Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

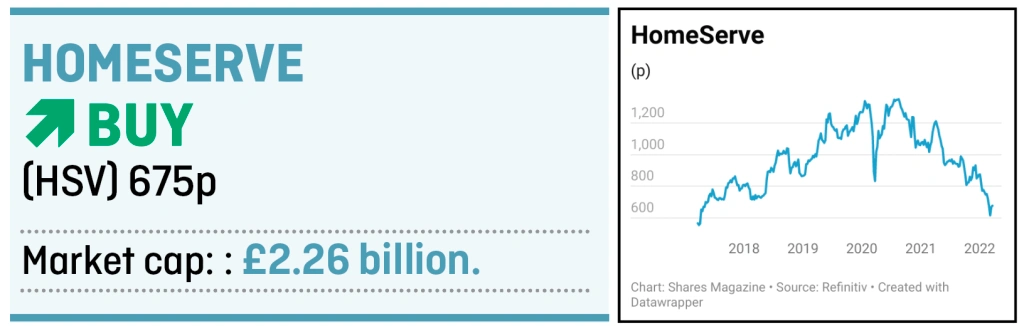

magazineUS growth can drive undervalued Homeserve shares higher

Shares in business services group HomeServe (HSV) have been oversold on concerns surrounding the growth prospects in the UK.

However the star performer is the US business, and management has indicated that it is currently ahead of schedule in achieving its medium-term target of $230 million of earnings before interest and tax from this region.

And while the domestic operation has been losing customers, this should start to bottom out as it works with water partners to enhance its product offering.

All in all the shares offer good value at current levels. The current squeeze on consumers’ finances caused by rampant fuel and food price inflation is likely to encourage more people to take out policies in order to avoid large repair bills.

The share price has fallen by 31% over last six months, which explains why the stock is trading on 2022 price earnings of 13 times, falling to a price earnings multiple of 12.1 times for 2023.

The 5 April pre-close trading update is likely to act as a catalyst for the shares.

Homeserve has two business lines. It sells homeowners insurance against unexpected plumbing, heating or electrical emergencies. This model works by selling these products through partnerships with utility companies, and has expanded from the UK into France, North America and Spain.

It also provides qualified tradespeople to sort things out if there’s a problem. Homeserve also runs the Checkatrade platform, charging tradespeople to advertise.

The share price weakness largely relates to concerns surrounding the UK business which has been hampered by a series of setbacks.

In 2021 it took an £85 million provision to write off its customer relationship management platform, which was no longer fit for purpose, hammering earnings.

The UK business is mature and customer numbers fell to 1.6 million at the end of 2021. However broker Liberum anticipates that it will trough shortly at 1.5 million customers.

Management are confident in the group’s ability to increase the number of US customers from the first half 2022 level of 4.8 million to a Milestone 2 target of six million to seven million.

According to Liberum double that figure is achievable long term.

Assuming that 30% of the market is insurance minded and that there are 151 million households in the US, the addressable opportunity is 45 million households

If HomeServe maintains its share it should be able to increase the number of customers from 4.7 million to 14 million.

There are a number of reasons to believe these projections are achievable.

HomeServe has a proven operating model, a strong balance sheet and is targeting the acquisition of 28 utility books. It also has 72 million affinity partner households in the US.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

- Why Magners maker C&C can cope with unprecedented cost inflation

- Fighting cyber attacks: Invest in the world's digital defenders

- Which is better - high yield today or dividend growth tomorrow?

- New world order: the big impact of a geopolitical earthquake

- Private equity has made a lot of people rich – how do you get invest in it?

Great Ideas

- BlackRock Throgmorton is a great fund for a small cap recovery rally

- Cordiant Global Infrastructure remains a way to play the growth in digital assets

- Why Berkshire Hathaway is hitting fresh highs

- FDM shows substantial recovery potential at shares rally 21% in two weeks

- US growth can drive undervalued Homeserve shares higher

- Essentra to become a streamlined components champion

News

- Chancellor Sunak’s spring statement full of surprise support measures

- Ferguson to leave the FTSE 100 in May as it focuses on the US

- Robust results from Nike as direct to consumer strategy delivers

- IG and Plus500 venture overseas with mixed success

- Hospitality enjoys good times despite spending pressures

- Value and inflation protection leave FTSE 100 well placed

- Hong Kong suspends shares in Chinese property giant Evergrande