Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFive stocks in trouble

A contrarian investor looks for unloved assets and buys them cheaply in the expectation that sentiment will change and he or she will be able to bank a healthy profit.

This is not an easy thing to do. Most of us prefer the comfort of falling in with the crowd. Sticking one’s neck out, particularly when your own cash is at stake, takes nerves of steel.

In this article we examine five businesses which are out of favour with investors – something which is reflected in bombed-out share prices. We look at what the market is concerned about and the changes which need to be made to win people over.

WHAT DO CONTRARIANS LOOK FOR?

A contrarian will look for signs that negative factors have already been priced in by the market.

They will also look at balance sheet strength, namely weighing up cash against liabilities. A contrarian needs to know a company can at least survive long enough for its fortunes to turn around.

A company lumbered with significant borrowings could either go bust or face a radical financial restructuring which leaves little upside on the table for existing shareholders.

Shopping centre investor Intu Properties (INTU) might look like an obvious candidate for a contrarian call. Its shares are at roughly a third of the level seen two years ago and it is hard to think of an asset class which is more unloved at the moment than retail bricks and mortar. Intu trades on just 0.36 times Liberum’s estimated 2019 net asset value.

Meanwhile the appointment of a new chief executive to replace the departing David Fischel could in theory act as a catalyst for

the shares.

But – and it’s a big but – Intu has £4.87bn worth of debt. It has already cancelled its dividend and if the value of its assets continues to fall then lending covenants could be tested.

With these examples in mind we now look at five companies sitting in the doldrums. Our analysis should stimulate your research process and show you how to think about stocks that the market doesn’t like.

Aston Martin Lagonda (AML) £11.32

WHY ARE THE SHARES DOWN?

You don’t have to dig deep to spot the multiple reasons for the dark market mood enveloping luxury sports car maker Aston Martin Lagonda (AML).

Brexit and the free flow of car components to and from Europe remains a major headache for all UK-based automotive operators. Aston also has to juggle massive investment for growth versus weakening profits, even after stripping out one-off costs from its IPO last year, and threadbare underlying cash flows despite selling more cars than ever.

The stock has got a lot cheaper since landing on the UK stock market with a toppy-looking valuation of £4.3bn and a £19 share price. The current price of £11.32 implies a 40% decline in six months which is significantly worse than the FTSE 100’s 5% equivalent fall.

HOW CAN IT WIN BACK THE MARKET’S FAVOUR?

A record 6,441 Aston Martin models were sold last year (26% gain year-on-year), with ever greater sales in North America and China encouraging for the company’s production push to 14,000 by 2022.

Aston’s development plan has stabilised the business and is now designed to expand the product portfolio and sell more motors.

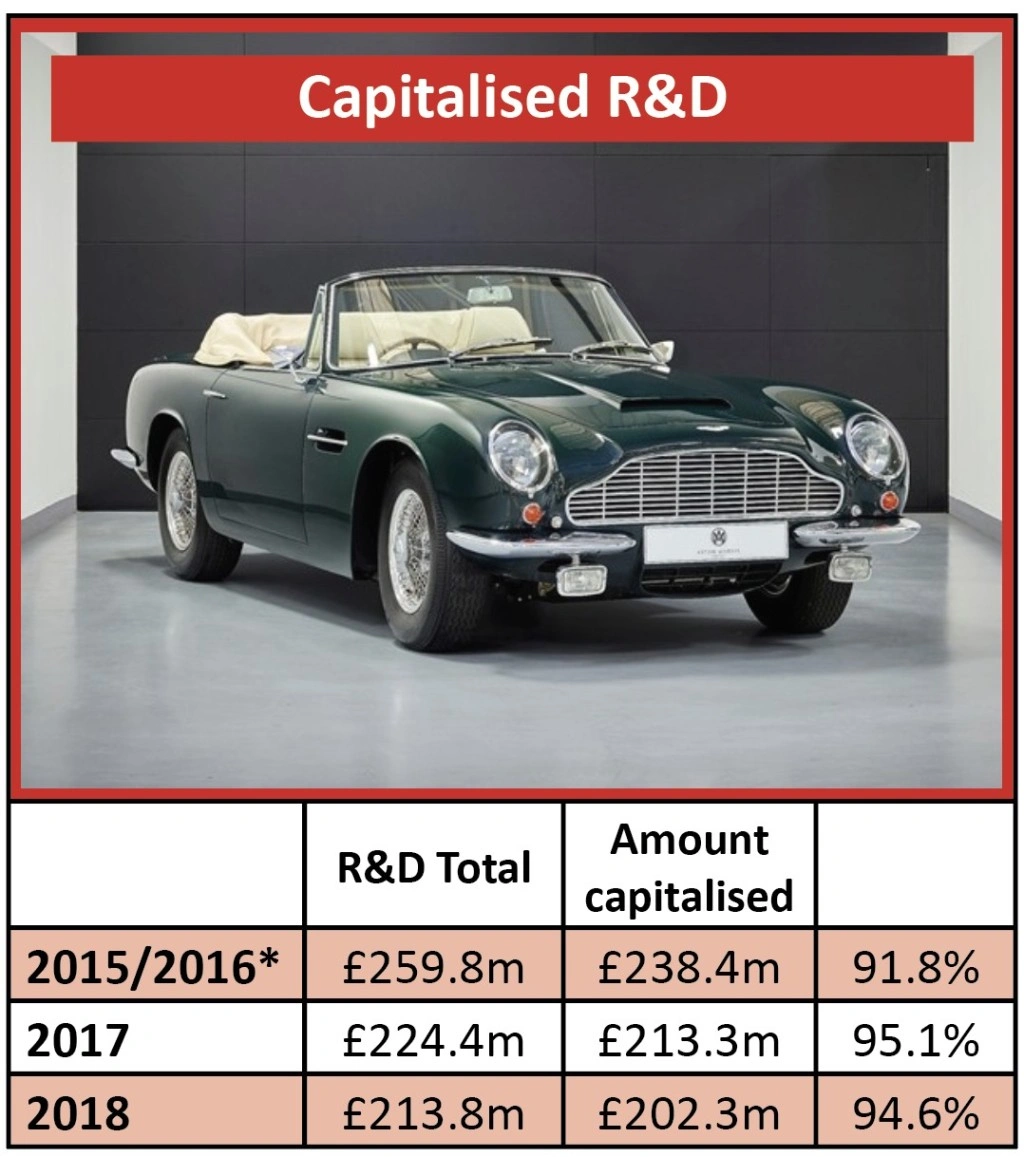

Here lies the challenge to the immediate investment case. New models require huge upfront investment to stay ahead of the technology curve, especially in the luxury space where Aston operates. Last year it spent £213.8m in research and development (R&D), yet 95% of that was capitalised, keeping it off the profit and loss accounts.

Companies are allowed to do this when they can demonstrate a clear benefit to the business down the line but this is not always possible. Aston Martin has always been fairly aggressive in this regard although within the rules. Ferrari, for example, expenses about a quarter of its R&D.

On top of new models the company also has to grow its current 162-strong worldwide dealer network and seed the necessary marketing to catch prospective buyers’ eyes.

WHAT DO ANALYSTS SAY?

Cash of £144.6m sits on the balance sheet but Aston Martin is actually £560m in the red when bank loans are taken into account, about 2.3-times EBITDA (earnings before interest, tax, depreciation and amortisation) which is the measure closely watched by lenders.

Analysts at Numis Securities don’t forecast positive free cash flow from the business until 2021. Could that imply extra funding will be required from investors in the future? That’s a possibility and one that may hang over the share price until being resolved one way or the other.

Funding Circle (FCH) 371p

WHY ARE THE SHARES DOWN?

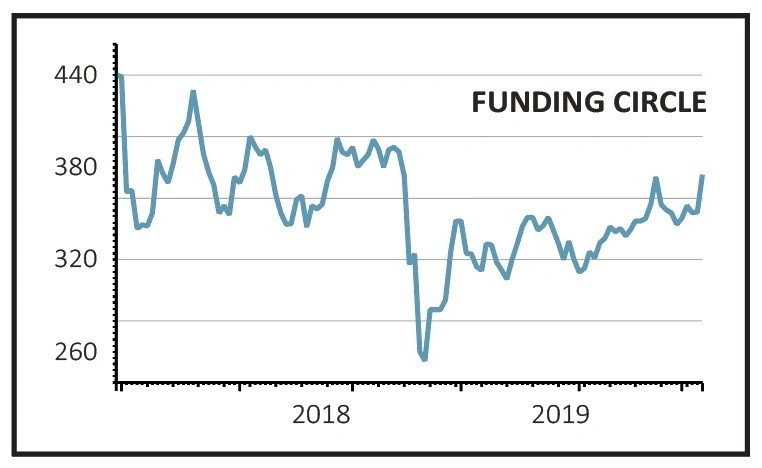

Business lending platform Funding Circle (FCH) floated last year at an issue price of 440p, raising £300m and valuing it at £1.5bn.

Chief executive Samir Desai described the firm’s market debut as ‘an exciting new chapter for the business as we seek to create a better financial world for small businesses and investors’.

Unfortunately, the first day of trading on 2 October was exciting for the wrong reasons with the shares sliding nearly 20%.

Concerns had been raised before the IPO about the mooted valuation given that Funding Circle only generated £94.5m of revenue in 2017 and racked up pre-tax losses of £36m due to heavy advertising spending.

While growth in the first half of 2018 was impressive – revenue was up 54% to £63m and it lent over £1bn to small and medium enterprises (SMEs) – free cash flow was negative to the tune of £35m and the company was nowhere near turning a profit.

The chief executive stressed that Funding Circle is ‘a very ambitious company’ but investors were clearly unhappy about the amount of cash it was burning through to achieve its ambitions.

HOW CAN IT WIN BACK THE MARKET’S FAVOUR?

The 6% rally in the shares in response to the 2018 full-year results last week suggests the market is starting to come around but there is still a long road ahead.

Revenue was above the guidance given at the IPO at £142m with strong loan growth in the UK and the US. Net lending on its platform to UK SMEs last year was greater than all the high street banks combined and its US platform is now among the 50 largest US SME lenders.

So in terms of growth the firm is delivering, but free cash flow is still negative and rising so 2018 pre-tax losses were higher than 2017’s number.

WHAT DO ANALYSTS SAY?

Analysts are firmly on the fence with four ‘hold’ recommendations, one strong ‘buy’, one strong ‘sell’ and an average price target of 369p.

Numis likes the stock for the revenue growth and the potential to increase margins as it increases in scale. It has a fairly punchy 523p target price.

TechMarketView on the other hand is floored by the company’s spending on people and advertising and wonders if the company will ever turn a profit.

GLENCORE (GLEN) 305p

WHY ARE THE SHARES DOWN?

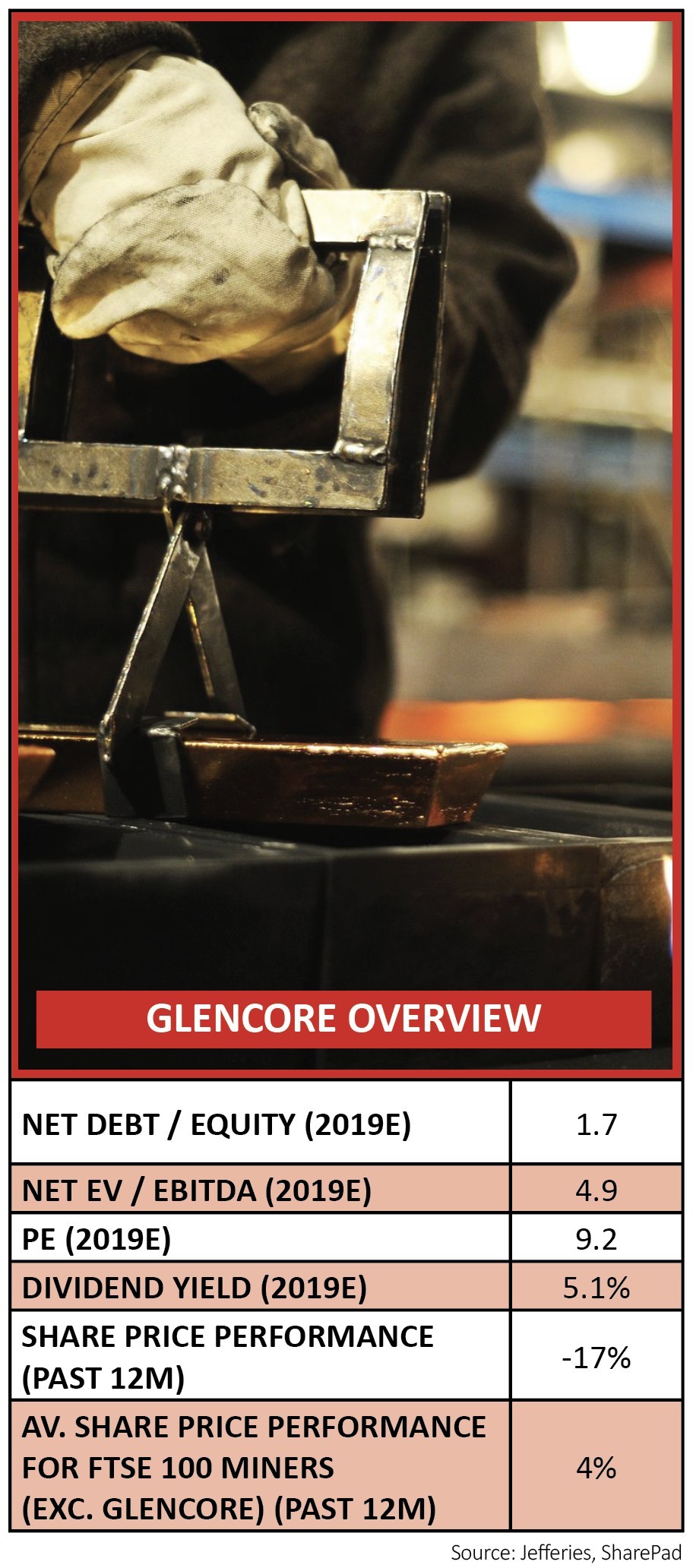

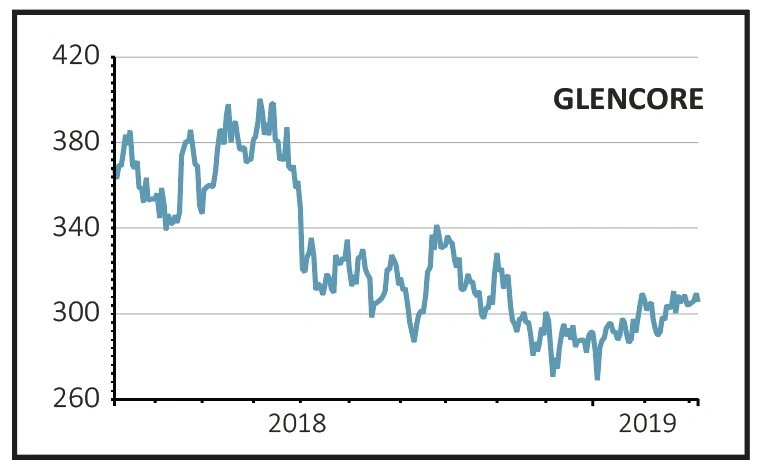

Shares in FTSE 100 miner and commodities trader Glencore (GLEN) have lagged every other diversified London-listed miner over the past year for a number of reasons.

It was ordered last summer by US authorities to hand over documents relating to a money laundering probe, prompting investors to panic.

A new mining law in the Democratic Republic of Congo (DRC) – where it has numerous interests – pushed up royalty rates, made taxes more punishing and placed restrictions on the repatriation of profits.

Glencore’s exposure to coal has also been a negative in the eyes of many investors who are increasingly paying more attention to environmental, social and governance factors. There are also concerns about a structural decline in coal usage and how that could weaken the commodity price longer term.

HOW CAN IT WIN BACK THE MARKET’S FAVOUR?

The US Department of Justice probe into money laundering is expected to take at least two more years to complete, thereby creating a major overhang on the shares.

Miners in the DRC have been trying to fight the new mining code and any success in reducing its severity would certainly act as a positive share price catalyst for Glencore.

The company last month said it would put a cap on its coal activities. While that may pacify some investors, it still doesn’t remove the fact that Glencore remains a large coal producer.

Perhaps a more realistic near-term potential catalyst for the shares would be a rally in the copper price as Glencore is one of the world’s biggest miners of the base metal, producing around 1.5m tonnes a year.

And an amicable resolution to the US/China trade war would be positive for commodity producers in general and act as a tailwind to Glencore’s shares.

WHAT DO ANALYSTS SAY?

Christopher LaFemina at investment bank Jefferies says shares in Glencore are worth buying ‘due to its inexpensive valuation, ongoing capital returns, resilient trading business, and leverage to prices of copper and coal.’

He expects the company to continue returning capital via dividends and share buybacks and to pay down debt. Large acquisitions look unlikely for now.

‘Glencore should continue to benefit from its resilient trading business,’ he adds. ‘On our estimates, the trading business accounts for up to a third of the company’s earnings before interest and tax.’

GoCompare (GOCO) 73.9p

WHY ARE THE SHARES DOWN?

Having been spun out of Esure and become a separately-listed company in November 2016, price comparison site GoCompare (GOCO) reached a peak of 143p in summer 2018.

During that period it fought off a takeover offer from property portal Zoopla and expanded in the energy price comparison industry.

Its shares have been in a falling trend since last summer as declining motor insurance premiums saw fewer motorists switch providers. GoCompare also saw its market share decline and suffered slowing revenue. This partially reflected a drive for advertising efficiency and higher margins which the market believes not unfairly will come at the expense of growth.

Equally as important was chatter that Amazon was preparing to disrupt the price comparison market – although nothing has come of that to date.

HOW CAN IT WIN BACK THE MARKET’S FAVOUR?

Central to the company’s strategy is delivering so-called ‘savings as a service’. To this end the company has launched WeFlip – a fully automated utilities switching service. The company will have to invest heavily in marketing in order for the service to gain traction, but the plan is for it to take in other areas like insurance and financial products.

Success with WeFlip could increase the predictability of earnings, boost growth and transform sentiment towards a business which currently trades on an undemanding 8.2 times forecast 2019 earnings. An investor day on 20 March is likely to spell out GoCompare’s plans for WeFlip in more detail.

The company recently received a vote of confidence from its chairman and insurance entrepreneur Peter Wood who increased his stake from 25.6% to 29.9%.

WHAT DO ANALYSTS SAY?

Berenberg’s Edward James believes WeFlip could be transformative for GoCompare as it ‘(1) addresses the underserved “infrequent switcher” user segment; (2) improves customer retention and switching rates, leading to higher user life-time value; (3) shifts the revenue model from one-off transactions to recurring switching revenue streams; and (4) reduces user acquisition/retention costs’.

However, he also cautions that WeFlip will take time to build up and will require significant upfront investment – cutting his 2019 earnings forecast by a third to reflect this thinking.

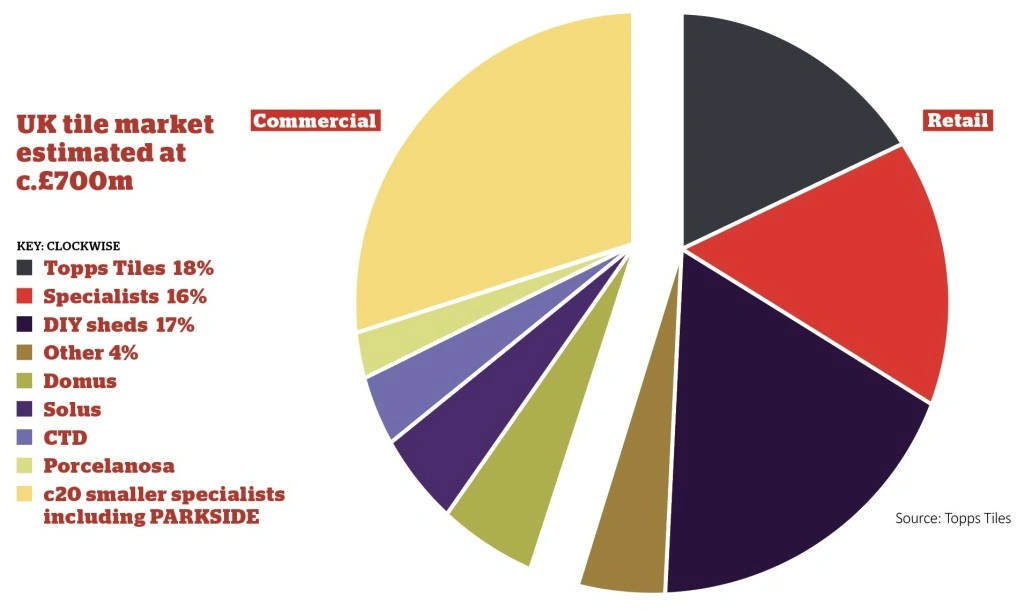

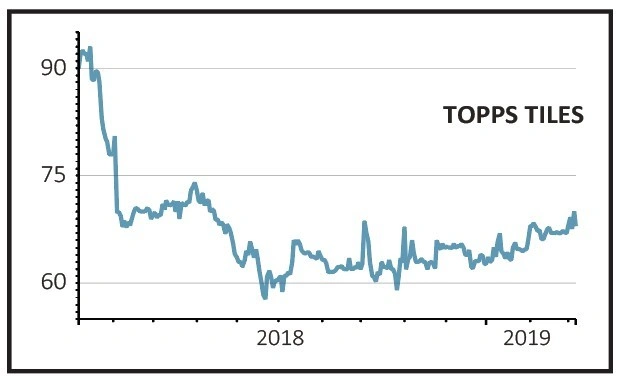

Topps Tiles (TPT) 68p

WHY ARE THE SHARES DOWN?

The UK’s largest specialist tile retailer languishes on a price-to-earnings ratio of 11-times with a 4.7% dividend yield, based on Liberum Capital’s forecast earnings per share and dividend per share estimates of 6.2p and 3.2p respectively.

Poor sentiment towards Topps Tiles (TPT) reflects heavy exposure to the UK’s challenged residential and renovation construction markets.

Investors are concerned about Topps’ near-term growth prospects amid diminishing consumer confidence, coupled with little to no growth in housing transactions resulting from Brexit-driven anxieties, which have caused weakness in the UK RMI (repair, maintenance and improvement) market. Topps’ like-for-like growth is subdued and rising costs present a margin headwind.

HOW CAN IT WIN BACK THE MARKET’S FAVOUR?

Topps Tiles posted a 1.4% like-for-like sales decline for the first quarter to 29 December 2018, although this reflected a demanding comparative and the base for comparison softens for the second and third quarters of its current financial year.

As the bulk of operating costs are fixed, Topps Tiles is operationally geared which means profit should grow by a greater amount than revenue. When sales growth is muted, that is a negative, but an eventual return to positive same-store sales growth would provide a material earnings boost.

Management needs to continue executing on its proven retail strategy of ‘out specialising the specialists’, aided by a winning digital offer. They believe there’s scope to add 10 to 15 sites a year, increasing Topps’ total estate from 367 stores to 450 locations.

Contrarians should also remember Topps has a competitive advantage in being the clear market leader, three times the size of its next biggest competitor.

Share price catalysts could include a Brexit resolution and confirmation Topps is growing profitably in the UK commercial market. Entry into commercial (via the 2017 acquisition of Parkside Ceramics) has nearly doubled Topps’ addressable market.

WHAT DO ANALYSTS SAY?

Liberum Capital has a ‘buy’ rating and 95p price target, arguing ‘the strategy continues to deliver outperformance versus the competition, underpinning Topps’ leading market position, and progress in the commercial division remains encouraging’.

It adds: ‘We do not see any change in the positive longer-term fundamentals and, with the group trading close to its five-year historic low price-to-earnings ratio, we see good value for those willing to look past the shorter-term.’

Berenberg has a ‘hold’ rating and 65p price target. ‘With no clear signs that the RMI market is going to return to strength over the next 12 to 18 months, and with operating cost inflation continuing to provide a material headwind, we remain cautious with regards to Topps Tiles’ outlook,’ it says, also acknowledging the retailer’s solid cash generation and healthy dividend.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Could Unilever turn the tables on Kraft Heinz?

- Doubts raised on OneSavings Bank and Charter Court merger

- Superdry, Kier, Domino’s and other news

- What Norway’s oil investment U-turn means for UK investors

- Raft of negative economic data fuels global growth concerns

- Airline sector gets tough on shareholders to keep flying post-Brexit