Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineLuceco knocks the lights out

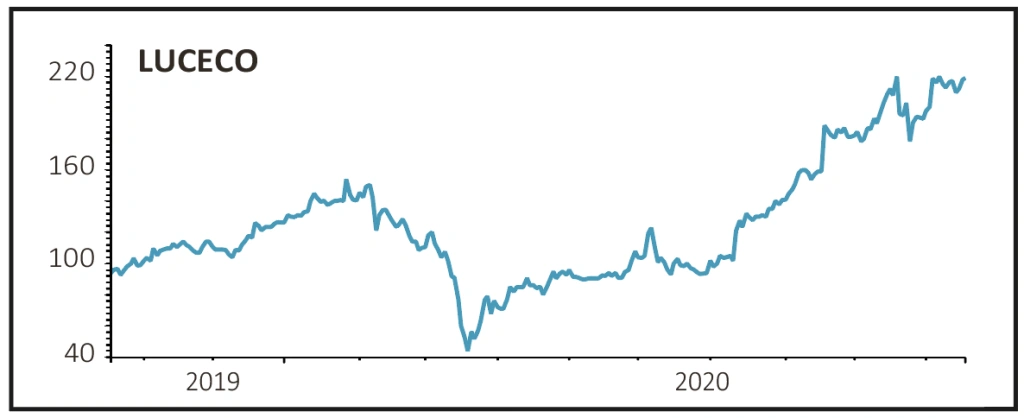

Luceco (LUCE) 245p

Gain to date: 111.2%

Original entry point: Buy at 116p, 19 December 2019

The recovery at LED lighting and portable power products firm Luceco (LUCE) continues to gather pace.

Not for the first time in 2020 Luceco is upping its earnings guidance amid an increase in demand. It now expects full year 2020 adjusted operating profit of between £28 million and £30 million compared with previous expectations for £23 million.

For the quarter ended 30 September 2020, revenue rose 7.5%, better than the low-single digit growth previously forecast, thanks to better than expected demand from online, multi-channel customers and DIY markets.

Third-quarter gross margin was better than expected, with higher sales volumes driving more efficient utilisation of manufacturing overheads, the company noted.

According to Numis analyst Kevin Fogarty the company is benefitting from a ‘structural margin shift, improved business model and near-term earnings growth’. Based on his forecasts the shares trade on a 2020 price-to-earnings ratio of 17.3.

SHARES SAYS: Sales momentum continues with positive implications for earnings growth. While the stock has more than doubled since we said to buy last December, it’s worth running this winner and keeping the shares rather than cashing out now.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

First-time Investor

Great Ideas

- The UK stock market has a new gold giant in town

- More to come from Touchstone despite doubling in price since the summer

- Very large earnings upgrades for Kainos

- Luceco knocks the lights out

- Ford shares start to motor after impressive third quarter trading

- This trust offers big potential if you believe value investing will thrive