Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat would a consumer slowdown in the US mean for markets?

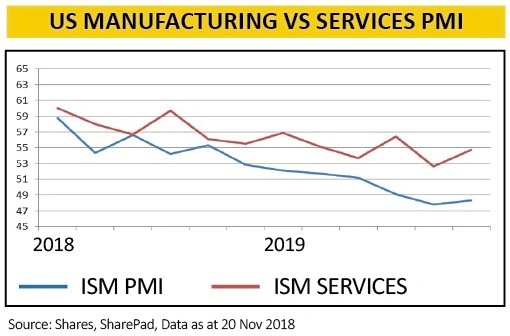

For the last year the mantra among market observers has been that although the US economic expansion is long in the tooth, there’s no need to worry about poor manufacturing confidence surveys. As long as the services sector is still showing growth, goes the thinking, markets can keep rising.

Recent corporate results and data releases suggest this argument may be losing some credibility.

The US Institute of Supply Management’s monthly survey of industrialists, the purchasing managers index (PMI), has been falling inexorably towards the expansion/contraction threshold of 50 – and has been solidly below it for the last three months. The same institute’s services sector PMI has been more robust although it too has been falling.

Meanwhile the US S&P 500 benchmark has continued to chalk up new highs, gaining 24% year to date excluding dividends, while the Nasdaq index which is more technology-focused has added 28%.

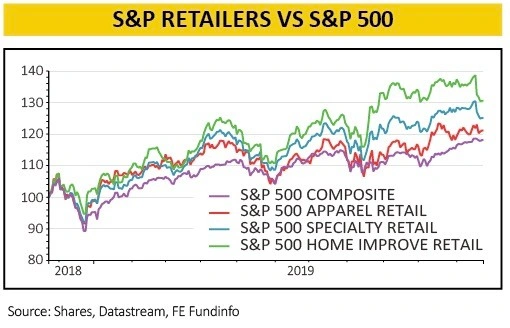

As we explained a few weeks ago, domestic consumer-facing stocks have been central to the performance of the US market this year. Retail stocks in particular have been strong performers, as the chart shows.

At its peak earlier this month, the S&P 500 Apparel Retail index was up 24.4%, in line with the benchmark, while the Specialty Retail index was up 31.4% and the Home Improvement Retail index was up 34.5%, a full 10 percentage points more than the index.

THE ECONOMY RELIES ON CONSUMERS

Consumer spending is estimated to account for 70% of US economic activity, and the retail sector is seen as a useful gauge of the health of two key drivers of confidence, housing and jobs.

Just this week, Jerome Powell, head of the US Federal Reserve, said that central bank officials ‘have a favourable outlook for the US economy founded on strong consumer spending, which is bolstered by a robust jobs market, increasing incomes and solid consumer confidence’.

Although spending slowed in the third quarter, with growth very slightly negative in September according to the Commerce Department, consumers are still buying enough goods and services to keep the economy from stalling.

Hence the market’s surprise when earlier this month Home Depot, which had been one of the biggest contributors to the year-long rally and seemed to have shed its cyclical image in favour of ‘defensive growth’, reported lower-than-expected third quarter sales and reduced its guidance for full-year sales growth.

Home Depot shares fell sharply on the downgrade, and while rival Lowe’s reported earnings marginally above estimates, sending the shares briefly to new highs, they have since drifted suggesting investors are hesitating to buy rather than piling in as they might have done before the Home Depot warning.

A TALE OF TWO MARKETS

Large-format discount retailers like Best Buy, Costco, Target and Walmart may have delivered strong sales in their most recent quarter, particularly in their online businesses, and ‘off-price’ retailer TJX – owner of the TX Maxx chain – also reported an uplift in sales and raised its full-year guidance.

However department stores such as Macy’s, Nordstrom and JC Penney have struggled all year to attract consumers and have followed Home Depot in cutting their forecasts, despite Thanksgiving, Black Friday and the Christmas period typically boosting sales. Shares in Macy’s have lost half of their value this year.

Most intriguing of all has been the poor performance of Amazon.com, the biggest ‘disrupter’ of the retail sector. Amazon shares have lagged the market all year as analysts have downgraded their earnings forecasts. The company’s fourth-quarter sales guidance of $80bn to $86.5bn was some way shy of estimates, while the cost of upgrading its Prime delivery service is eating into margins.

WATCH THE 'SOFT' DATA FROM NOW ON

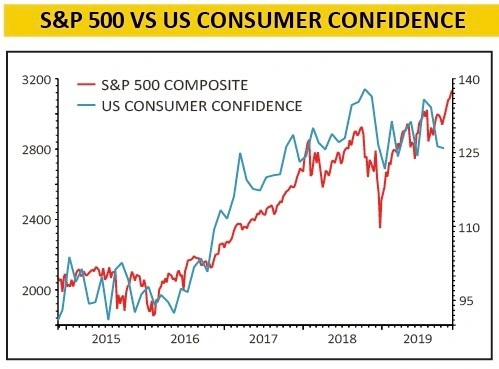

Consumer confidence is key for the retail sector and the wider economy, and the various US measures of confidence seem to be pointing to a more cloudy outlook for spending.

The Conference Board’s consumer confidence index has dropped for the last four months running, missing market forecasts in both October and November, as has the expectations index which is based on consumers’ short-term outlook for income, business and labour market conditions.

Consumers were less optimistic about the job market and business conditions in six months’ time with a lower proportion of positive responses and a higher proportion of negative responses.

The University of Michigan consumer sentiment index and expectations index have also been falling for several months in spite of rate cuts from the Federal Reserve.

It’s important to be aware that the performance of the stock market can also have a big impact on consumer sentiment. The consumer confidence index peaked at 137.9 in October last year, but as the stock market sold off sharply confidence also tumbled, hitting a low of 121.7 in January.

Although it recovered over the spring, the latest reading is still some way below the high. There is a danger here that if consumer confidence starts to crack, the stock market could start to falter creating a negative feedback loop with confidence affecting the market and vice versa.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.