Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThree ways to boost your retirement savings

Increasing life expectancy means we are living for longer than ever before. According to Office for National Statistics data, people aged 65 in 2020 on average can expect to live for another 20 years or more, and for those in very good health, it’s statistically quite possible that many will hit 100 years of age.

We will need financial support when we stop working and the state pension is unlikely to provide enough income for most of us. While spending might fall in your 70s, there are still large care and health costs to consider. Some people will also want to weigh up their options for passing money onto children and grandchildren.

You need at least 10 years’ worth of National Insurance contributions to get any state pension and to get the full £185.15 a week you need at least 35 years of National Insurance contributions.

Currently you need to be aged 66 to receive the state pension but there is gradual rise to 67 for those born on or after April 1960; and a further gradual rise to 68 is planned between 2044 and 2046 (subject to review) for those born on or after April 1977. Many of us are aiming to work less or not at all before reaching that age range.

It’s important to monitor your finances. It is worth looking to see if you can pay more into your personal retirement savings now as getting into good habits could make a big difference in later life.

THREE ROUTES TO CONSIDER

Thinking about how to improve your retirement savings needn’t be complicated. Here are three routes to consider:

Option 1 – pay more into your workplace pension

Option 2 – pay additional contributions into a personal pension

Option 3 – pay additional payments into a Lifetime ISA if you qualify for this type of account

We’ll look at each of these in more detail later but the first step to take is a little financial housekeeping.

GETTING YOUR FINANCES TIDY

You should initially think about paying off expensive debts, such as credit cards or personal loans, whose interest rate charges can eat savagely into your savings.

According to personal finance website NimbleFins, the average interest rate on UK credit cards was 21.5% as of January 2022. Paying off these debts makes a lot of sense.

You also need to consider an adequate emergency fund for those bills that hit you out of the blue. Six months of your monthly spending is an appropriate amount to target.

Things like repairs to your home or needing to fix the car can incur hefty bills so it is best to have a pot of cash set aside to help with these sudden costs.

Once you’ve addressed these points, the next step is to consider if any extra savings you desire are exclusively for retirement or if you might want access to the money earlier in life, perhaps for projects like extending the house or paying university fees for your children.

If this is the case, an investment-focused ISA might be more appropriate place for any extra savings as there are no restrictions on withdrawals which you find with a pension or Lifetime ISA.

However, payments into an investment-focused ISA such as a Stocks and Shares ISA do not qualify for tax relief or government bonus which you find with pensions and Lifetime ISAs respectively – we explain these bits in more detail later on.

HOW MUCH MONEY DO YOU NEED IN RETIREMENT?

For those happy and able to contribute more to their retirement savings, how much do you need in later life? This may seem a difficult question to answer, especially if retirement is years away.

A common perception is that you’ll need between half and two-thirds of the final salary you had when you were working, after tax, to maintain your lifestyle once you retire. This is because you will have likely paid off the mortgage, will no longer be bringing up children and won’t face the cost of commuting once you stop working.

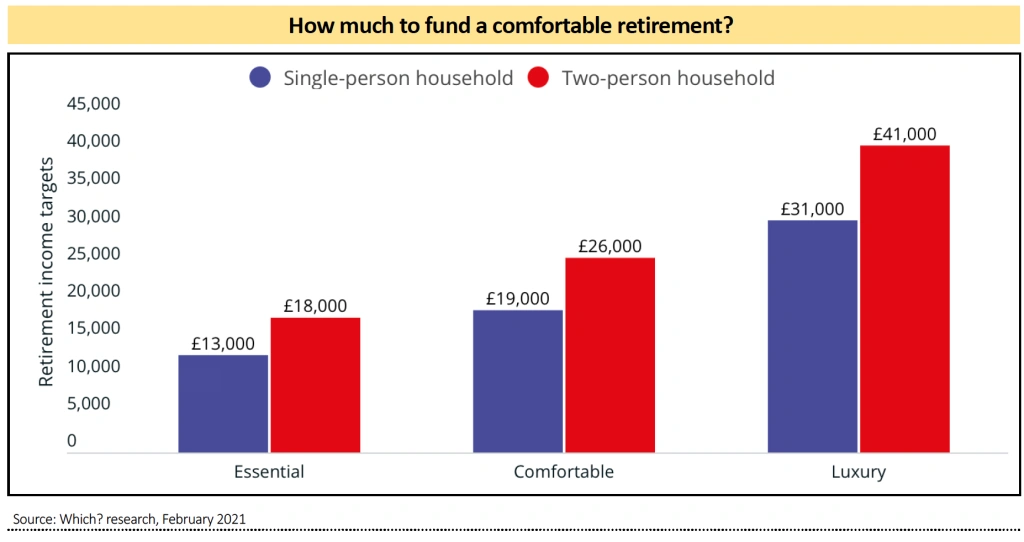

According to a Which? survey of more than 6,800 retirees conducted in 2021, the average two-person household spent around £26,000 a year, or a little less than £2,170 a month on a reasonably comfortable lifestyle. This covers all the basic day-to-day costs of living, such as utility bills, groceries and council tax, with a few luxuries too, such as holidays, hobbies and eating out.

Couples after a more extravagant retirement lifestyle spent around £41,000 a year or £3,420 a month if you include luxuries such as more exotic holidays and a new car every five years.

The equivalent spend for single individuals in the comfortable category was £19,000 a year, or £31,000 for a more luxurious lifestyle. Some people might be comfortable with a more frugal lifestyle than these illustrations and others might have circumstances that require greater funding, but the data does provide a useful rule of thumb.

SELECTING A TAX WRAPPER

– Option 1 –

Join your employer’s workplace pension. Given the government also tops up your contributions through tax relief, a workplace pension is one of the most important ways to build up wealth for later in life.

Under the government’s auto-enrolment scheme introduced in 2012, if you’re at least 22 years old and earn more than £10,000 a year then your employer will have to automatically enrol you in a pension scheme into which you and they must contribute.

You can opt out but doing so means you won’t benefit from your employer’s contributions, missing out on what is effectively free money. If you don’t have access to an employer’s pension scheme, perhaps because you’re self-employed, you can still contribute to a personal pension and benefit from tax relief on your contributions.

Workplace pension schemes offer a choice of funds to invest in and you may get to choose how much of your contribution goes into each fund. However, the rules and range of fund options may differ depending on your company scheme, so you’ll need to check the options available to you.

For example, the Standard Life Managed Pension Fund aims to provide long-term growth by investing in a diversified portfolio of assets including shares, bonds, property and cash.

The share component of the fund is selected both in the UK and from overseas markets and currently includes well-known companies like Microsoft (MSFT:NASDAQ), AstraZeneca (AZN) and Apple (AAPL:NASDAQ). For the five years to 31 December 2021, the fund returned 35.5%, according to FE Fundinfo.

– Option 2 –

A SIPP, also known as a self-invested personal pension, can be run alongside your workplace pension or on its own if that is not an option. With a SIPP, you are responsible for picking your own investments.

UK residents can pay in 100% of their earnings up to a maximum of £40,000 each year into a pension and receive tax relief. Unused allowances from the previous three years can be carried forward but a maximum of 100% of earnings can be paid in any one tax year.

You’ll receive tax relief at the basic rate of 20% on personal contributions made to pensions. So, for every £80 you pay in, the taxman will top it up to £100. If you’re a higher or additional rate taxpayer, you can claim back up to an additional 20% or 25% respectively through your self-assessment tax return.

There is no tax payable on any growth or income related to your pension. But usually you will be taxed on 75% of withdrawals when you come to take money out of the pot.

A SIPP can be useful if you already have a broadly-based selection of investments through a workplace pension but want to add a little more spice or security to your portfolio. It will enable you to access a far larger selection of investments than workplace schemes which typically have a limited number of funds.

With a SIPP, you can choose from a range of low-cost exchange-traded funds that track an index, so you get wide exposure to a market or investment theme.

Vanguard and iShares, for example, offer a large range of ETFs, such as the Vanguard FTSE All-World UCITS ETF (VWRP) which tracks a basket of larger companies from around the world, or the iShares FTSE 100 ETF (CUKX) which focuses on matching the returns of the FTSE 100, an index of the largest companies on the UK stock market.

SIPPs also give you the opportunity of investing in a broad range of funds and investment trusts, as well as thousands of individual companies.

There are downsides. The choice can be mind-boggling and picking your own investments may be a bigger responsibility than you are ready to take on.

– Option 3 –

You might want to consider using a Lifetime ISA to make additional payments to retirement savings.

A Lifetime ISA is a tax wrapper open to anyone aged between 18 and 39, although once an account is live you can contribute each year until age 49.

You can pay in up to £4,000 per tax year to a Lifetime ISA and the government will add a 25% bonus on top of the money you save. So, a payment of £4,000 from yourself would quality for a £1,000 bonus from the government. Any growth or income within the Lifetime ISA will be free from income tax and capital gains tax.

The £4,000 contribution counts towards your overall annual ISA allowance of £20,000.

Although you don’t pay any tax on any withdrawals from a Lifetime ISA, you may pay a penalty if you withdraw in certain circumstances.

Whereas pensions can be accessed from age 55 (or 57 from 6 April 2028), to withdraw money from a Lifetime ISA without penalty means waiting until age 60 unless the money is used towards your first home or you are terminally ill.

Anyone who withdraws money from a Lifetime ISA for any other reason before reaching age 60 will be charged a 25% penalty fee.

– Option 4 –

Earlier in this article we said there were three key routes for saving extra money for retirement. There is a fourth which involves saving into a Stocks and Shares ISA.

On a positive note, you can put £20,000 of money a year into this type of ISA a year versus £4,000 for a Lifetime ISA. You can withdraw the money at any time and without penalty which is positive – although this also raises the temptation of dipping into the pot before you hit retirement.

WHICH TYPE OF INVESTOR AM I?

If you put a group of people in a room, there would most likely be a range of different attitudes towards the type of stocks or funds individuals would be willing to choose.

Some people would be happy taking high risks in the quest to get higher returns; others are less adventurous and don’t want to see their money lose value if markets go through a bad patch.

There’s no right or wrong, it’s down to the individual to decide what kind of investments they want to make, what kind of risk they are happy to accept, and which tax wrapper would suit them best. This is essential when working out an investment strategy.

In simple terms, investors often fit into one of the following categories:

Cautious – A desire to put money into investments that won’t experience wild price swings up and down

Balanced – Investors who want steady growth and are less concerned about short term market movements

Adventurous – investors who want to put money into higher risks stocks or funds to achieve higher returns

Let’s look at two examples that help to illustrate certain types of hypothetical investor:

THE BALANCED INVESTOR

Julie is 28 and lives in rented accommodation in Leicester. She is a qualified audiologist and is in full-time employment.

She wants to buy a house worth £270,000 and needs £27,000 for a deposit. She already has £25,000 in a Cash ISA which is combination of gifts and inheritance from family members.

Julie has just opened a Lifetime ISA and can afford to save £150 a month into it. After 11 months she will have contributed £1,650 into the account which qualifies for an extra £412.50 from the government, totalling £2,062.50. Julie needs to have the Lifetime ISA funded for 12 months before she can use it to purchase a property.

Given it will take just under a year to hit her goal of having enough money for the property deposit, Julie is already thinking about building on this savings habit. She plans to continue investing money into her Lifetime ISA once the property is bought and to use these contributions for retirement.

Julie believes it is too risky to invest the money for the property deposit in the stock market given the short timeframe and so those savings are kept in cash. However, for the retirement savings she is happy to take the risk of having money invested.

She already has exposure to a mixture of larger companies and bonds through her workplace pension and would like to use her Lifetime ISA to add exposure to infrastructure and smaller companies. In doing so, she would add a blend of lower and high-risk investments respectively.

Infrastructure funds typically put money into assets crucial to a country’s development such as roads, energy and water treatment facilities. One way of getting broad exposure to this space is via exchange-traded fund iShares Global Infrastructure ETF (INFR) which tracks an index of infrastructure companies from developed and emerging market countries.

Smaller companies can grow faster than larger companies, giving a potential boost to an investment portfolio which has exposure to this part of the market. There are higher risks because smaller companies often need additional funding to achieve their growth goals and many are loss-making while they try to gain scale. But historically they’ve often outperformed larger companies when looking at a long period such as 10 years.

For example, the Numis Smaller Companies index (including AIM but excluding investment companies) generated a 127% total return for the 10 years to 22 April 2022 versus 91% from the FTSE 100 index, according to Fe Fundinfo. Total return accounts for share price gains/losses and dividends.

One option for Julie is to look at exchange-traded fund SPDR MSCI World Small Cap UCITS ETF (WOSC). This tracks an index of smaller companies in developed equity markets globally.

THE ADVENTUROUS INVESTOR

32-year-old Adam is a chemical engineer in Whitby Bay and puts aside £200 to £400 a month into a bank-based savings account.

Adam has a well-paid job, 20 years left on his mortgage and over the years he’s dabbled in the stock market buying technology stocks and in cryptocurrencies. He knows his cash in the bank is not earning much interest and now is the time to start seriously thinking about putting the money to work for the longer term.

His workplace pension is spread across various assets and geographies, so Adam is comfortable there is a solid backbone to his retirement saving plan.

He decides to do two things: first, he increases the contribution to his workplace pension; second, he decides to open a self-invested personal pension to hold individual stocks.

By having a SIPP, Adam can continue to use his knowledge of the tech sector to buy and sell individual stocks and not have to pay any capital gains or income tax on these investments.

He accepts that buying individual shares is risky and so he adds a few tech-themed investment trusts and exchange-traded funds to his SIPP to provide more diversification.

One option for Adam is to look at an investment trust where a fund manager is actively looking for opportunities in the tech space. For example. Allianz Technology Trust (ATT) has stakes in some of the big names in the sector including Apple and Microsoft as well as lesser-known companies such as monitoring platform Datadog (DDOG:NASDAQ) and data storage group Seagate (STX:NASDAQ).

DISCLAIMER: The author (Steven Frazer) owns shares in Allianz Technology Trust. The editor (Daniel Coatsworth) owns shares in iShares Global Infrastructure ETF.

* This article contains various fictional situations to provide an example of how someone might approach investing. It is not a personal recommendation. It is important to do your research and understand the risks before investing.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

Great Ideas

Investment Trusts

News

- Tesla and Microsoft give investors fresh reasons to fret

- Why boot brand Dr. Martens is walking tall by delivering growth

- Why the timing of Sandberg’s exit from Meta is terrible given severe challenges

- What the latest FTSE reshuffle means for the UK's leading shares

- Is it finally time to take a proper look at the Chinese market?