Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

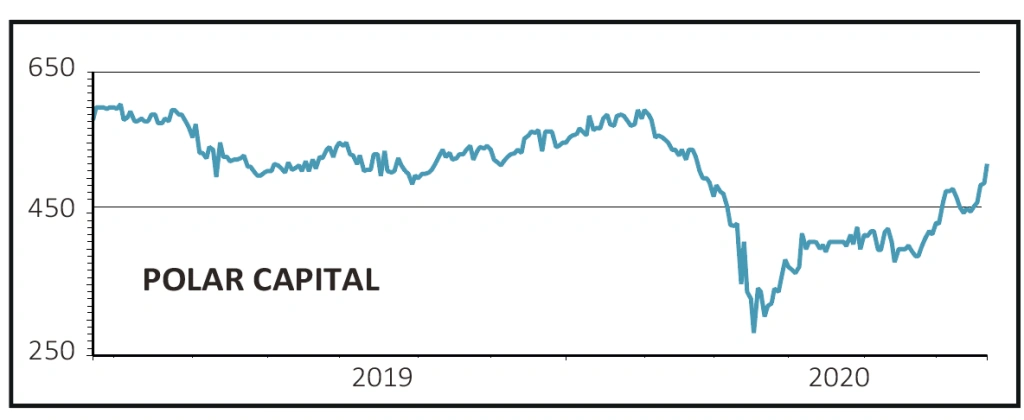

magazinePolar Capital’s shares are up 10% since we said to buy a week ago

Polar Capital (POLR:AIM) 502p

Gain to Date: 10.3%

Original entry point: Buy at 455p on 18 June 2020

Full-year results from the asset manager highlighted good strategic progress while post year-end the business has experienced positive net inflows.

For the year to 31 March, net management fees increased 5% to £119.5 million, in line with growth in the group’s average assets under management (AUM) to £14.1 billion.

However, core operating profit excluding performance fee profit fell slightly to £41.6 million (2019: £42.2 million). This was caused by an increase in staff costs in relation to new team hires and additional distribution capabilities in the US and Nordic markets. In addition, the firm recruited its first chief investment officer and established a central dealing desk.

Over 70% of the company’s funds are ahead of their benchmark for the calendar year to 29 May. Institutional investors tend to focus on longer-term performance and several of the group’s products have achieved a top decile ranking since inception, including the £5.3 billion Polar Global Technology Fund (B42NVC3). Technology-related investments now represent 43% of the group’s AUM.

The company maintains a conservatively managed balance sheet with £108 million of cash at 31 March. This financial strength allowed the company to propose paying a second interim dividend of 25p per share, taking the full-year dividend to 33p per share, equating to an attractive 6.6% yield.

SHARES SAYS: Polar Capital remains a high-quality business. Keep buying the shares.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Premier Foods is in a sweet spot as it breathes new life into the business

- Lam Research is a best in class stock you need to own

- Buy Touchstone now as it gears up for a big increase in production

- Microsoft shares hit new all-time high as it sees little coronavirus impact

- Fresh pork-to-poultry supplier Cranswick continues to sizzle

- Polar Capital’s shares are up 10% since we said to buy a week ago