Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineUS retail titans smash forecasts as Christmas comes early

Investors in US retail names have grounds for optimism given the latest retail sales figures from the across the pond and positive earnings updates from dominant players including Walmart.

US retail sales rose by 1.7% in October, according to the Commerce Department, beating forecasts of 1.4%, as shoppers start their holiday shopping early to avoid empty shelves as the pandemic squeezes supply chains.

High inflation has yet to dampen spending with rising household wealth, driven by a strong stock market and house prices, savings accrued during the pandemic and wage gains, shielding American consumers from the higher cost of living.

However, consumers are now eating into those savings as they spend on leisure activities or return to costly commutes at a time when food and fuel prices are rising sharply.

Investors need to consider how much of the past month’s spend was brought forward as gift-givers rushed to make sure they had what they want to sit under their Christmas trees amid warnings over supply shortages.

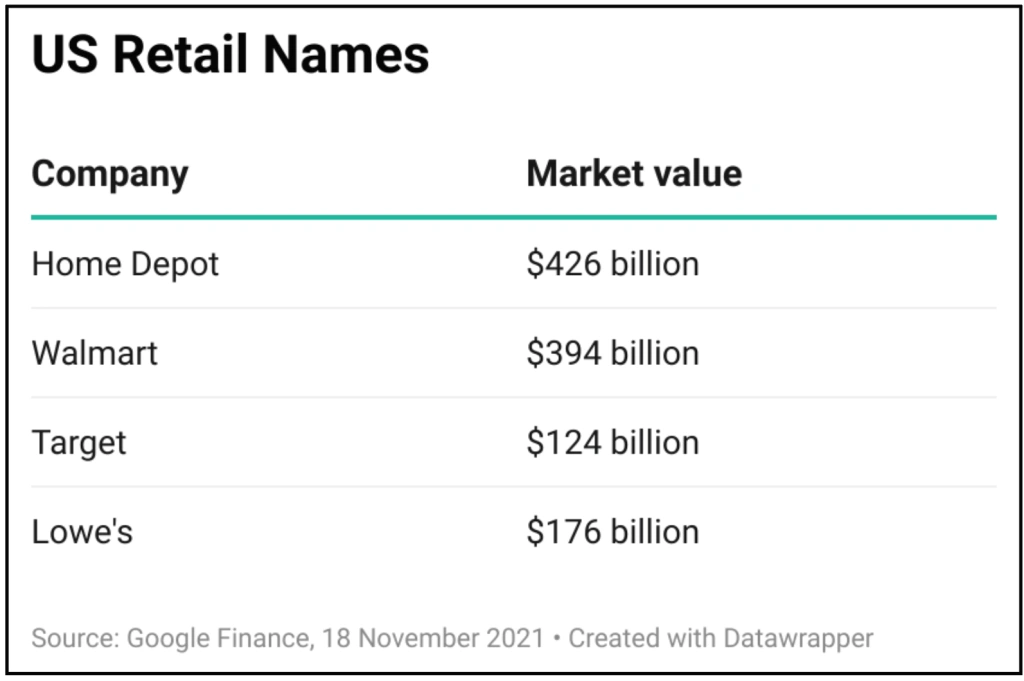

At the same time, it is important to note that scale matters in retail and the likes of Walmart, Target, Home Depot, Lowe’s and Costco have the resources to charter ships that smaller competitors don’t, which is helping them to mitigate challenges ranging from port congestion to staff shortages.

KEEPING PRICES LOW

Despite delivering impressive third quarter performances which beat Wall Street expectations, shares in both Walmart and Target fell after they posted earnings as the pair pledged to absorb some of the higher costs of shipping, materials and wages rather than pass them on to customers.

Walmart and Target are playing the long game, attracting new customers with sharp prices to build consumer loyalty and maintain sales momentum, although failing to pass on price increases comes at the expense of margin and short-term profitability, which is irking impatient investors.

Third quarter sales were up by more than analysts had been anticipating at Walmart, one of Shares’ running Great Ideas selections, which has ‘Every Day Low Price’ at the cornerstone of its strategy.

The company reported 9.2% growth in US comparable sales excluding fuel for the 13 weeks ended 29 October, up by 15.6% on a two-year basis, and raised full year guidance.

Walmart also reported US e-commerce sales growth of 8% for the quarter and impressive 87% growth on a two-year basis, and assured that its US inventory was up 11.5%, which is reassuring with Christmas approaching.

‘Our momentum continues with strong sales and profit growth globally,’ said Doug McMillon, president and CEO of the US supermarket giant.

‘Our omnichannel focus is pushing digital penetration to record levels. We gained market share in grocery in the US, and more customers and members are returning to our stores and clubs around the world. Looking ahead, we have the people, the products, and the prices to deliver a great holiday season for our customers and members.’

MORE THAN FOOD

General merchandise seller purveyor Target also has keen pricing at its core – the company’s tagline is ‘Expect More, Pay Less’ – and uses its groceries business to drive traffic to its stores, where it can sell consumers higher margin non-food products.

Third quarter comparable sales grew 12.7%, on top of the 20.7% growth generated in Q3 a year earlier, reflecting like-for-like store sales growth of 9.7% and comparable digital sales growth of 29%.

Confident it is both stocked and staffed for Christmas, Target also upgraded its fourth quarter comparable sales guidance to high-single digit to low-double digit growth, up from previous guidance for a high-single digit increase.

Chief executive Brian Cornell continues to expect a full year operating income margin of 8% or higher from Target.

‘Following comparative growth of nearly 21% a year ago, our third quarter comparative increase of 12.7% was driven entirely by traffic, and reflects continued strength in our store sales, same-day digital fulfilment services and double-digit growth in all five of our core merchandising categories,’ says Cornell.

RIDING THE DIY BOOM

While shares in Walmart and Target weakened, Home Depot’s stock topped the S&P 500 leader board following forecast-beating third quarter sales and earnings.

By responding to the elevated DIY demand engendered by the pandemic the home improvement giant’s market value has overtaken Walmart’s for the first time.

And despite concerns that DIY-ers might have done all they needed to during the pandemic, Home Depot continues to benefit from the tailwinds of US housing market strength and the structural work from home trend.

Home Depot’s same-store sales grew by a forecast-beating 6.1%, despite a testing prior year comparator, with US like-for-like sales up 5.5%, as customers splashed the cash on home improvement projects, with management flagging continued strong demand as the company entered the fourth quarter.

Smaller rival Lowe’s beat expectations for third quarter sales and earnings alike, and once again raised its 2021 outlook after a holiday shopping boom came early and results were boosted by online sales and high demand from contractors and electricians. Same-store sales edged up by 2.2%, confounding expectations for a decline against demanding comparatives.

‘Our momentum continued this quarter,’ said CEO Marvin Ellison, ‘with US sales comps up nearly 34% on a two-year basis, as our Total Home strategy is resonating with the Pro and DIY customer alike.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

Great Ideas

- DotDigital share slump means you can buy cheaper now

- Growth, profit and M&A to drive CentralNic higher

- Plenty of reasons to remain positive on Euromoney

- The smart way to play a rebound in the Chinese stock market

- All-weather trust Ruffer is selling new shares at a discount

- Investors overreact to Frontier Developments' downgrade