Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

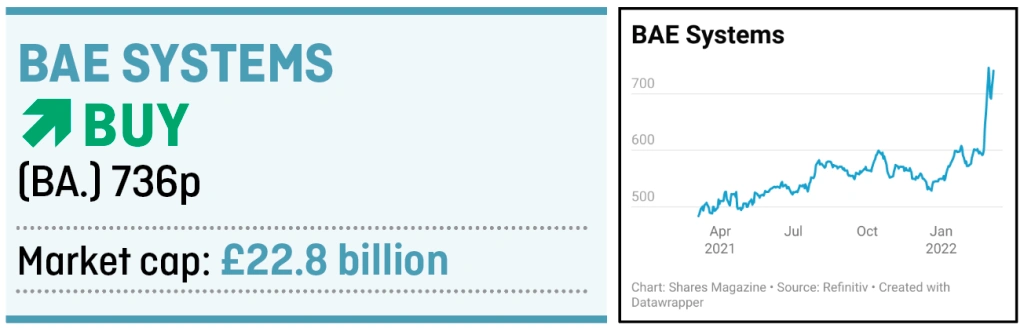

magazineBAE to benefit as global defence spending ramps up

The irony of calling a defence company a safe haven while war rages in Ukraine is not lost on Shares yet this is what we believe BAE Systems (BA.) stock offers investors in these troubling times, and importantly, for the longer-run.

Few reasonable investors would feel comfortable buying a stock based purely on the impact of what is clearly an escalating human tragedy but what the conflict does show is that there are significant long-term opportunities for the UK-listed FTSE 100 company, and that’s what investors should focus on.

A LEADING GLOBAL DEFENCE CONTRACTOR

BAE is one of the largest defence contractors in the world, with one of the most substantial portfolios of defence technologies covering land, sea and air.

Latest company data shows a skilled workforce of around 90,000 people in more than 40 countries, developing, engineering, manufacturing and providing support for military capability and national security systems that helps keep critical information, infrastructure and people secure.

There can be little doubt that the world is on the cusp of a significant increase in military and defence spending over the coming years, a direct response to Russia’s attack on its neighbour.

Last month Germany announced plans to hike its own military spending to at least 2% of its gross domestic product from an estimated 1.53% in 2021, according to NATO statistics, earmarking an extra €100 billion in its 2022 budget.

Germany is unlikely to be alone. Analysts at Jefferies have calculated that if all NATO members were to raise defence budgets to 2% of GDP it would imply a 25% increase in overall spend, excluding the US, which would trigger significant benefits across the entire industry.

The US already has the world’s largest defence budget, with an estimated $750 billion earmarked for 2022. That’s more than three times the $237 billion that number two China is expected to spend this year, yet analysts still anticipate substantial US budget growth. Berenberg analysts forecast an 8% increase in 2023 above this year’s President’s Request and think there is ‘growing support to go higher.’

SEA-CHANGE IN SPENDING

This marks a sea-change versus prior expectations for flat or declining military budgets and it bodes well for BAE both in terms of driving future earnings growth and a higher rating. The shares are now trading on 2022 and 2023 price to earnings multiples of 14.5 and 13.8, based on Berenberg forecasts.

BAE’s strategy is comprised of five key long-term prongs centred on maintaining and growing core franchises and securing growth opportunities:

– Sustain and grow its defence and security businesses

– Ongoing growth in adjacent markets

– Develop and expand its international business

– Inspire and develop a diverse workforce to drive success

– Enhance financial performance and deliver sustainable growth in shareholder value

BAE’s products and services range from ballistic missile firing systems, armoured vehicles, combat ships, Typhoon and F-35 fighter jets, communication systems and much more, including its growing FAST Labs Cyber Technology digital security and intelligence business. This arm should help future-proof the group as emerging threats in the cybersecurity space become more of an issue.

As a primary contractor for the UK’s Ministry of Defence BAE holds a key edge over global competitors when bidding for MoD contracts, while the UK Government owns a golden share in the business, effectively giving it the ability to veto any corporate actions it does not agree with.

UNIQUE RISKS

But there are unique risks. The global defence industry is highly regulated and controlled and BAE must be careful to stay on the right side of regulators to maintain its presence in the market. If it falls foul of these rules, it could be barred from future programmes and cut-off from its existing customers.

It is also a competitive space. There are strict rules about how contracts are bid for and awarded and while it may be among the go-to contractors for the UK, defence departments could favour local suppliers elsewhere, particularly in the important US market.

Maintaining its advantages will require a lot of ongoing research and development spending which could depress future returns. Capital expenditure in 2022 is forecast by Berenberg at £520 million, rising to £560 million by 2024, versus £477 million and £462 million in 2020 and 2021 respectively.

That said, BAE has typically earned returns on capital employed, or ROCE, in the mid-teens, meaning that it has a proven track record of getting value for money for shareholders from what it spends.

A final point worth thinking about is that BAE’s improving margins and operational execution are turning the company into an increasingly cash generative one. Berenberg estimates range from £1.68 billion to £1.98 billion of free cash flow in each of the next three years, versus the £689 million earned in 2020, meaning that growth in future dividends looks secure and could be bolstered by share buybacks down the line.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.