Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineRPS outlines plan to win back investors’ interest

For a professional services firm operating in 125 countries across the world and turning over £600m in annual revenue, RPS (RPS) flies under most investors’ radar.

Chief executive John Douglas aims to change that, starting with a brand overhaul and the appointment of a new group director of strategy and a chief information officer.

SAFE PAIR OF HANDS

A civil engineer by training, Douglas was chief executive of Australian engineering consultancy Coffey for five years prior to taking the top job at Abingdon-based RPS in September 2017.

Before running Coffey he spent 15 years at industrial firm Boral including managing its largest business.

He describes RPS as ‘having good bones’ but in need of an image and IT overhaul so that the business can continue to grow in an increasingly digitally-enabled and rapidly-changing marketplace.

CHALLENGING MARKET PERCEPTIONS

RPS is perhaps best known among investors for its environmental consulting work which has made it a firm favourite with environmental, social and governance (ESG) funds over the years.

However it is also known for its energy consulting business which tends to ebb and flow with the fortunes of its customers, the big oil and gas companies, which rely on commodity prices to dictate where and when they spend.

When times are good energy consulting is a great business, when times are bad RPS shares can suffer harsh treatment.

Part of Douglas’s challenge is to connect with investors and draw their focus onto the other parts of the business which are less cyclical.

CHANGING FROM THE INSIDE

In the past RPS proudly claimed that it had over 200 businesses worldwide which didn’t help investors or analysts trying to get to grips with the firm.

In July last year the firm announced a new segmentation to better reflect how the businesses are actually managed.

The company now offers services in six sectors: property, energy, transport, water, resources, and defence and government services.

Across these sectors it provides planning and approval, design and development, project management, advisory and management consulting, health, safety and risk, laboratory services and training, among other services.

BUMPY START FOR THE REBRAND

Last October RPS announced that it would take a one-off £2m hit for the corporate re-branding and that there would be additional ‘ongoing’ costs of £2.5m a year.

In addition the firm is investing £14m in a new planning system which doesn’t go live until 2021.

It cautioned that as a result of this spending profit for 2018 and 2019 would be well below market estimates, triggering a 27% collapse in the share price.

It also warned that the exodus of senior staff from some of its acquired businesses had continued, casting doubt over revenue projections for its environmental business in particular.

EXPECTATIONS HAVE BEEN RESET

After this disappointment analysts lowered their 2018 earnings forecasts to around £50m, and last week RPS confirmed that it expects £50.2m of full-year profit.

Douglas points to the firm’s healthy margins, excellent cash conversion and robust balance sheet, reassuring investors that the investments which have dented the profit line will make RPS ‘an even better business in the future’.

With 2019 profit expectations also in the £50m ball-park we suspect that the chief executive has set the bar low enough that RPS shouldn’t have too much trouble at least matching it.

EXPANDING THROUGH M&A

Having been an avid acquirer in the past, especially in the US, RPS has become very quiet on the acquisition front.

It looked at a number of potential US acquisitions last year but decided to pass due to high vendor valuations.

However this month the company surprised the market with a deal to buy Australian transport advisory consultancy Corview for A$32m, which includes A$2.1m of cash used for working capital.

Corview is a leading player in the New South Wales and Queensland transport consultancy market and generated A$17.1m of turnover in the year to June 2018.

Transport is a key market for RPS and as well as adding depth to its Australian business it brings a strong brand and important public sector relationships.

Given that Corview’s pre-tax profit last year was A$5.1m, the price tag is less than six times earnings excluding the cash on balance sheet making it an attractive deal and one which should add to earnings this year.

A MORE BALANCED BUSINESS

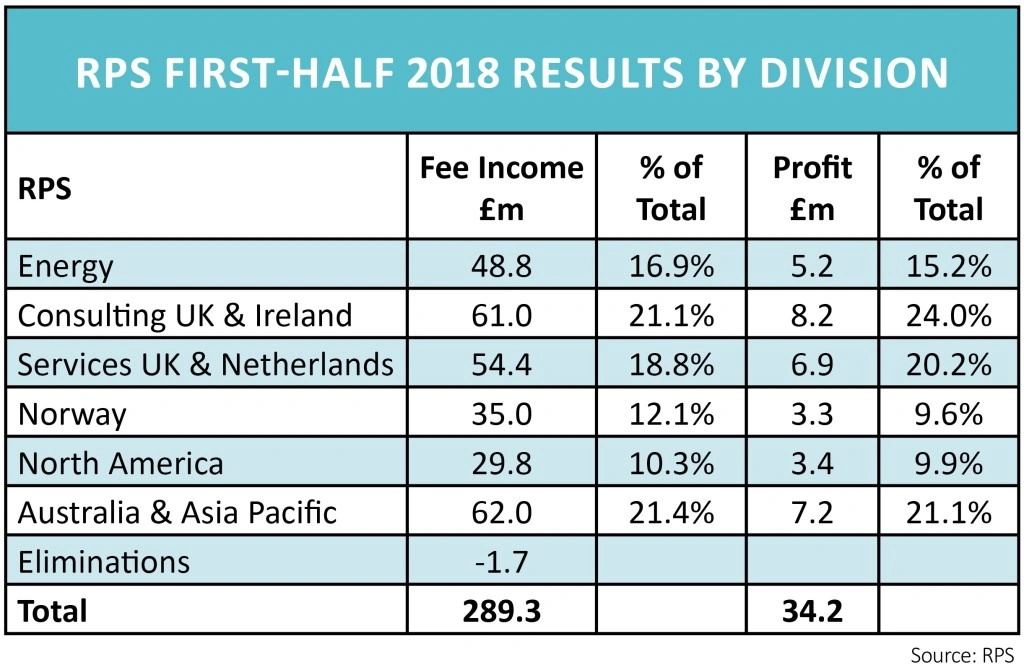

RPS is no longer as exposed to the energy sector as it was historically.

At the half year stage fee income from energy was just under 17% of the group total compared with more than twice that level at its peak in 2014.

The biggest drivers are now consulting and services in the UK, Ireland and the Netherlands, along with its businesses in Australia and Asia Pacific.

In theory a smaller contribution from the energy sector should mean that the predictability of earnings improves and with it a smoother ride for the shares.

In the meantime investors can pick up a 6% dividend yield so to an extent they are being compensated for waiting while the chief executive’s new strategy beds in.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.