Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazine3i Infrastructure is a great long-term investment

The second and third quarters of this year have seen some chunky fundraisings by infrastructure and renewable energy funds.

In June, Greencoat UK Wind (UKW) raised €375m, Sequoia Economic Infrastructure Income (SEQI) raised £216m and Aquila European Renewables Income (AERI) raised £154m.

In September, Sequoia raised a further £139m, IPP (INPP) raised £234m in two separate funding rounds and Renewables Infrastructure Group (TRIG) raised £227m.

All of which goes to show that while investor appetite for stocks continues to wane, exposure to infrastructure via quoted vehicles remains very much in vogue.

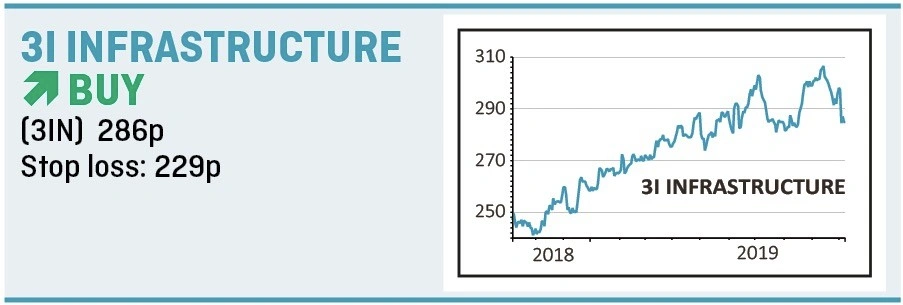

With a market capitalisation of £2.3bn, FTSE 250-listed 3i Infrastructure (3IN) has delivered consistent growth in net asset value (NAV) of 13% per year including dividends since listing in 2007, which is more than twice the total return of the FTSE 250 index over the same period.

The investment trust owns a portfolio of economic infrastructure businesses, which in turn own their physical assets in perpetuity. It has a portfolio of greenfield projects in the construction phase where it owns all or part of the ensuing concession.

The infrastructure portfolio makes up 88% of the group’s assets and includes among other things telecom towers, power lines and metering, energy storage, and emergency rescue and response services.

These assets typically employ between £50m and £250m in capital and generate annual returns of between 9% and 14%, and the company has a good track record of realising full value for its assets when the time comes to sell.

The main attractions of infrastructure as an asset class are that it offers diversification from equities as well as ‘locked-in’ long-term yields.

Infrastructure funds typically aren't cheap though, and like the rest of the sector 3i trades above net asset value which analysts at Stifel estimate was between 245p and 250p at the end of September. On that basis the trust is at a premium of 14% to 16%, well below its recent high but not cheap on an absolute basis.

There is conceivably a risk that the Labour Party might win the next general election and set about nationalising infrastructure assets but that seems unlikely in the short term.

Also the company is currently raising more money to pay down debt following a recent acquisition. While the deal is accretive to earnings, the issue of new shares is dilutive for existing shareholders.

As the company identifies more targets, so it will need to raise more finance or sell existing assets so there is a risk of further dilution.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.