Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineInc vs acc: choosing the right fund type to collect or reinvest dividends

Share classes on funds can be confusing, but picking the right and wrong one can make a significant difference to your portfolio.

Often investors will be faced with a confusing array of letters or acronyms after a fund name, which can look like alphabet soup but actually make a big difference to how much you’re charged, whether income is paid out or reinvested, and what currency the fund is in.

Some of the differences are explained in this article.

WHAT IS INC AND ACC?

Fund investors, particularly in income funds, can be faced with the choice between an ‘Inc’ or ‘Acc’ share class – standing for ‘Income’ or ‘Accumulation’.

Put simply, if you invest in the accumulation version of the fund then any income generated from the underlying investments will be automatically reinvested back into the fund, while the income version will see all of that money paid out to you.

Which one you pick depends on whether or not you’re relying on the fund to pay you out an income that you need to use now. For example, someone who is drawing their pension may want the fund’s income to help pay for their lifestyle.

However, someone who is still building up their pension pot and doesn’t need any additional income could buy the accumulation share class and see their income reinvested.

If you buy the income unit the income will be paid out across the 12-month reporting period of the fund, but how often it pays out depends on each fund – sometimes it’s monthly, quarterly or twice a year. You’ll need to check the fund documents to see the payment frequency.

The fund may also choose to attempt to smooth the income payments across the year – rather than just paying out the income as it comes in. This means you’d get roughly equal amounts through the year and then any remainder included in the final payment of the year.

SPOTTING THE DIFFERENCE BETWEEN AN 'INC' AND 'ACC' FUND UNIT

The clue is in the product name. If you want to collect income as cash look for the letters ‘Inc’ in the fund title. If you want to automatically reinvest dividends, look for the version of the fund with ‘Acc’ in the fund title.

TB Evenlode Income B Inc – this is the cash-paying income version

TB Evenlode Income B Acc – this version rolls up the income so dividends are automatically reinvested

HOW DOES IT AFFECT MY RETURNS?

With the accumulation unit you benefit from compounding of returns, assuming the fund increases in value. This means that the income generated by the fund is used to buy additional units of the fund, which then (hopefully) grow and generate more income. The impact over the long time period you’re holding the fund can be quite dramatic.

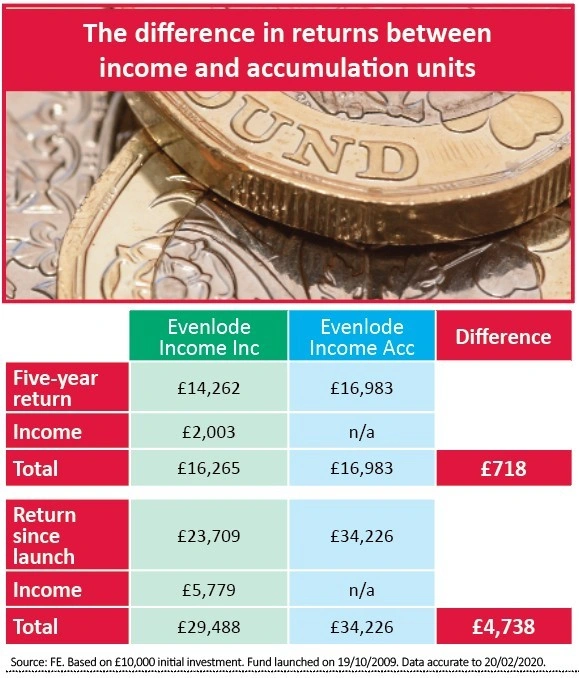

Let’s take Evenlode Income (BD0B7D5) as an example of an income-focused fund. Over the past five years the ‘Inc’ version of the fund has turned a £10,000 investment into £14,262.

During this time it has also paid out £2,003 in income. However, if you’d bought the ‘Acc’ version of the fund it would have turned that same £10,000 initial investment into £16,983 – meaning you’ve generated more than £700 in extra returns by reinvesting the income payouts.

The difference is starker over longer periods, as there is more time to benefit from compounding. Since the fund launched in October 2009 the Inc version has turned £10,000 into £23,709, while also paying out £5,779 in income while the same £10,000 in accumulation units is now worth £34,226 – nearly £5,000 more than if you’d gone with the Inc version.

BUT HOW DOES THIS ACCUMULATION WORK IN PRACTICE?

As income is received from the underlying investments it will be added to the capital value of the fund, which will be reflected in the unit price of the fund. So if accumulation version of the fund received 10p of income per unit, the unit price would rise by that amount to reflect this payment.

For accumulation units this money continues to be rolled up in the fund, as and when the income is received. For income units this money is also rolled up, but on the next date that income is due to be distributed by the fund, the unit price will drop as the income money is stripped out of the fund.

You’ll still be left with the capital value, but all things being equal your unit price will drop by the amount of income that’s been paid out (and you’ve received). For example, if the unit price is 110p and 10p of income per unit is paid out, then the unit price would drop to 100p.

WHAT ABOUT THE TAX DIFFERENCE BETWEEN INC AND ACC FUNDS?

You also need to think about the tax on any income you are paid out. If you invest your money in an ISA you won’t need to pay any tax on income generated by investments in the account. But if you own the income-generating fund in a dealing account, where there are no tax advantages, there will be tax implications for either unit.

For the income unit it’s simpler. You’ll have to pay tax on income that’s paid out to you, and this will be categorised as either interest or dividend income, depending on the fund you’re investing in and what it invests in. If it’s categorised as dividend income it will be counted against your annual dividend allowance, which is currently £2,000.

If your dividend income exceeds this, when combined with other dividends you’ve received in the year, you will have to pay dividend tax at your marginal rate. However, if the fund categorises these payouts as interest it will be taxed as income rather than dividends.

This means that rather than being counted against the dividend allowance, it will count as part of your personal savings allowance. The annual limit is £1,000 for basic-rate taxpayers, or £500 for higher-rate taxpayers. Additional-rate taxpayers get no allowance.

INCOME TAX ON ACCUMULATION FUNDS

If you own the accumulation unit then income that’s rolled up into this unit is called ‘notional distribution’ and is taxable in the same way as the income that’s paid out to holder of the income unit of the fund.

Your platform will usually keep track of these notional distributions and provide you with a summary of them at the end of the tax year. This can be used when filing a tax return. You then need to go through the same process as above, setting it against the relevant tax allowance.

If you own the funds within an ISA and decide to sell them you won’t have to pay capital gains tax on any growth in the fund, but if you own it outside a tax-efficient wrapper such as a dealing account you’ll need to consider the capital gains tax (CGT) implications. The current allowance for CGT is £12,000 per person a year, meaning you can make gains up to this level before you pay tax.

With the income units of a fund this is a simple calculation, as the income has been paid out already so you just need to deduct your initial investment from the amount you receive when you sell the investment, and work out if you owe tax on any gains.

CAPITAL GAINS TAX ON ACCUMULATION FUNDS

With an accumulation unit it’s a bit trickier. You need to deduct the sum of the initial investment and any notional income that’s been accumulated from your sale value, to work out the capital gain.

For example, if you buy a fund for £100 and received £20 of notional income in the accumulation unit, and then sell it for £200 you’ll only have a capital gain of £80 (the £200 minus the £100 initial investment and the £20 income).

This is important because you could have already paid tax on the notional income you received, so if you don’t include it in the final calculation you could end up paying tax twice on the same money. Most platforms will keep track of the notional income for you and provide this information.

What if I want to switch?

If your circumstances change you may want to shift from the accumulation unit of a fund to the income unit – for example, when you come to retirement age and want to use your pension for income.

You can switch from one unit of the fund to another, and with AJ Bell Youinvest you would incur no cost for doing so. You would see the same value of your investment, regardless of the unit you own, but you might see the number of units change.

For example if you have £100 worth of the accumulation unit of a fund, which is priced at 100p, you would own 100 units of the fund. However, if you switched to the income unit, which was valued at 80p per unit, you would still own £100 worth of the fund but would see the number of units you own increase to 125.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.