Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe underappreciated Baillie Gifford fund achieving stellar returns

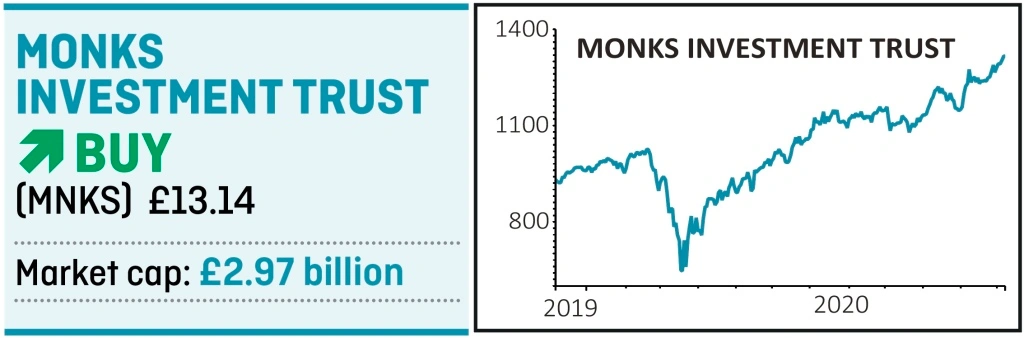

While Baillie Gifford’s flagship investment trust Scottish Mortgage (SMT) tends to hog the headlines, there are other top-performing funds that bring exposure to the highly rated investment management group’s best growth ideas. One high-flying trust that looks particularly compelling is Monks (MNKS), which has a differentiated approach to global growth.

Typically holding over 100 stocks offering a range of different growth profiles, Monks offers investors a diversity of growth drivers which has translated into an outstanding track record. As such, the 3.1% premium to net asset value (NAV) isn’t prohibitive, while a low ongoing charges figure of 0.48% only adds to Monks’ myriad attractions.

STELLAR TRACK RECORD

Rigorous, bottom-up analysis is at the heart of Monks’ investment process, with managers Charles Plowden, Spencer Adair and Malcolm MacColl looking to identify companies with above-average earnings growth.

The team take a long-term view on their holdings as this ensures that the fundamental attributes of a company are given ample time to drive returns and since this trio took over the portfolio in March

2015, Monks’ performance has been outstanding.

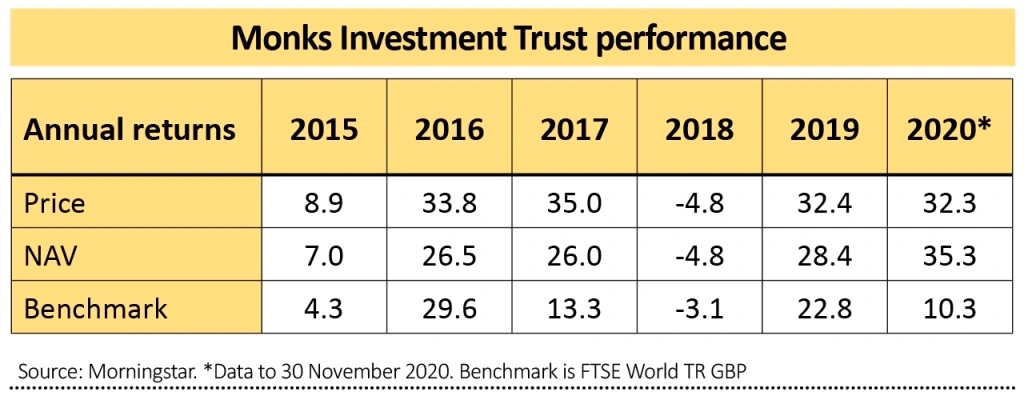

Over the past five years it has achieved 25.8% annualised returns versus 14.8% from the FTSE World total return index, according to Morningstar.

Investec Securities says the trust has ‘a clear and distinct philosophy and a proven investment process’. It adds: ‘Since the adoption of the current approach, the company is ranked seventh out of 263 global open and closed end funds in terms of shareholder total returns. This has enabled the company to establish itself as a core strategic investment for investors.’

Monks significantly outperformed its benchmark in the most recent half-year to 31 October 2020, with net asset value (NAV) growth of 26.8% helping to power the share price 25.7% higher. This represented another knock-out performance versus the FTSE World benchmark, which rose 10.2%.

Unlike Scottish Mortgage, the Monks team take a broader and more diversified approach with over 100 stocks and the largest 10 holdings only account for roughly 21% of the portfolio, providing for a more balanced, global approach.

DIFFERENT FROM THE BENCHMARK

Macroeconomic forecasts or the structure of the benchmark equity index are of relatively little interest to the managers, as the portfolio’s high 86% active share demonstrates.

Active share is a measure of how different a fund’s holdings are from its benchmark – being the index against which performance is measured.

If a fund had no holdings at all in common with its benchmark, it would have an active share of 100%, and if all its holdings were the same as the benchmark, its active share would be 0%.

DIVERSIFIED GROWTH DRIVERS

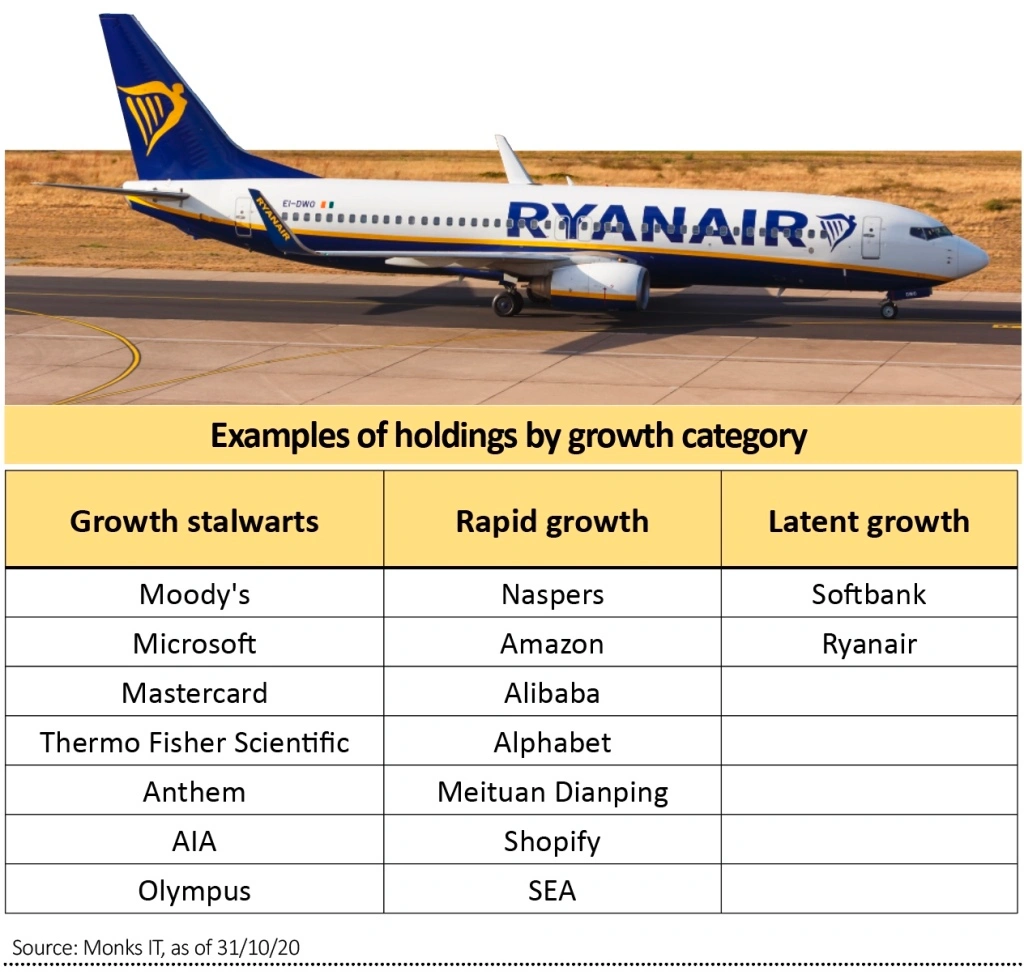

Monks’ portfolio contains four distinct categories of growth stock: ‘Stalwart’, ‘Rapid’, ‘Cyclical’ and ‘Latent’. At around 25% of the portfolio, growth stalwarts are names considered to have a durable franchise generating earnings growth of around 10% per year, such as Microsoft and Mastercard.

Over half of Monks’ portfolio is invested in rapid growth stocks. These are companies in the early stage of their business cycle with a vast growth opportunity ahead, typically delivering 15% to 25% earnings growth per year.

Cyclical growth names are delivering 10% to 15% growth over the economic cycle, with common characteristics including a significant structural growth opportunity and a strong management teams with proven capital allocation pedigree.

The latent growth bucket currently includes SoftBank and Ryanair (RYA). Here, you’ll find out-of-favour companies with a specific catalyst that could drive above-average earnings in the future.

Investec points out that in recent years there has been a distinct rotation away from cyclical to the rapid growth category, although Monks’ managers have good valuation discipline too. They will sell if future growth is fully reflected in the price of a holding, as happened with the recent sales of fast-food chain Chipotle and payments group Visa.

NEW ADDITIONS

Recent investments include the likes of online furniture seller Wayfair and music streaming platform Tencent Music Entertainment, a joint venture between Chinese social media platform Tencent and Spotify.

Plowden has also ploughed cash into cloud service businesses, among them Snowflake, Cloudflare, Datadog and Twilio, as well as online travel agency Booking and car sharing company Lyft.

Sports apparel company Adidas and cosmetics firm Estee Lauder have also been added to the portfolio in the belief both brands will emerge in a stronger position post-pandemic.

Monks has also put money to work with mining giants BHP (BHP) and Rio Tinto (RIO) to add diversity of growth drivers to the existing portfolio, while also upping its stake in low-cost airline Ryanair.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Exchange-Traded Funds

Feature

First-time Investor

Great Ideas

Money Matters

News

- Supply chain issues could mean a bleak winter for UK consumers

- Big Goco shareholder Peter Wood throws weight behind Future tie-up

- Questions still linger over National Grid and SSE dividends

- Key catalysts for markets before the end of 2020

- Flutter Entertainment secures prize US asset

- Fast growing hydrogen stock Ceres gets closer to fulfilling its potential