Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineUnderstanding bonds and how to invest in them

Bonds are an important asset class in the world of investing, providing diversification benefits as well as income. In times of market stress, bonds have historically provided defensive characteristics.

First-time investors should use investment funds as the easiest way of adding bonds to their portfolio.

WHAT ARE BONDS?

Governments and companies can raise cash by issuing bonds, which are like IOUs. They sell the bonds to investors in exchange for cash which they have to repay over an agreed timeframe – this can range from a few months to 30 years.

They also have to pay a regular interest payment to the investor which is called ‘the coupon’. In most cases the coupon remains fixed until the end of life of the bond.

The issue price of the bond is called ‘par value’ and once the bond term ends, referred to as ‘maturity’, the initial amount of money received for the bond is paid back at par value.

With bonds, the investor (the person buying the bond) has to weigh up the creditworthiness of the borrower (the entity issuing the bond), especially in higher risk corporate bonds, because there is always a chance that the original capital will not be paid back in full.

In other words, be careful about bonds that pay a seemingly high rate of interest as you may not get all your original cash back.

UK GOVERNMENT BONDS

Government bonds are referred to as Gilts in the UK and issued by the Treasury. They are considered very safe, partly because the government has the power to raise taxes to service and repay its debts.

One example of an exchange-traded fund that tracks the price of UK Gilts is Lyxor FTSE Actuaries UK Gilts 0-5yr UCITS ETF (GIL5).

Longer-dated bonds pay higher coupons than shorter-dated bonds, partly because investors demand a higher rate to cushion them against future inflation risk and partly because there is always a small risk that the bond might not be repaid.

For example the current 30-year Gilt has a fixed coupon of 1.75% a year, while the two-year bond pays 0.5%.

WHAT IS THE YIELD TO MATURITY?

Receiving only 1.75% a year for 30 years may sound miserly, but in fact it’s currently much worse than that.

At the time of writing, the buy price of the bond was 127.6 and at maturity the investor will be repaid at the original issue price (or par value) of 100. This means investing now would lock in a capital loss of 21.6% if held to maturity. However the investor would still get interest payments along the way.

So taking into consideration the capital loss and the annual interest payment of 1.75% a year for 30 years will result in the investor actually receiving only 0.68% a year. This is called the ‘yield-to-maturity’.

The yield to maturity of the two-year bond is slightly negative at the time of writing. Investors are guaranteed to lose money if they hold these bonds until maturity. However, fund managers will still buy these bonds if they believe interest rates will become negative in the future, providing capital gains.

Bond prices rise as yields fall, so in the above example fund managers would look to make a profit by selling the bond at a higher price than they paid and not holding the bond until it matured.

OVERSEAS GOVERNMENT BONDS

Investors may want to look at different countries and their government bonds in order to achieve higher rates of interest.

This effectively narrows the list down to emerging markets where economies are growing faster and interest rates are higher.

Two examples of funds that invest in this area are M&G Emerging Markets Bond Fund Sterling (B4TL2DS) and Vanguard USD Emerging Market Government Bond UCITS ETF (VEMT).

CORPORATE BONDS

Companies can raise money by issuing corporate bonds to investors in return for paying them an annual or semi-annual fixed rate of interest.

One crucial difference compared with government bonds is that most companies don’t have cash flows that are as reliable as the government’s tax receipts. This introduces more credit risk.

Investors in corporate bonds need a full understanding of the issuing company’s finances in order to access the likelihood of receiving their money back. This requires the ability to analyse cash flow statements and balance sheet strength, as well as grasping industry profitability dynamics.

Many investors – both first-timers and more experienced ones – can’t or don’t want to do this, which is why it is easier to buy a bond fund where a skilled fund manager is selecting the bonds, or an exchange-traded fund which just tracks a broad basket of bonds.

Corporate bonds are considered more risky and consequently pay higher coupons than government bonds.

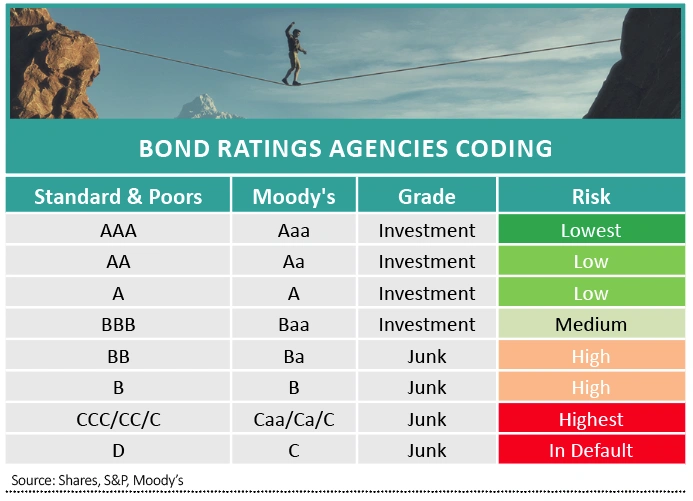

Ratings agencies specialise in assessing the riskiness of bonds and sell their research to fund managers, although it should be mentioned that companies themselves pay the ratings agencies, so there is an inherent conflict of interest.

Corporate bonds are classified into investment grade and non-investment grade. Some fund managers have mandates which restrict them to investing in investment-grade only, while some managers specialise in non-investment grade, also called junk bonds.

The riskier bonds are issued by companies with weak fundamentals and heavily indebted balance sheets, hampering their ability to repay debts. But, for specialists willing to put in the work, this part of the bond market can be a good hunting ground for mispriced securities.

An example of an exchange-traded fund tracking a basket of corporate bonds issued by large cap high quality companies is iShares GBP Corporate Bond UCITS ETF (SLXX).

For exposure to high yield bonds there are funds such as Baillie Gifford High Yield Bond Fund (3081671).

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.