Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat are stocks and shares?

For first-time investors, continued references in the media to ‘stocks’, ‘shares’ and ‘equities’ might lead you to think that they are all different things. However, they are all just different names for the same thing.

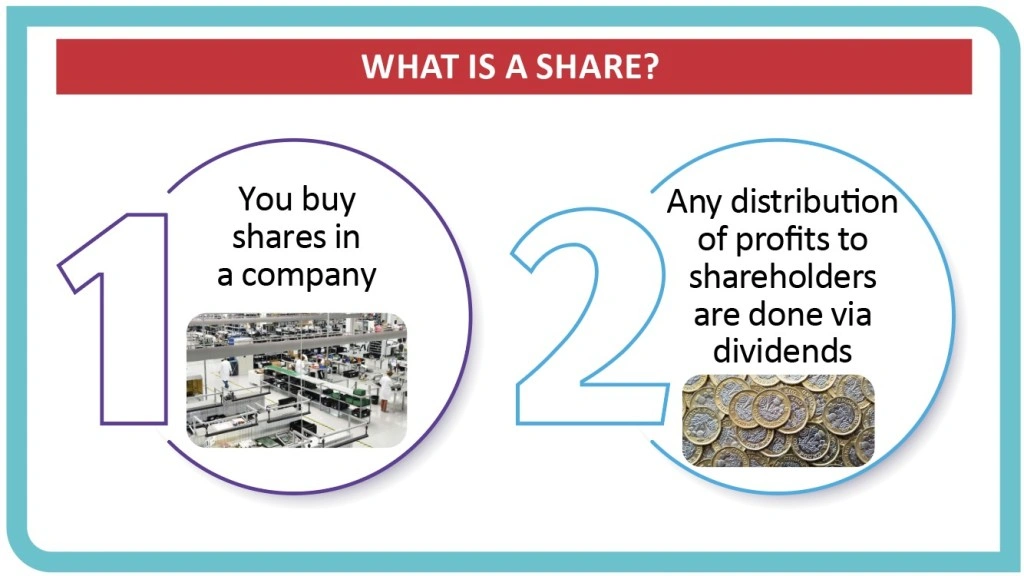

It’s easiest to think of a ‘share’ as just that. If you buy shares in a company – such as Lloyds (LLOY), for example – you are literally buying a share in the company’s business. For that investment, you are entitled to part of the company’s future income and profits in the form of dividends. You also hopefully benefit from your shares going up in value if the business is successful.

Ownership of the shares also gives you the right to take part in the company’s annual general meeting, to vote on certain decisions put forward by the board, as each share carries a vote, and to buy shares in any new issues the company might make to fund its growth.

Buying and selling

Shares are bought and sold on the stock exchange. Before the ‘Big Bang’ market overhaul in 1986, shares were traded face-to-face on the floor of the London Stock Exchange itself.

The stock ‘broker’, who was buying or selling shares on behalf of their clients, would negotiate in person with a stock ‘jobber’, whose job it was to make a continuous market price in a given list of shares.

Trading eventually moved to computer screens with the ‘jobbers’ making prices and the ‘brokers’ buying or selling electronically or by telephone. This is still the case today (for an explanation of the process of buying shares for the first time, see here).

Why buy shares?

Historically, the case for owning shares is strong. According to Richard Oldfield, fund manager and the author of Simple But Not Easy, since around 1850 shares have given a real return (after inflation) of around 6% per year plus or minus a percentage point in most countries.

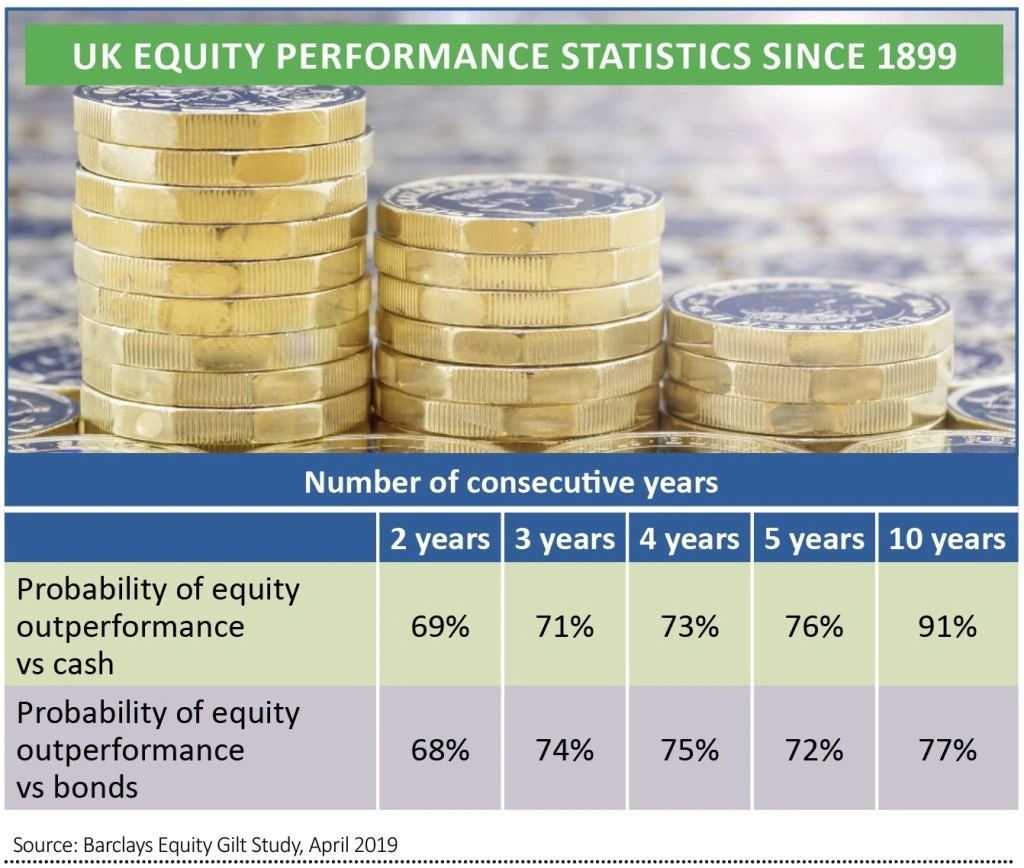

The 2019 iteration of Barclays’ Equity Gilt Study shows that £100 invested in cash since 1899 would be worth just over £20,000, while the same amount invested in UK government bonds would be worth £42,000.

However, if you had invested £100 in UK shares in 1899, they would have been worth around £2.7m by the end of 2018.

As these figures show, over the long run the returns on shares are much higher than the returns on cash and bonds, but those returns are also much more volatile.

While the returns on bonds and cash are reasonably predictable, the returns on shares can vary hugely over short periods, as the performance of the stock market this year has demonstrated.

Whereas bonds pay a fixed rate of interest, and at some point the company or the government pays back the loan and the investor gets back their capital, shares are an actual stake in a company’s assets and profits.

If a company fails to grow its profits much, its shares will perform poorly. If the company gets it completely wrong and goes bust, however, shareholders may not even get their money back.

Risk versus reward

If you might not even get your money back, you might wonder why you should buy shares at all. The answer is that, broadly speaking, higher risk leads to higher returns. For more on the different levels of risk involved in cash, shares and bonds, see here.

If you aren’t comfortable with the risk that, in order to generate higher returns by buying shares you might lose some or all of your investment, then you should probably stick to bonds or other ‘long duration’ assets such as property.

If you are comfortable with that risk, then you need to set yourself reasonable expectations. Success in investing isn’t instant, nor is it easy otherwise we would all be millionaires within a year.

Mistakes are par for the course

Building long-term wealth takes time and patience, and a willingness to accept losses as part of the process. No fund manager on the planet gets every investment decision correct, in fact many successful managers would admit to being only two thirds right at best.

One of the most common mistakes that investors and analysts make is to be too confident in their forecasts for companies’ profits. Quite often they focus too much on what a company is good at and not enough on what it is bad at or what could trip up their forecasts.

Usually, looking at the consensus range of forecasts is better than looking at one single forecast, and if a company’s shares look cheap on even the lowest profit forecast then it is probably worth further investigation.

Information provider Reuters provides, free of charge on its website, consensus estimates for sales and earnings per share (EPS). Also, many larger companies have an ‘Investors’ section on their website with a range of analysts’ forecasts.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

Investment Trusts

Money Matters

News

- Scottish Investment Trust denies ‘style drift’

- £1.6bn fundraising frenzy: companies tap markets to ensure their survival

- UK industrials ‘unlikely’ to breach debt covenants

- Trading platforms see surge in demand amid market volatility

- Market’s attention turns to exit strategy

- UK Treasury reported to be considering strategic companies bailout

- Times are hard for value fund managers

- Lindsell Train’s Japanese fund soars ahead