Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineAmigo Loans distances itself from Wonga in bid to gain investor interest

The summer stock market float of Amigo (AMGO) brought the UK’s best known guarantor loan company to the London Stock Exchange with a market cap of £1.3bn.

Given the trouble of some companies in the sub-prime lending sector, notably Wonga, it is worth asking if all companies in this bracket, including Amigo, can be tarred with the same brush?

Amigo’s chief executive Glenn Crawford is quick to dismiss comparisons with payday lenders like Wonga, who have fallen foul of regulatory scrutiny in recent years. ‘We are a very different business to Wonga and there’s no read across to what’s happening to them,’ says Crawford.

Wonga was rocked by a series of compensation claims over improper sales practices and its customers are thought to still owe the company around £400m despite it being in administration. Amigo argues it does not have these problems as it targets a different part of the market.

WHO IS ITS TARGET CUSTOMER?

Described as a non-standard lender, Amigo’s rate of interest or APR is the middle ground between mainstream lenders and half of what sub-prime lenders are allowed to charge since reforms were introduced in 2015.

At 50% APR, the loans are by no means cheap but still a long way off the 100%+ that short term lenders often charge.

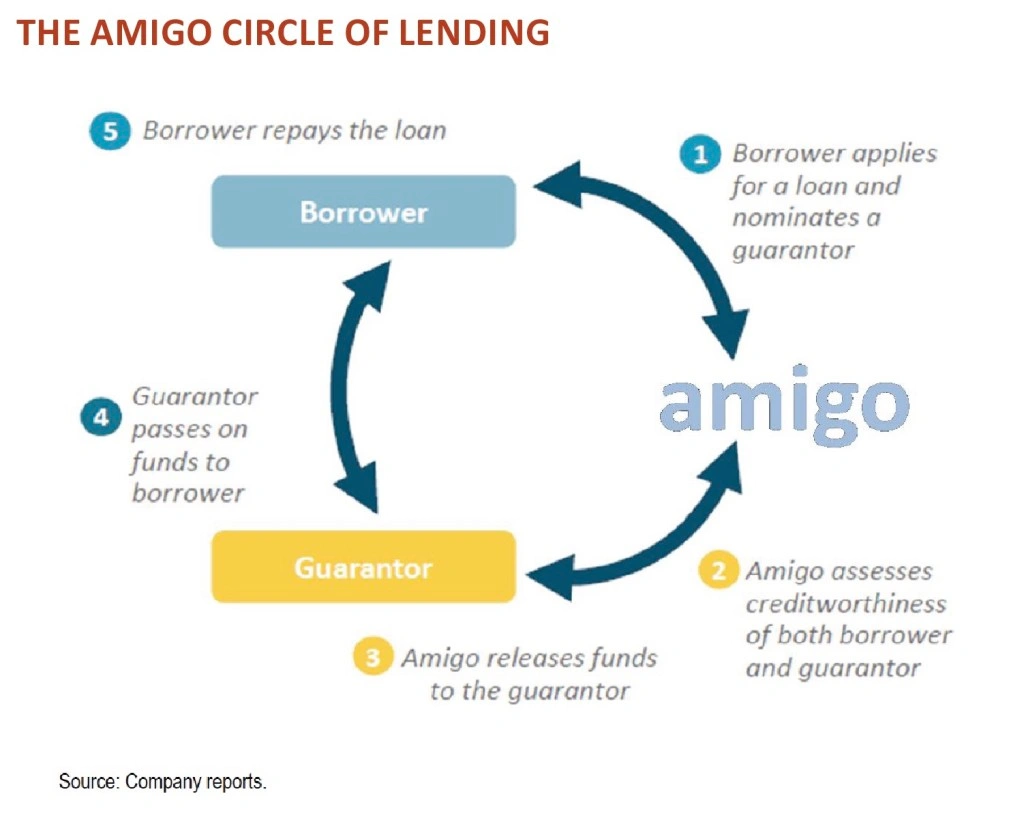

The company works by giving those excluded from mainstream lenders access to credit. The catch is that they need someone with a better credit history to guarantee the loan repayments will be paid. These guarantors will typically be a friend or family member.

Crawford says this is only part of the story as debt consolidation is another reason people use Amigo. He states that a quarter of its monthly lending is to allow people to consolidate more costly debts.

Amigo also caps the interest it charges, so if a customer gets into trouble they don’t get sucked into a spiralling debt vortex, the so-called ‘payday trap’.

Crawford says a number of the company’s customers have been prime borrowers in the past but a ‘bad event’ happened to them such as relationship breakdown or loss of job severely limiting their options and affecting their credit status.

‘We are a credit rehabilitation company and want to help rebuild credit scores and we don’t discourage people from moving away from us,’ says Crawford.

Even if customers do graduate from Amigo to more mainstream lenders, guarantor loans still account for just 0.4% of the UK unsecured consumer finance market according to a review by the Financial Conduct Authority in 2017.

With other parts of this market under regulatory pressure and traditional lenders retreating from the space, Amigo estimates there are 7.8m-9.8m potential untapped customers in the UK.

POLITICAL RISKS

Despite Crawford’s apparent desire to help people rebuild their credit and ergo no longer need his company’s services, it should remembered that Amigo is still the target of certain people’s ire.

Labour MP for Walthamstow, Stella Creasy has been a long-time critic of payday loan companies. She doesn’t distinguish between the likes of Wonga and Amigo, going as far to call the latter a ‘loanshark’.

In a recent article in The Sun by Creasy, she attacked the practices of high cost lenders and said ‘Amigo lets friends guarantee loans, so has two people to chase if the debt goes bad’.

Crawford says he tried to engage Creasy in dialogue but given the amount of money the company has spent on advertising, it may have inadvertently have made itself a target.

One reason that Amigo has such a dominant position in the guarantor loan market, with an 88% share, is its brand awareness.

But being a well known name clearly has its downsides as seen with Creasy’s attack on the company.

CASH MACHINE

Despite the downsides of being a whipping boy for left leaning members of Parliament, there’s no denying the strength of Amigo’s business model.

Releasing first quarter results recently, the company increased its revenue by 47% to £62.9m on a year-on-year basis. Its profit after tax only increased by 4% to £12.3m, and this disappointed investors as shown by a 6% price decline on the day. However, it is worth noting the profit figure was constrained by IPO costs.

A look at the company’s shareholder register suggests that institution investors believe the company is a winner. Names include Investec Asset Management, Woodford Investment Management and Janus Henderson Investors.

Amigo plans to pay out 35% of its post-tax profits as dividends and looking at forecasts from JPMorgan Cavenove, this equates to a maiden dividend yield of 2%, rising to 3.4% in 2020. Also given the share price slump following the release of its first half results, Amigo is trading on 12.3 times 2019’s 20.9p of earnings using market forecasts – an undemanding rating.

JPMorgan says: ‘The primary aim of this (guarantor) structure is to encourage repayment of the Amigo loan; this has proven effective, with less than 13% of payments on average over the past five years coming from guarantors.’

In other words because of the link to a close friend or family member Amigo’s borrowers don’t want to let guarantors down by not paying back the cash.

Amigo has spent a lot of money on advertising and this is part of the company’s efforts to create a high barrier to entry to its niche market.

While some companies have attempted to launch guarantor loan products, given that Amigo was first out of the stalls in 2005 it could take a long time for these rivals to catch up. (DS)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Investors braced for potential dilutive equity fundraise from Sirius Minerals

- Will Unilever exit the FTSE 100?

- Second worst September start for US tech stocks in 10 years

- Are UK markets finally ready to shed their Brexit discount?

- Share price decline implies Debenhams is at death’s door

- Is this the beginning of the end for Whitbread?