Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow to maintain a portfolio

Last week we looked at effective ways to build a portfolio and why it’s so important to construct a well balanced portfolio. In this article we focus on maintaining good balance as the performance of different assets diverges.

If you have done a good job constructing your portfolio, you should expect to see performance vary between the different assets, and this divergence brings more stability to your returns.

If that divergence increases, over time some areas of your portfolio may become significantly larger or smaller than you first intended. What should you do?

DON’T REBALANCE TOO OFTEN

It might be tempting to use a blanket rule to rebalance your portfolio say every quarter or perhaps biannually. However you should think carefully before tinkering with something you spent so much time building.

Matt Brennan, head of passive portfolios at AJ Bell highlights the hidden costs of trading which are not only restricted to broking commissions, but include bid/offer spreads, which also need to be taken into account. That is, the difference between the cost of buying and selling units.

These costs can add up, especially if you choose to rebalance four times a year, but first you might be thinking, if it costs money why would I want to do anything in the first place, why not just let the asset proportions diverge?

The short answer is that as asset prices move around, the overall portfolio risk changes. And that matters because your initial asset allocation was based upon your individual risk tolerance, age and financial circumstances.

For example, if the shares part of your portfolio started out at 60% and a few months later they represented 70%, you are implicitly taking more risk overall, and your asset allocation may no longer match your needs.

That’s primarily because the portfolio’s government bonds proportion will now be lower and these assets provide not just stability but also some protection if shares suddenly went into reverse. Your portfolio would be less stable and more volatile.

THINK IN BANDS

The trick is to strike a balance between keeping a balanced portfolio which matches your needs and tweaking too often and incurring lots of charges. According to Brennan a sensible way to go about this is consider making changes when one part of the portfolio outperforms by at least 10%.

A practical consideration to appreciate, especially if you adopt a regular savings habit, is that you will be constantly investing every month or whenever you have built up enough savings to deploy into your portfolio.

That may mean, in practice you will not need to make any sales in order to reduce weightings, but deploy capital into the parts of the portfolio that have underperformed. This is a far more effective way to rebalance as it involves lower transaction costs.

AN ILLUSTRATION

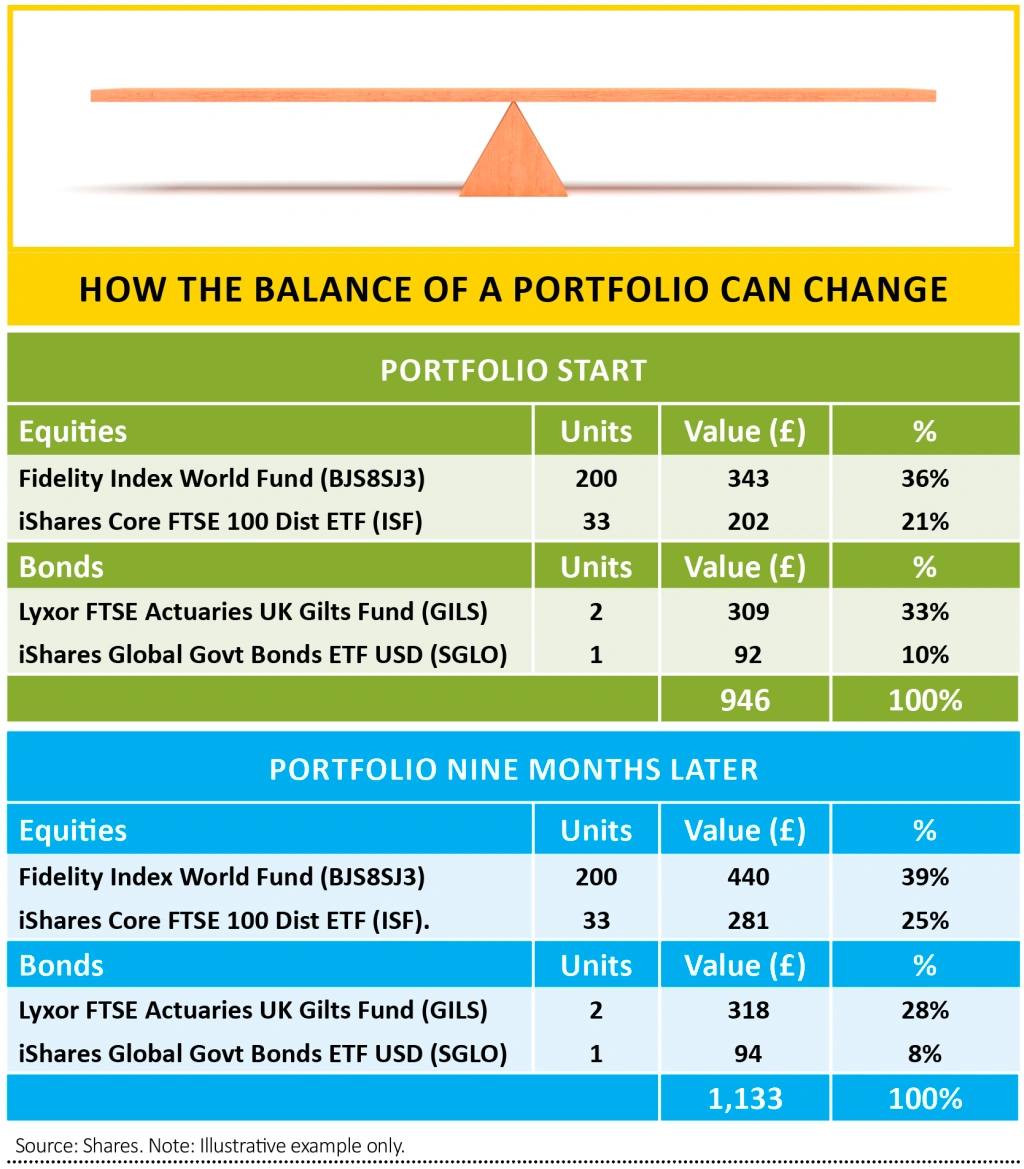

To illustrate the principles, we have put together a random portfolio using passive products and we have allocated 57% to shares and 43% to bonds. This is a relatively conservative asset allocation.

Some of the products cost hundreds of pounds to buy one unit, so you may need to slowly build-up your savings before starting to invest.

With the products illustrated here you would need to save around £1,000 in order to construct the whole portfolio in one go. This makes sense as it allows you to achieve the best asset allocation for your needs from the start.

We have assumed divergent asset returns over the following nine months which has resulted in the shares portion of the portfolio growing from 57% to 64%, around 10% higher, which is the trigger to consider re-balancing the next time you deploy new funds.

Simply purchasing one more unit of either of the bond ETFs would bring the asset allocation back closer to the original position.

The important thing to remember once you have built your portfolio is to keep adding new money regularly or when your financial circumstances allow. Focus on long-term results and use shorter-term market volatility to rebalance your assets.

All the articles in our first-time investor series can be found here

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.