Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat would make the Federal Reserve change tack?

Regular readers could be forgiven that this column is obsessed with the issue of liquidity, not least because that is the case.

We have already looked at how central banks are draining it away and how issues such as capital controls could mean that investors must never assume that it will always be easy to buy or sell assets, owned directly or indirectly via funds, when, in the size and at the price they want.

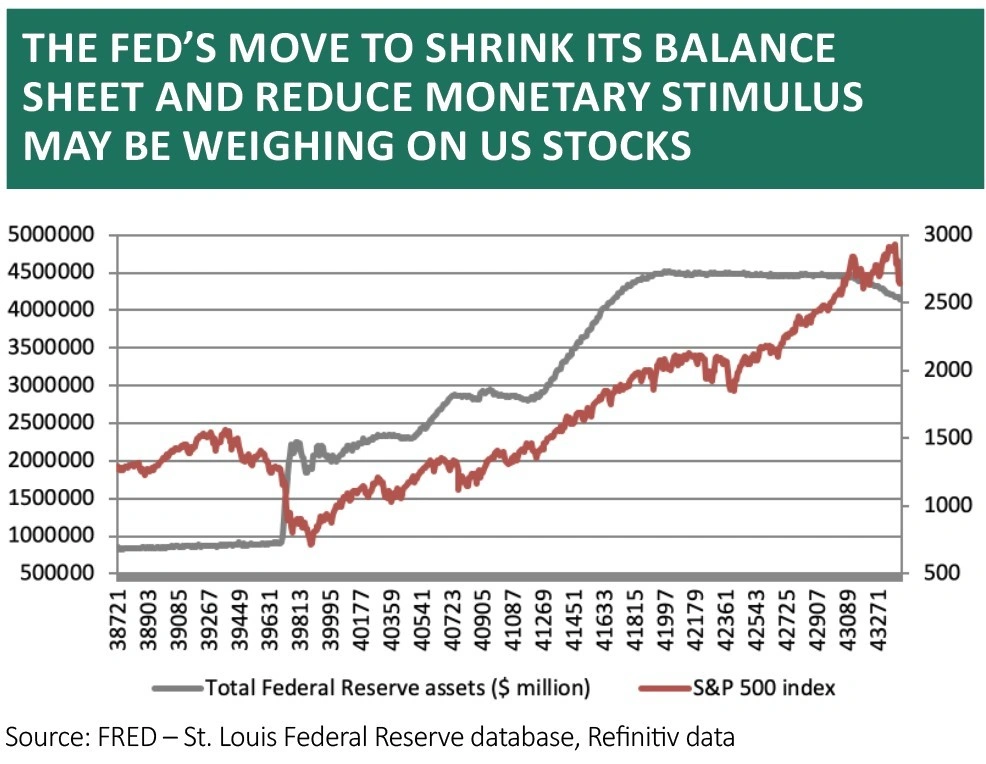

Now we must return to the issue of central bank policy because our warning that higher rates and less quantitative easing (QE) could provoke increased volatility does not seem too far off the mark, given the autumn stock market wobble.

The Fed has now reduced its balance sheet by some $351bn, or 8%, while the S&P 500 is some 7% off its all-time high.

This may be just a coincidence but it is enough to prompt complaints from no less than US President Donald Trump, whose willingness to measure his administration’s success by how high the US stock market goes may yet prove a poor choice of yardstick.

The President’s colourful accusations that his country’s central bankers are ‘loco’ and ‘going crazy’ articulate a deep-rooted fear in the markets that higher rates and less stimulus could mean lower share prices.

The Fed does not seem moved by such talk as yet, but this does beg the question of what might have to happen for the US central bank to stop tightening and start loosening policy once more.

DIFFERENT SCRIPT

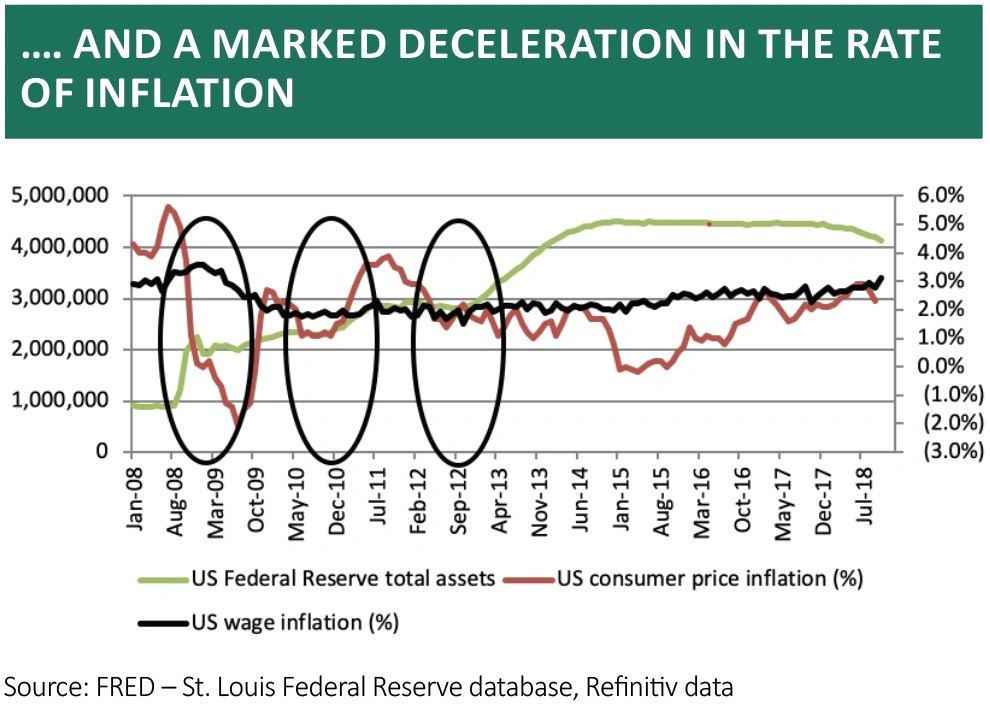

Fed chairman Jay Powell’s predecessors Ben Bernanke and Janet Yellen oversaw the launch of all three phases of the Fed’s QE scheme in November 2008, November 2010 and September 2012.

All three of those programmes came in the wake of a combination of stock market weakness, a sell-off in high yield (junk) bonds and a flattening in the yield curve (a decline in the premium yield offered by US 10-year Treasuries relative to two-year ones).

Powell seems to have a different outlook, given his 2017 quote that ‘it’s not the Fed’s job to stop people losing money’ and the US central bank’s recent suggestions that the yield curve is not as reliable an indicator as it once was.

If financial market indicators will not sway Powell and colleagues, then perhaps we have to look to real-world, economic ones.

THREE INDICATORS

This column has looked at US data to see which items may have influenced Fed thinking under Bernanke and Yellen.

Of the real-world ones, three areas seem to have tempted the US central bank to pull the monetary stimulus trigger in the past (the rings show when QE1, QE2 and QE3 were launched):

– Weakness in the Institute for Supply Management’s (ISM) manufacturing purchasing managers’ index (PMI)

– Weakness in the non-farm payroll data and a loss of momentum in job creation

– A slackening in the rate of inflation

The following charts illustrate these points, with the rings highlighting when each phase of QE came into effect.

The Fed has a twin mandate of employment and inflation. The latter has ebbed a little and the PMI has pulled back slightly from its peak but neither really has done so to the degree seen ahead of QE2 or QE3.

Moreover, US job creation is still strong, judging by the 250,000 new non-farm payrolls added in October and 3.1% wage growth.

Under such circumstances, the Fed seems unlikely to be deflected off course by increased asset price volatility. Financial markets are on their own.

Investors must decide whether momentum in earnings, cash flow and dividends are sufficient to justify prevailing valuations and compensate them for the specific risks that come with individual asset classes and geographic regions, because there is no longer enough cheap money around to lift all prices on a tide of liquidity.

Russ Mould, investment director, AJ Bell

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- What the US midterm election results mean for markets

- Aberdeen plans global private-market sustainability trust

- UK metal bashers are facing uncertainty as Brexit looms

- Trustpilot IPO could provide big bucks exit for seed backer Draper Esprit

- Living wage increase: which stocks are most impacted?

- Investors see value in emerging markets

- Why isn’t the oil price surging on Iran sanctions?