Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineDown, up, where next? The outlook for investments after a wild six months

The last six months have been extremely turbulent for the markets with significant divergence in performance across different regions, sectors and themes.

The story has been one of topsy-turvy trading with an alarming cliff edge drop in March, as investors capitulated, and then a rapid recovery from these lows.

In this article we take stock of the first half of 2020 in more detail and consider the outlook for those parts of the investment universe which have both outperformed and underperformed through this period.

We address such questions such as:

• Will the US remain in the ascendancy?

• Can the UK play catch up?

• Where next for emerging markets?

We also offer investment ideas to play the themes which we believe will persist in the remainder of the year.

WHY THE TECHNOLOGY BOOM HAS FURTHER TO GO

Covid-19 and its challenges have really put the spotlight on the technology sector. Netflix subscriber numbers have risen sharply and we have all shopped on Amazon for stuff while stores remained closed during lockdown. Some of us, having never made a video call before, have now become minor Zoom experts.

Shares in these three companies have jumped roughly 53%, 48% and 278% respectively so far in 2020. You do not need to be a tech fan to have developed a new appreciation of what technology can do for us, as both ordinary people and ordinary investors.

This attraction to tech is not simply a response to Covid-19. The world’s five largest companies by market value are tech names we all know well, and most of us use. Between them, Microsoft, Apple, Amazon, Google-parent Alphabet and Facebook command a market value of more than $6.2 trillion and produce much of the growth in the US stock market.

This dominance of tech returns did not emerge with the virus; it has been building for years. ‘All the operating profit growth from the S&P 500 over the last eight years is tech,’ says William de Gale, the former BlackRock manager who is now running the BlueBox Global Technology fund.

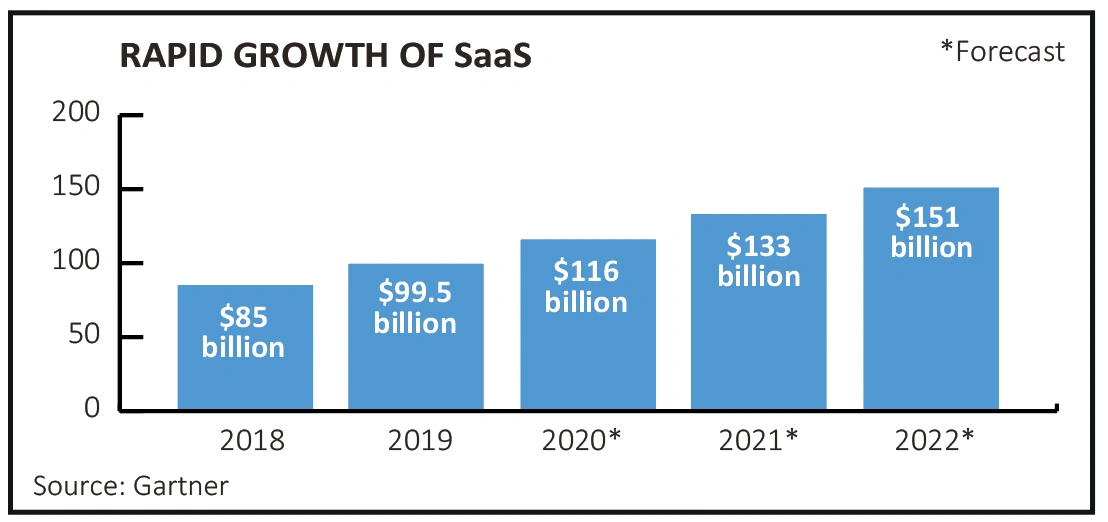

These are essentially digital, flexible, cloud-based platform businesses that can control costs, maintain service standards and still fulfil customer needs during these difficult times, and long into the future. Software-as-a-service (SaaS for short), for example, which effectively means providing IT services over the cloud on subscription, provides the flexibility and scalability valued by users, and the predictability and cash generation loved by investors.

Cloud computing is reshaping the way consumers, businesses and governments use technology to access the exponentially growing mountains of data being created by our modern, inter-connected world.

‘The cost of computing is collapsing’, says Polar Capital fund manager Ben Rogoff, as suppliers with huge investment resources bring scale and processing power.

Fund managers also remain excited about the growth opportunities in artificial intelligence, robotics, complex microchips and digital commerce.

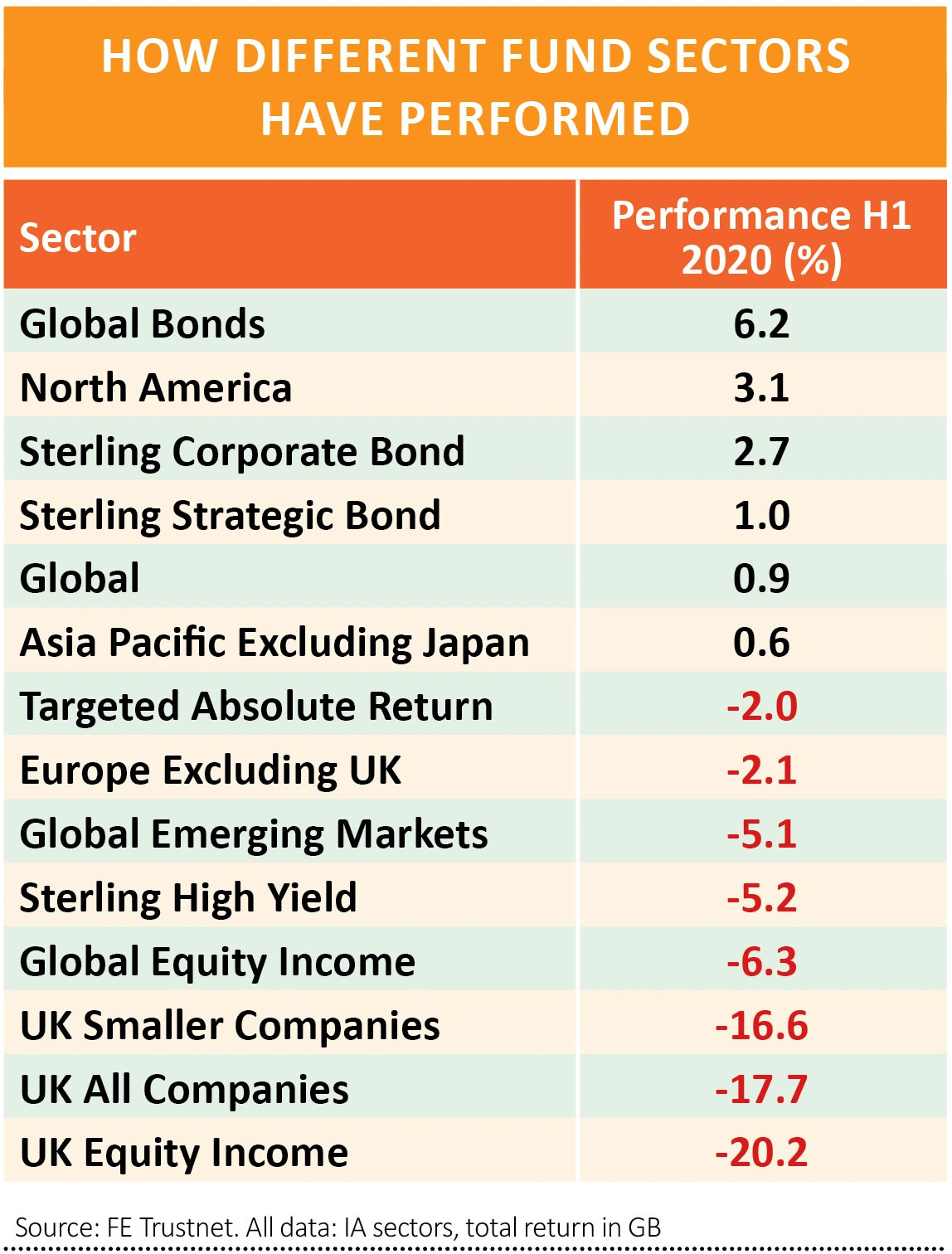

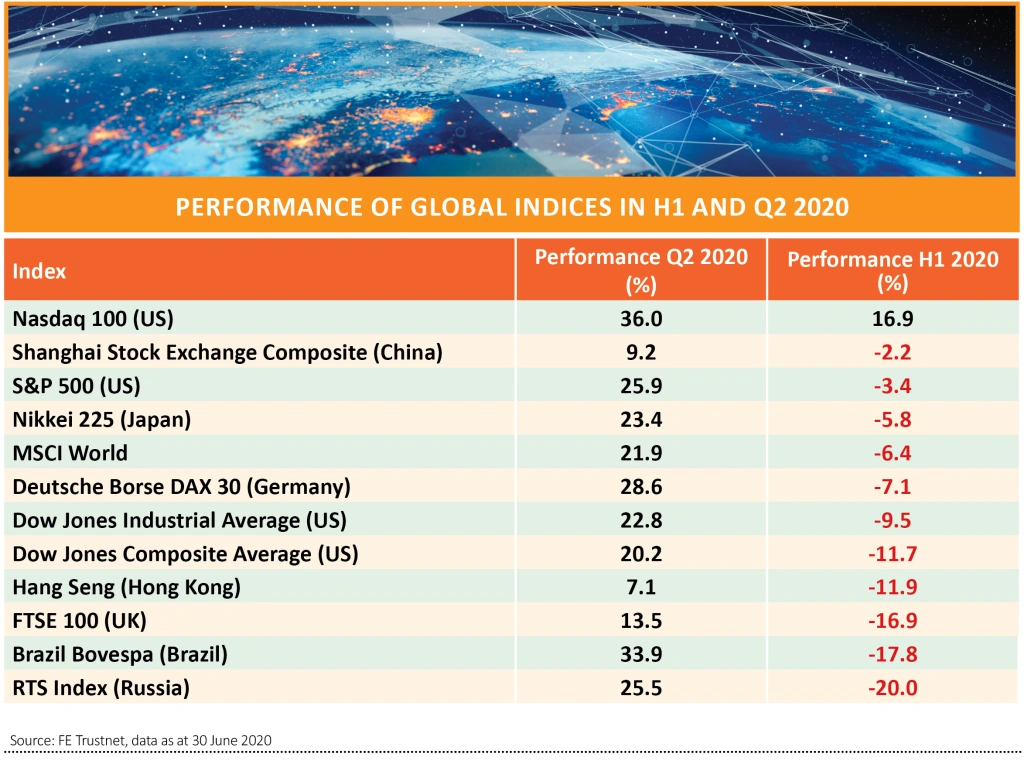

This means that the technology sector has provided protection for investors during the volatility of 2020’s first six months, propping up stock markets and recovering much faster than wider markets. For example, the tech heavy Nasdaq index is up nearly 17% in 2020 having recovered all of its Covid losses by the start of June.

In contrast, Hong Kong’s Hang Seng, the Nikkei in Japan, all of Europe’s major markets and even the S&P 500 in the US, remain down on their pre-coronavirus peaks. The UK’s FTSE 100 is 17% down in the first half of 2020.

The significant allocation to technology in North American and Global funds explains why these sectors have also performed strongly in relative terms this year.

Increasingly, ordinary investors are embracing tech themes, and who can blame them. Data from investment platform AJ Bell Youinvest shows that some of the most bought funds and investment trusts with clients during the first half of 2020 come with technology-laden portfolios.

Collectives like Polar Capital Global Technology (B42W4J8), Polar Capital Technology Trust (PCT) and Baillie Gifford American (0606196) have joined long popular products such as Fundsmith Equity (B41YBWT), Lindsell Train Global Equity (B644PG0) and Baillie Gifford US Growth Trust (USA), which also hold substantial tech names including Tesla, Amazon, Microsoft and Facebook.

Disclaimer: The writer Steven Frazer owns shares in Polar Capital Technology Trust

THE UK'S CATCH-UP CHALLENGE AND THE INCOME CONUNDRUM

The UK was one of the worst performing markets in the first half of 2020. The FTSE 100 failed to keep pace with the recovery seen in other major indices from the low point seen in March.

A material weighting towards banks and oil and gas companies has been a significant factor behind the underperformance of the UK index and could remain a drag on performance in the remainder of the year.

According to the latest figures which run to the end of May, these sectors combined account for more than 15% of the index. If you include financial services that total increases to over a quarter.

Banks have struggled to perform for several reasons and, worryingly for anyone hoping the FTSE can play catch-up in the remainder of 2020, these factors do not look like they are going away soon.

Interest rates have been cut which impacts directly on bank profitability. At the same time lending activity is down as institutions rightly become more cautious about the risk of increasing bad debts in the recessionary environment resulting from coronavirus.

The situation has been exacerbated by the regulator effectively preventing banks from paying a dividend. This reduces investor appetite to own the stock as income has historically been the main reason why people invest in banks.

In the oil sector Royal Dutch Shell (RDSB) cut its dividend by two thirds in April as it responded to the collapse in energy prices brought about by lockdown, and BP (BP.) is widely expected to follow suit when it announces its second quarter results on 4 August. Again, lots of people principally invested in the oil sector for generous dividends and this appeal has now been diluted.

INCOME FUNDS UNDER PRESSURE

The wider wave of dividend cuts, suspensions and deferments has contributed to the extremely weak performance put in by UK Equity Income funds.

The widespread nature of dividend disruption, which to date has involved nearly half the constituents of the FTSE 100, have made it very difficult for managers of income funds to avoid being hit and these funds have been sold down as investors go elsewhere in the hunt for potentially more reliable sources of income.

A POTENTIAL INCOME SAVIOUR

Anyone in this situation should buy shares in Assura (AGR) which invests in GP surgeries and primary care centres.

With the UK Government effectively funding around 90% of its rental income Assura has been relatively unaffected by Covid-19, with the need to reduce pressure on hospitals likely to see further investment in facilities based in the community. This is reflected in a large pipeline of acquisitions and development opportunities for the company.

While a share price of 79p means the shares trade at a near 40% premium to forecast net asset value they do offer a decent and resilient yield of 3.5% based on forecasts from investment bank Jefferies.

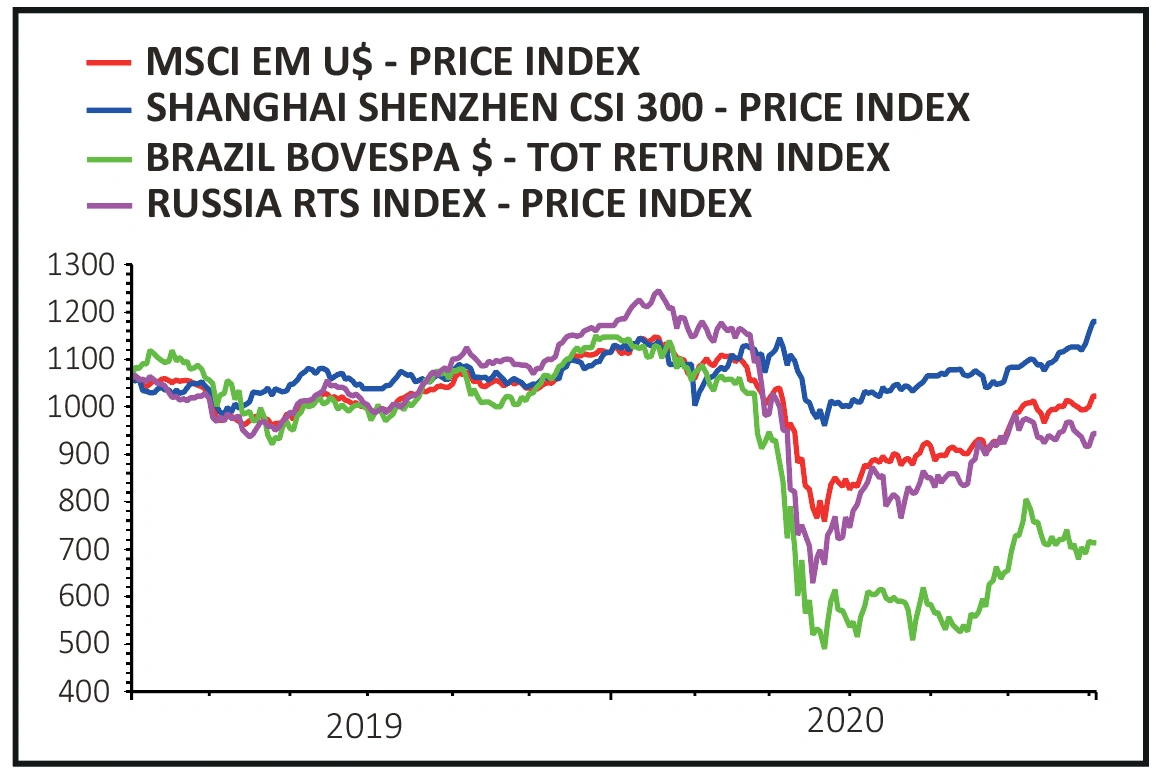

EMERGING MARKETS HAVE DIVERGED DRAMATICALLY POST-COVID

The wild gyrations in emerging markets (EM) in the first half of this year may finally serve to explode the myth that lumping a group of highly diverse developing markets together under one banner makes any sense from an investment perspective.

Anyone who thought emerging markets were created equal, and would therefore react the same way to the coronavirus crisis, had a rude awakening in the second quarter.

The MSCI Emerging Markets index – the most widely used EM benchmark for fund managers and investors alike – is heavily skewed towards China (plus Taiwan), South Korea, India, Brazil

and Russia.

China was the first country to confront the pandemic and was able to impose draconian restrictions on movement, halting the spread of the virus and allowing activities to get back to ‘normal’ well before other countries.

So successful was it at controlling the virus that industrial confidence is back to pre-crisis levels and the latest service sector confidence survey is at a 10-year high.

As a result, China’s CSI 300 index has rocketed from its March lows to a five-year high and has left the rest of the EM basket for dead. Yet the economy is only half the story – six of the top 10 stocks in the EM index are Chinese.

The two biggest stocks are Alibaba and Tencent, which not only make up almost 13% of the benchmark between them but are widely held by global growth funds, especially those with a technology bent. As soon as markets began to recover in late March, investors piled into growth funds and tech stocks.

POOR RELATIONS

In contrast there are two Indian stocks in the top 10 – neither of which has a technology angle – no Russian stocks and no Brazilian stocks.

Russia’s economy and its stock market are inextricably linked to the oil price, which is still down close to half since the beginning of the year, while Brazil not only has the second worst level of coronavirus deaths globally but is suffering increasing political instability, sending investors scurrying for the exit.

After months of outflows from EM funds, Bank of America’s global research team believes the asset class is now a contrarian buy along with commodities, as a counterpoint to weakness in the US dollar.

For investors with a high tolerance for risk, Russia could be a good option. One way of playing this market is JPMorgan Russian Securities (JRS).

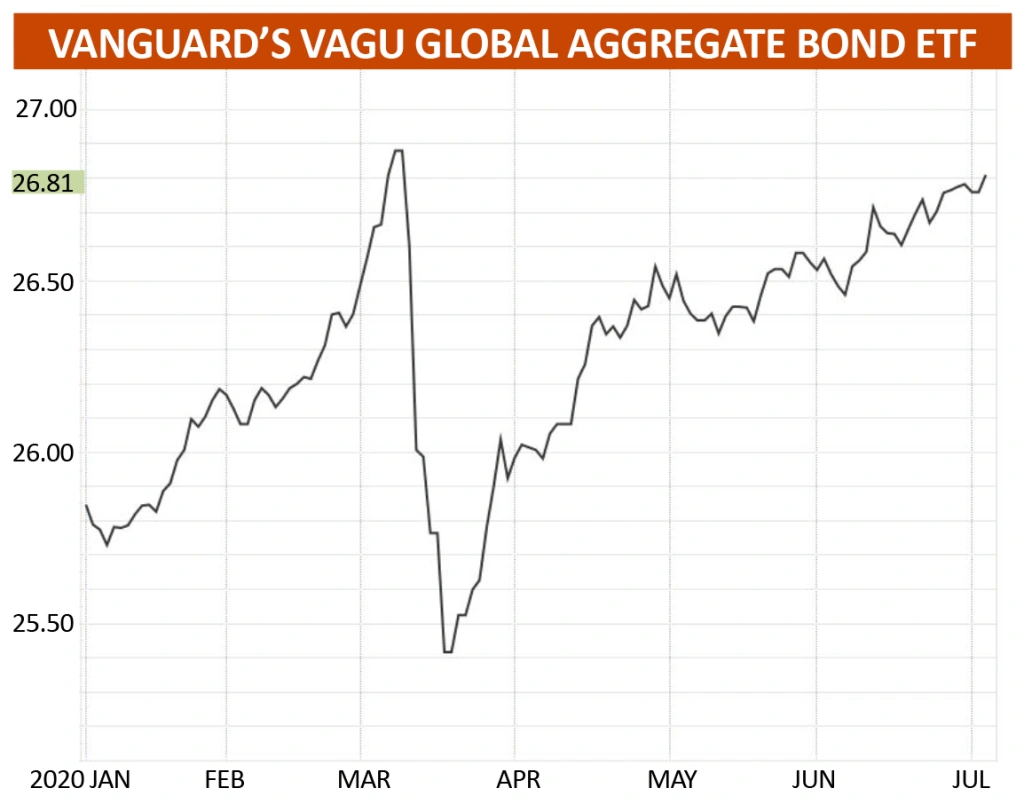

BOND RETURNS LOOK LIKELY TO WANE

Bond markets delivered strong returns in the first half with the Investment Association Global Bonds category up 6.2%, beating most global equity markets. Given the backdrop of ultra-low interest rates and compressed credit spreads, it seems unlikely such a return will repeat itself in the second half.

GOVERNMENT BONDS

Central banks acted swiftly and aggressively in response to the coronavirus pandemic, pushing interest rates down right across the maturity spectrum, from short-dated to 30 years. Bond prices go up when interest rates go down.

Due to the greater sensitivity of long dated bonds to interest rate moves, the long end of the market has seen the lion’s share of the gains. For example the US 30-year Treasury bond has delivered a 20.7% return year-to-date.

By contrast the 10-year Treasury bond is only up just over 1%, which means the interest rate curve has flattened. In the UK, the spread between the 30-year and 10-year bonds has narrowed to only 0.35% compared with 1.5% back in 2012.

With interest rates anchored at such low levels there is little scope for the curve to flatten much further, even if the US Federal Reserve and the Bank of England follow the European Central Bank and entertain negative interest rates.

Ben Edwards, fund manager at BlackRock, doesn’t believe there is much upside from owning government bonds at the current juncture.

CORPORATE BONDS

Corporate bonds are divided into investment grade and non-investment grade or high yield with the distinction being linked to the likelihood of default. Poorer quality companies issue debts with higher yields to compensate for the higher risks. Corporate bonds behave more like shares as the key driver is corporate profits.

At the height of the lockdown the spread between high yield corporate bonds and government bonds hit 12% as investor priced in higher perceived risks of economic distress.

Edwards said the investment grade corporate bond market offered some of the best value he had seen in the middle of March.

The bond buying programme launched by the Federal Reserve which included high yield and bond ETFs for the first time had the desired

effect and pushed high yield spreads back down to 6.5% from 12%.

While there is some scope for corporate bond spreads to shrink further, Edwards believes it has become more of a ‘bond-picking market’ with less value on offer.

WHERE TO PUT YOUR MONEY IN THE BOND MARKET

For investors looking for exposure to bonds, we would suggest focusing on strategic bond funds such as the Artemis Strategic Bond Fund (B2PLJR1).

This fund has the flexibility to invest in the most attractive areas of global bond markets, as well as dial risk up or down according to prevailing market conditions.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.