Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy new float Loungers can buck the high street gloom

In our view there are two key things which stand-out about newly-listed casual dining outfit Loungers (LGRS:AIM) which make it an interesting investment proposition.

First, because each Lounge is a hybrid format, it doesn’t compete directly with restaurants, coffee shops and bars in a local area, so it has no direct competitor.

This means that Loungers is uniquely positioned to benefit from ever changing consumer trends. For example, if breakfast venues suddenly become fashionable at the expense of late-night bars, the company is positioned to capture the upside, unlike single-concept operators.

Second, once established, Loungers aims to become part of the local fabric of a town where people can meet, support local charities or organise events. This could potentially create an economic ‘moat’ or protection around the business which helps fight off competitors.

Loungers has only closed four sites in the last 17 years, which is testament to the ‘stickiness’ and longevity of the hybrid format.

WHAT IS A LOUNGE?

Founded in 2002 by industry veterans Alex Reilley, David Reid and Jake Bishop and floated at 200p in April 2019 (and raising a little over £80m), Loungers operates from 125 Lounge sites and 25 Cosy Clubs.

A Lounge is equal part restaurant, pub and coffee shop and can be found across the UK in small towns and communities. Each has its own individual name which connects to the history of the town.

For example, Shares visited the Pato Lounge in Orpington, which is named after a breed of domestic duck, originally created by William Cook of Orpington. Pato is Spanish for Duck.

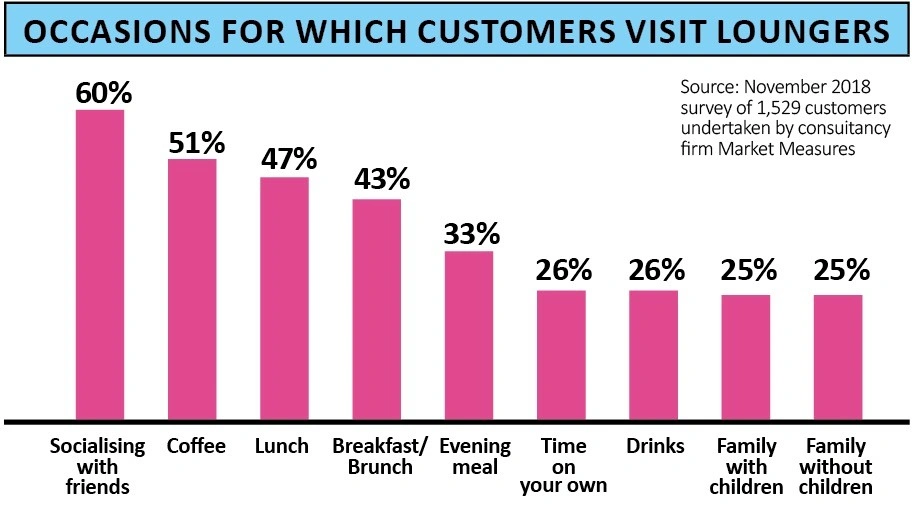

A Lounge site is open all day, serving coffee and breakfast in the morning, through to lunch, then meals and drinks in the evening.

Just over half of revenue is generated from sales of food, with just over a third from drinks (excluding coffee) and roughly 10% from hot drinks. It is clear from data collected by the company that its customers use the venue across the whole day and make repeat visits, with 27% visiting weekly and 67% visiting monthly.

Lounge is positioned at the value-for-money end of the price spectrum, with 90% of menu items costing less than £10.

WHAT IS A COSY CLUB?

Targeting more urban areas, underserved by an all-day-offer, Cosy Club is more formal than Lounge, and is an occasion-led venue. It therefore caters to more planned experiences, with customers making reservations and receiving a table service. They are more in keeping with a traditional restaurant or wine bar.

The spaces are larger and whereas for Lounge, customer visits are spread throughout the week, for the Cosy Club, Friday to Sunday is the busiest part of the week, representing almost two-thirds of visits. More men visit a Cosy Club in contrast to Lounge, where women represent 61% of all visits.

HOW LOUNGERS MAKES MONEY

The company makes healthy gross margins on the drinks and meals that it sells, getting 76%, and 72%, respectively, which averages out at an overall gross margin of 74%.

It receives cash from its customers before it has to pay its own suppliers, which means that it runs a negative working capital position of £3m to £4m a year.

As might be expected given the people intensive nature of the business, labour costs are the largest expense, coming in at close to 40% of revenue. Including energy maintenance, total site costs represent 48% of revenue.

Loungers leases all of its properties, typically on 15-year terms, and pays lower than sector average rents. This creates a sustainable economic advantage compared with its competitors. Rental costs are around 6% of revenue while the industry average is around 11%. Investors need to consider whether this will be sustainable in the longer term.

The company generates earnings before interest, depreciation and amortisation (EBITDA) of circa 20% per site. Joint brokers Liberum and Peel Hunt think there is scope to improve margins as the business builds more scale and central costs shrink as a proportion of revenues.

HIGH RETURNS ON CAPITAL

According to Liberum, the business produces far more revenue relative to capital expenditures than the industry average, roughly 1.6 times for Lounge and 1.5 times for Cosy Club, compared with an industry average of 1.1 times. This results in an attractive return on investment of 36% for a Lounge and 30% for a Cosy Club.

Management believes that the market will support over 500 sites nationwide based upon the work of independent property consultants CACI.

Loungers employs its own in-house property and build teams to select properties and fit them out. They, in turn are supported by nine directors, four managers and five logistics staff.

Loungers has a visible pipeline of new sites and plans to open 20 Lounge sites and five Cosy Clubs each year over the next few years.

HOW WILL THE GROWTH BE FINANCED?

Upon admission the company had a net debt position of £25.5m, a five-year bank loan of £32.5m and a £10m revolving credit facility. Opening 20 Lounge sites and five Cosy’s per year will cost around £19m per year, which means that the company might need to ‘dip into’ some of its credit facilities to facilitate growth and increase debts over the next year or two.

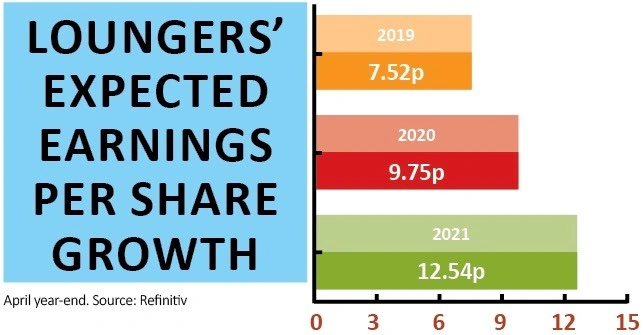

However, analysts expect the business to become self-financing from internally generated cash flow from 2022.

SHARES SAYS: At 218p Loungers is an interesting growth story with a truly differentiated format which caters to consumers evolving spending habits although is not cheap at 22.5 times earnings.

As a newly-listed company some investors may want to wait for signs it can deliver on its ambitions before taking the plunge. Full year results are out on 28 August 2019.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.