Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTechnology fund expert who’d been slicing Apple long before the warning

Leading technology fund manager Ben Rogoff had been cutting back on his appetite for Apple long before the consumer electronics giant’s shock profit warning (2 Jan).

The respected manager of the Polar Capital Technology Trust (PCT) has become increasingly wary of potential threats to the Cupertino giant’s iPhone sales volumes against a backcloth of aggressive trade rhetoric from both the US and Chinese governments.

Apple chief executive Tim Cook has tried various ploys to patch potential leaks from his company’s earnings from global smartphone saturation. This has included schemes like launching an array of new and more expensive handsets, cranking up its services revenues from streaming music, apps and much else, plus enormous share buybacks, for example.

ALARM BELLS RING

This came to a head just two days into 2019, the company reporting the grim news that its revenue and earnings numbers would be lower than it had forecast at the last quarterly earnings report in November.

Apple blamed faltering sales in Asia, particularly in China, for the adjustment, but the share price tanked, losing about 10% of their value to $144.04.

Adding to Rogoff’s concern was Apple’s controversial decision last year to stop telling investors how many iPhone units were shipped, seen by many commentators as a slap in the face for transparency.

Being seemingly ahead of the curve should be, at least partially, satisfying for Polar Capital investors. Back in August 2017 Apple ranked as the investment trust’s second largest holding, with 7% of its funds tied up in the smartphones designer.

Today the stake is 5.4%. That remains sizeable (Apple is still Polar Capital’s third biggest investment) yet our back of note book calculations suggest that more than £17m of net assets have been funnelled out of Apple and into other investments during that 17 month spell.

Critics might say that this still leaves the trust with egg on its face. A 5.4% net assets stake in Apple implies that something close to £9m of the trust’s value was eaten away by the Apple warning.

Rogoff sees Apple’s cast iron balance sheet as a major positive for the company going forward, backed by a $237.1bn cash pile (as of 1 November 2018) that will continue to fuel share buybacks.

But the manager also remains ‘benchmark aware’ to its Dow Jones World Technology Index, which means some very large technology stocks simply must be owned.

WILLING TO LOOK BEYOND THE BENCHMARK

But it is encouraging that Rogoff shows a distinct willingness to look beyond the benchmark in his stock selection when he can to gain access to the very best long-term growth opportunities, as any active fund manager should look to do.

It is a strategy that stands up to performance scrutiny. Overweight holdings (meaning they are a higher proportion of the trust than in the benchmark) such as chip maker Advanced Micro Devices and software stocks like Alteryx, Twilio, New Relic and Hubspot joined better-known names (Amazon, Dropbox, ServiceNow) to significantly bolster the half year performance to 31 October 2018.

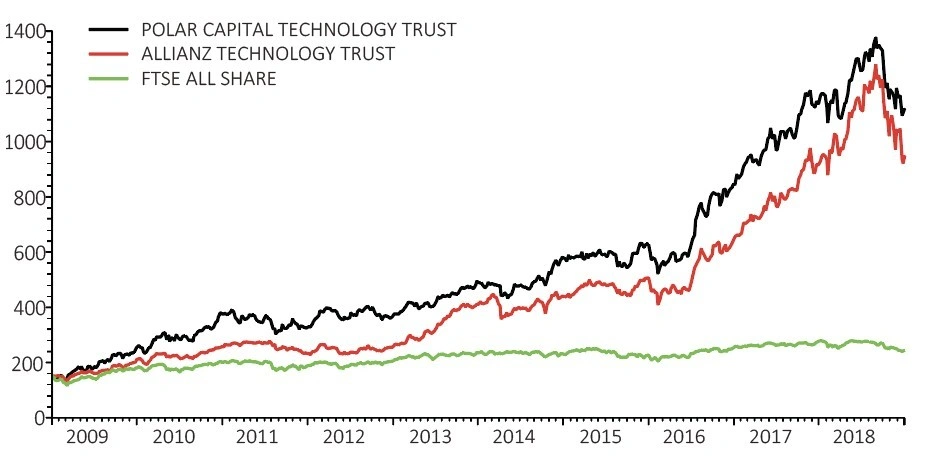

During that six-month trading period Polar Capital saw its net asset value (NAV) increase 8.5%, about a fifth better than the 7% of the Dow Jones World Technology Index.

Yet the trust’s share price has, perhaps understandably given concerns for global stock markets and growth, continued to struggle, falling about 17% since ‘Red October’s’ sell-off kick-in.

That leaves the stock changing hands now at £11.10. The share price discount to NAV had widened to 6.5% at 31 October, although it has since narrowed again to about 3%, more in line with its 10-year average of 3.8%, according to Winterflood data.

NEXT DISRUPTIVE TECH CYCLE

While recent months have seen an extreme spell of volatility across technology markets Ben Rogoff remains as chipper about the long-run prospects for select technology themes as ever, flagging cloud computing, software-as-a-service, digital marketing, complex microchips and robotics/automation as some of his pet favourites.

‘Ben Rogoff makes a compelling case for the continuing emergence of the next technology cycle and the disruptive effect that it is having on many of the sector’s existing large cap incumbents,’ points out Emma Bird, analyst at Winterflood.

It has certainly worked in the past. Over the last 10 years the fund has delivered a NAV total return of 551%, smashing the 423% return of the Dow Jones World Technology benchmark. That’s also modestly better than its closest UK–listed peer, the Walter Price-run Allianz Technology Trust (ATT) at 534%.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.