managed investment trust whose objective is to provide shareholders with a growing total annual dividend, as well as capital appreciation, from a diversified portfolio of companies from the Asia Pacific region.

PERFORMANCE OVER PAST FINANCIAL YEAR

For the financial year to August 2017, the investment trust delivered an impressive net asset value (NAV) total return of 17.7% and a share price total return of 17.3% in sterling terms.

Although past performance isn’t a guide to how the investment trust will perform in the future, it is worth noting that the past financial year’s capital returns were all the more encouraging for not being boosted by weak sterling, as was the case in the strong previous year.

Investors were treated to a 4% improvement in the total dividend to 20.8p (2016: 20p), a distribution fully covered by the company’s revenue and increased ahead of UK inflation once again, indicative of fund manager Mike Kerley’s confidence in the growth and sustainability of Asian dividends.

In a year dominated by political, geopolitical and economic uncertainty, Henderson Far East Income’s positive returns reflected an improvement in the underlying fundamentals of the Asia Pacific region.

For the first time since 2009, Asian earnings have been upgraded since the start of 2017 rather than the previous trend of downgrades, thereby helping the Asia ex-Japan region outperform its developed market peers.

POSITIVE OUTLOOK FOR THE REGION

Kerley is cautiously optimistic on the medium-to-long term outlook for Asia Pacific ex-Japan. Speaking to Shares, he explains that while Asian markets have risen, valuations on a price-to-earnings basis have not changed markedly, because earnings growth has kept up with share price movements.

Kerley notes this is not the case with developed markets which are trading at, or close to, all-time highs, yet look fully valued since they lack the same kind of earnings support.

Price-to-earnings is a popular valuation metric and is calculated by dividing the share price by earnings per share.

Despite the strong performance in some of the expensive new economy sectors, the portfolio manager insists he’ll stick to his discipline of focusing on well-managed companies with attractive valuations which have the potential to sustain and grow their dividends in the years ahead.

As Kerley outlined at the company’s annual financial results (3 Nov): ‘Our focus remains on domestic orientated areas which are exposed to the improving spending power of the consumer across the region.

‘The outlook for dividends in Asia Pacific is still a compelling story. Asian companies have low levels of debt, a pragmatic view on capital expenditure and strong cash flow generation which should allow dividend payout ratios to continue to rise in the years ahead.’

The dividend payout ratio is the amount of dividends paid to shareholders relative to the total net income of a company. Investors should note that dividends aren’t guaranteed to be paid on a regular basis and dividend payments can go down as well as up.

LOOKING FOR DIVIDEND OPPORTUNITIES

Kerley is able to put money to work across the region, but he isn’t expecting too much growth from more mature markets in his investable universe, such as Australia and New Zealand, markets which already have pretty high dividend payout ratios.

‘The real opportunity lies outside of those in terms of dividend growth,’ he says, citing a 30-35% payout ratio for the rest of the Asia Pacific region, a ratio which has plenty of room to expand.

‘My view is that dividend growth outstrips earnings growth in Asia on a five year view, because I think payout ratios will rise,’ says Kerley, whose portfolio offers investors a compelling combination of dividend yield and growth.

Stocks in the portfolio offering a high yield today include the likes of Macquarie Korea Infrastructure, Digital Telecommunications, Mapletree Greater China Commercial Trust and National Australia Bank.

Dividend growth stocks in his portfolio, typically names where strong earnings growth is being translated into progressively rising dividends, include Samsung Electronics, the South Korean technology conglomerate which historically hasn’t paid dividends.

The smartphones, memory chips and televisions maker is becoming more shareholder-friendly and could double the level of its dividends in the next three years, according to Kerley.

Other dividend growth stocks in the portfolio include Dali Foods, a Chinese producer of snacks, energy drinks and soya milk based products, which boasts growing brand recognition backed by strong earnings, cash flow and dividends.

Another compelling dividend growth play part owned by Henderson Far East Income is Chinasoft. Kerley says the Hong Kong-listed software developer is moving into cloud services, adding that penetration of cloud computing in China remains quite small and implying significant scope for growth.

BOOSTING EXPOSURE TO CHINA

The investment trust increased its exposure to China in 2017, saying the country has the best combination of value, growth and dividend growth in the Far East.

‘We own banks, property, and consumer staples, as well as electric bus manufacturers and the owner of the hydro dam on the river Yangtze,’ he adds, referring to hydro-electric power producer China Yangtze Power.

Besides biggest position Samsung, Henderson Far East Income’s top 10 holdings include names such as China Construction Bank. It also has a stake in Bank of China, the corporate-to-personal banking services provider which is now the world’s largest bank by market capitalisation.

Shareholders in the investment trust are also gaining exposure to the cash flows of another market leader, namely Taiwan Semiconductor, the globe’s largest dedicated independent semiconductor foundry whose customers include tech titans Apple and Qualcomm.

‘The internet and tech sector globally have been driving markets,’ explains Kerley, who refuses to overpay for market darlings whose shares are priced for perfection.

Yet he makes the point that amid synchronised global economic recovery, investors may still be able to access growth without paying high earnings multiples for fast growth tech names.

The fund manager suspects 2018 will see investors start to look at value rather than growth stocks. ‘A switch to value would help us, because we do have a value bias in Henderson Far East Income,’ he remarks. (JC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Is Mothercare a takeover target after share price slump?

- Dialight banking on new leadership

- Coal hits one-year high

- Eco Atlantic gets Exxon discovery boost

- The week in a minute

- Christmas boost for grocers

- Which UK-listed stocks are affected by US tax reform?

- Where to invest your Worldpay takeover proceeds