Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat is a reasonable return to expect from investing?

One of the main reasons why new investors tend to become despondent with the process is because they set unrealistic expectations for themselves.

The inexperienced tend to believe that they can achieve returns far and above what is reasonable, or likely. Search around the internet and you’ll find countless investing strategies and systems that promise to double or triple your money in weeks or months. Do not fall for these hollow claims, they are for the foolish and extremely gullible.

The reality is not about knock-out performance for a handful of rocket stocks or star fund managers, but steady, incremental gains across a range of different investments over the long-run. New investors often fail to appreciate just how long it takes to build investment wealth, but investing is a process that should be measured in years, even decades (depending on when you start), not in months.

– Have realistic expectations

– Play a long game

– Time and compounding are your friends

This is because there is always the risk of external or company factors wreaking havoc with stock markets, funds and individual company shares over a short period. Losses are as much a part of investing as anything else, and you must be prepared to accept that.

Take the current coronavirus. This emerged out of the blue and simply could not have been foreseen, yet it has hammered financial markets and share prices everywhere. The world is now in ‘corona’ chaos yet the FTSE 100 index, the UK’s benchmark, is still more than 1,000 points above its lows during the depths of the financial crisis.

A REASONABLE RETURN

So what is a reasonable rate of return from investing? The simple answer is, it depends on your appetite for risk. If you hate the idea of risk, you can leave your savings in the bank or put them into government bonds. Neither will generate the kind of long-term returns you can get from the stock market but then you aren’t taking any risk.

These assets are often used to calculate the so-called ‘risk-free rate of return’. Riskier investments are benchmarked against this, with an expectation of higher potential returns as you move up the risk curve.

For example, you can get 1.31% a year (Virgin Money) from an easy-access cash ISA, according to MoneySavingExpert, or 1.55% if you’re willing to tie you cash up for three years (Aldermore).

That’s much better than the 0.24% annual income (yield) on a two-year UK government bold, or the 10-year’s 0.37%, which could be considered as the risk-free rate.

So what does history tell us about what a reasonable rate of return is from different assets?

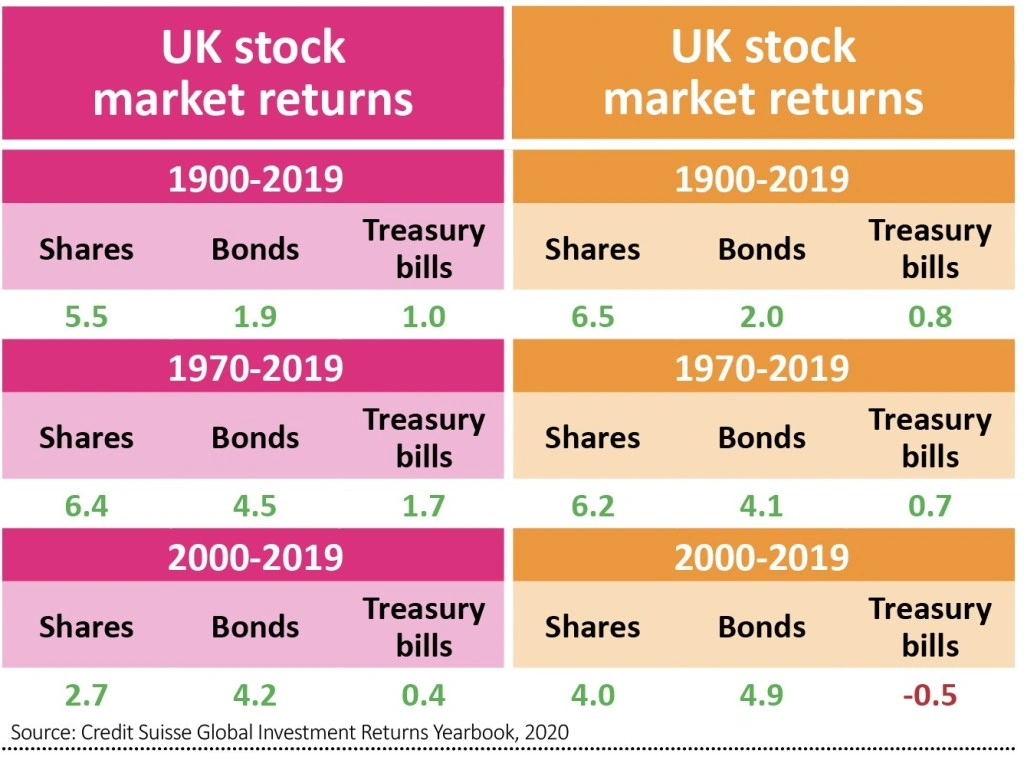

According to the Credit Suisse Global Investment Returns Yearbook 2020, global stock markets have delivered a real return of 7.6%, versus 3.6% for bonds over the past decade. The annual study is conducted by academics Professor Elroy Dimson, from Cambridge University, and Professor Paul Marsh and Dr Mike Staunton of the London Business School.

Real returns means after stripping out the effect of normal inflation. While we have had several years of low, sub-3% inflation (CPI averaged 1.74% in the UK during 2019) that is not always the case. In 2011 CPI averaged 3.85% and it was more than 7% in 1990/1991, figures that can significantly skew how much better-off investors really are over time.

Long-run returns have been more moderate than 7.6%, especially in local markets. For example, as the data shows, UK returns averaged 6.4% in the years between 1970 and 2019, but just 2.7% since the beginning of this century. That compares to 4.5% and 4.2% for gilts.

It’s a similar pattern in the US, where longer-range average return trump short-term gains for stock markets, illustrating how time is an investor’s friend.

BENCHMARKING PERFORMANCE

The final piece of the returns puzzle is benchmark performance, or in other words, what investors should expect for investing in individual shares and stock-selecting ‘active’ funds versus buying passive trackers of indexes, like the FTSE 100.

Consider Layla. The 41-year old mother of two has earned an 11% total return (capital gains and dividend income) in both 2018 and 2019 from her portfolio of actively-managed funds. She is pretty chuffed with that since it is significantly better than she would have earned by leaving her cash in the bank, and it was also far better than the single-digit yield of gilts, or the risk- free rate.

Yet the FTSE 100 went up 13.5% during 2019, albeit not in a straight line. On reflection, Layla wonders why she would pay a 1% or so active fund management fee when they delivered a lower return than an unmanaged FTSE 100 tracker fund or ETF. However, in 2018 the FTSE 100 did less well, declining by about 12.4%, which nets off at a 9.94% return over the two years.

So her 11% is better, albeit not by a huge amount. Small margins over time add up because of the effects of compounding, where past profit can be reinvested to super-charge returns. Set against this you also need to consider the extra costs of actively managed funds compared with passive products.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.