Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWitan is ready to fight back after lagging the market

Growing awareness among the general public of low-cost exchange-traded funds (ETF) means actively-managed funds have to try even harder to stand out from the crowd and justify their typically higher fees.

With ETF products such as Lyxor Core MSCI World (LCWL) offering exposure to companies around the world for a mere 0.12% annual charge, an actively-managed fund will need to be a compelling alternative in order to attract investors’ money.

Among the active funds in this situation is Witan (WTAN). Focused on global equities, its 0.75% ongoing charge (excluding performance fees) is very competitive versus the peer group yet still materially higher than the aforementioned Lyxor ETF.

Investment director James Hart acknowledges the competition from passive investment products such as ETFs and says Witan isn’t complacent about its position in the market, despite having £2.1bn of gross assets and being one of the most popular investment trusts among retail investors.

‘Anyone can buy a cheap index fund. We need to offer something superior because we charge more,’ admits Hart.

PERFORMANCE HAS LAGGED

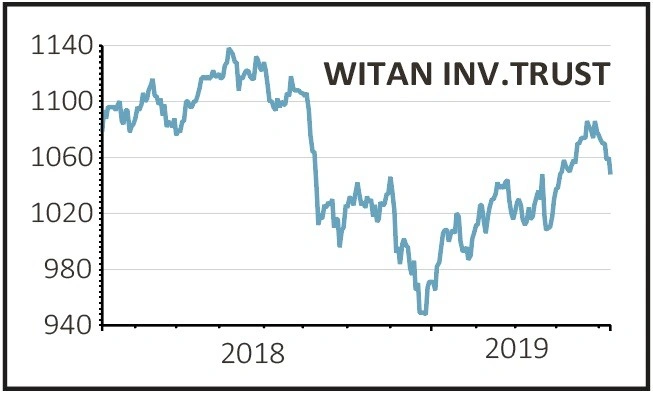

While Witan generally has a good performance track record, last year wasn’t a trophy period for the investment trust. Not only did its net asset value fall by 8.4% on a total return basis, but it performed worse than the 6.5% decline from its benchmark – which is a mixture of indices tracking different geographic territories.

When assessing funds it is important to consider their style(s) and how that fits into current market conditions. In Witan’s case, the value side of its portfolio suffered in 2018 as value remained out of favour as an investment style.

Performance is still lagging with the trust’s net asset value up 8.5% in the first quarter of 2019 versus a 9% gain from its benchmark.

MUCH BETTER LONGER-TERM RECORD

While frustrating for the Witan team and shareholders, this is hardly disaster territory. Last year was a difficult market for most investors and the scale of the underperformance this year isn’t that bad.

Ultimately a product like Witan should be judged on a much longer term and it is here that the investment trust has excelled.

Net asset value growth over the past five years was 64.9% versus 57.7% from the benchmark, and 268.2% versus 220% respectively over a 10-year period.

HOW DOES IT ATTEMPT TO BEAT THE MARKET?

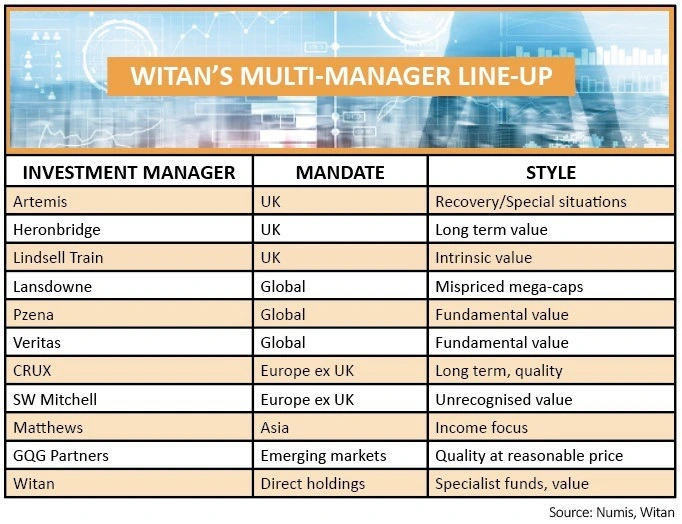

Witan’s strategy to deliver better returns than the market is to use a panel of third party managers, as well as running a small component itself, who are deemed to be experts in certain areas.

‘We choose people to back for multiple economic cycles,’ says chief executive Andrew Bell. ‘We provide access to fund managers you might not be able to access normally as a retail investor, plus a better deal with fees.’

All of the third party managers, bar one, are on one month’s notice which gives Witan some flexibility. ‘Some new funds, particularly those in the alternative energy space, are signing up managers for five years which can be a poison pill, in our view,’ says Bell.

He explains that Witan has made changes to managers over the years for such reasons as streamlining the number of experts in certain areas but he aims to retain appointed managers for the longer term, rather than switch managers to suit which investment style is in fashion.

Some of Witan’s managers should be well known to retail investors including Nick Train from Lindsell Train and Derek Stuart from Artemis. Others are under the radar such as Bevis Comer from Heronbridge Investment Management.

WILLING TO TRY NEW NAMES

Potential additions or replacements to the panel are constantly considered with up to 2.5% of the trust’s assets acting as a nursery for new managers to prove their worth.

In April 2018, £14m (0.7% of net assets) was allocated to Latitude Investment Management to invest in global equities. This proved to be a good decision as its component of the Witan portfolio outperformed significantly, with a total return of 6.3% compared with the 1.0% return from its global index benchmark during the latter nine months of the year.

‘The managers meet the board once a year and James (Hart) and I might meet them three or four times a year. However, we are quite hands-off. After all, these people are meant to be managing a portfolio, not talking about it all the time,’ says Bell.

WHO WOULD WITAN SUIT?

While the yield may be fairly low at circa 2.3%, dividend growth has been an important factor with the investment trust. Dividends per share have more than doubled since 2008, rising 130% compared with 25% for the UK CPI rate of inflation and 65% dividend growth for the UK market.

A share split is planned for 28 May where shareholders will get five new shares for every one they already hold. It wants to make Witan’s shares more appealing to individuals who like to make regular savings or reinvest their dividends. The current £10.60 price is deemed too high for many people to do this.

We highlighted Witan last month as one of the investment trusts to put in your ISA for the new tax year and we still rate it highly. We also believe it is suitable for anyone looking to add a solid global fund to their pension or even for a child in a Junior ISA.

It is a particularly good investment for someone who wants to ‘buy and forget’, namely put regular money into the fund and simply get on with their lives while Witan and its manager panel do all the hard work.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.