Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat to expect from investing in different assets over the long-term

Before embarking on a journey it is important to have a realistic expectation of how long it will take, how bumpy or smooth it will be and the likelihood of reaching the final destination.

Likewise there are many types of asset to choose from in the capital markets which will be appropriate for different levels of risk appetite and time frames.

There’s no point for example putting your hard earned money into an instant access cash account and expecting to earn high rates of return, especially over longer periods.

RISK AND RETURN

Assets which produce higher rates of return are normally associated with higher levels of risk, but the savvy investor will always be looking for situations which maximise returns for a given amount of risk.

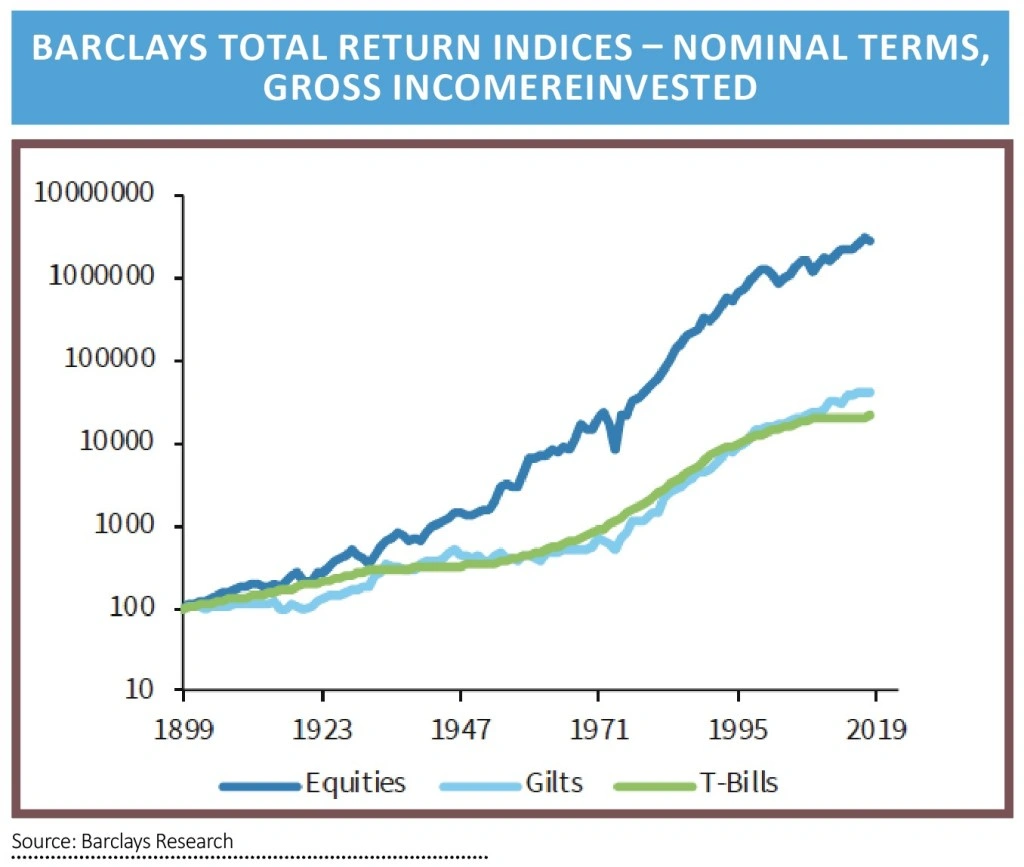

Barclays has been publishing an annual study since 1956, providing data and analysis on long-term asset returns in the UK. Shares has used that data to shed some light on investing in relation to cash, bonds, equities and inflation.

CASH

Cash held in an instant access account is very safe as amounts up to £85,000 are insured by the UK government even if the bank goes under. As one might expect, idle cash shouldn’t provide much of a return, but today’s low rates haven’t always been this measly.

For example since 1945 the value of £100 invested in cash and assuming that interest was re-invested (an important point) would be worth £6,349 today. That works out at a compound annual growth rate (CAGR) of 5.75% a year.

Another important point to mention here is the effect that inflation has on purchasing power, because the aforementioned 5.75% per year is reduced to 0.66% per year if measured in today’s money, quite a stark difference.

That said, cash is a very important element of any long-term plan, both as an emergency fund for unseen problems as well as ‘dry powder’ to take advantage of unseen investment opportunities.

BONDS

A bond is like an ‘IOU’- a company or a government borrows money from an investor by issuing bonds in exchange for cash. They pay a fixed or variable rate of interest over a specific time period, and at maturity the investor would expect to get their money back.

Government bonds are less risky than corporate bonds because the bank of England is able to print money if necessary in order to pay back its loans, while a company has to make cash profits in order to pay back its loans. This introduces a credit risk.

That’s why corporate bonds pay higher rates of interest than government bonds, to compensate for the possibility that the loan isn’t fully repaid at maturity.

As you might expect, the less financially secure a company is perceived to be, the more interest it has to pay to investors to compensate them for the higher risk.

However some bonds are of a higher quality, such as senior bonds which are secured on real assets that a company owns.

If a company struggled to pay interest, it would ‘default’ on the loan and the owners of the bond would be legally entitled to seize the company’s assets.

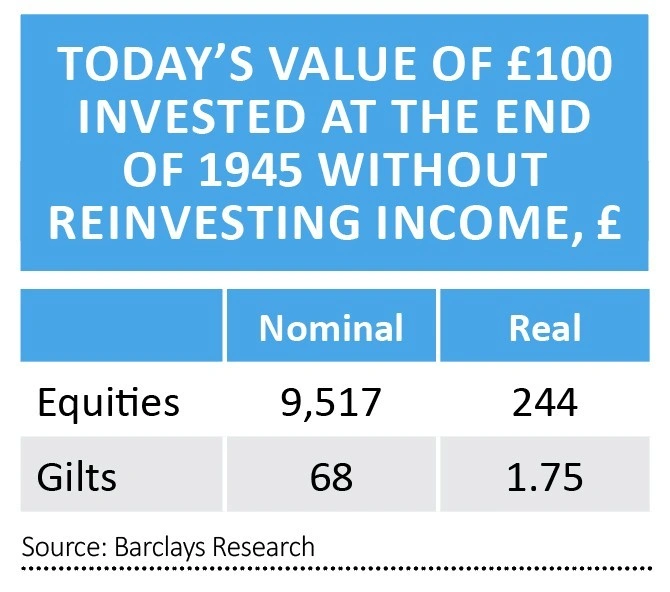

A £100 investment in government bonds in 1945 with interest re-invested would have turned into £8,991 today, a CAGR of 6.25%. That is 42% more than cash returns. If we adjust the return for inflation the CAGR falls to 1.1%, still about 1.6 times better than the return from cash.

As you can see, over longer periods inflation can have a brutal impact on cash and bond real returns. This is because the rates of interest paid are fixed through the life of the bond, while future inflation can rise unexpectedly.

EQUITIES

Historically stocks have provided the best long-term returns. £100 invested in 1946 would have turned into £217,045 today, equivalent to a CAGR of 10.94%. That is £208,054 more than government bonds and £210,696 more than cash. Adjusted for inflation the CAGR has been 5.6%, 5.5 times more than bond returns and 8.4 more than cash.

RISK

The 10.94% achieved since 1945 has not been a straight line for stocks, sometimes they have delivered negative returns, even over 10-year periods. That makes them an unsuitable investment for shorter holding periods.

It’s important to build a diversified portfolio of stocks, as single companies can and do go out of business from time to time. Loss of capital is more of a risk with stocks and corporate bonds than with cash and government bonds.

Although today’s investment environment is different to those in the past, dominated as it is by ultra-low interest rates, the ranking of expected returns and the risks attached to those returns remain a good guide for the future.

It is very important to remember that around 96% of the total return comes from re-investing the income received, whether from cash, bonds or stocks.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.