Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineInflation ahead!

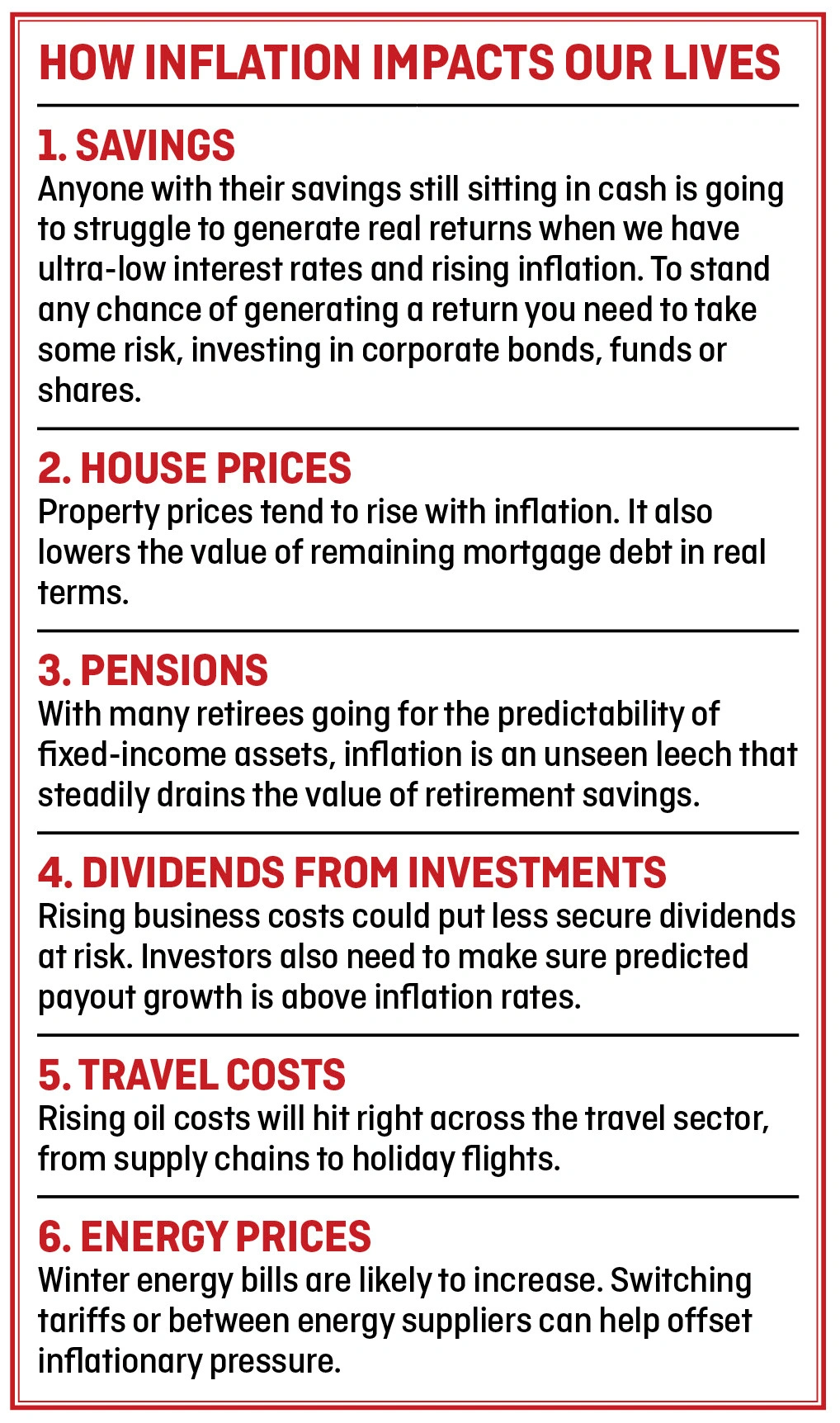

Everyday life is becoming more expensive as inflation rears its head for the first time in years. You must now look at your savings and investments to see if they can still deliver a positive return in real terms.

For example, if inflation goes up by 4% – as predicted on 2 November by NIESR (National Institute of Economic and Social Research) – then you need to make a minimum 4% return on your savings and investments just to protect the real value of your assets.

The situation is so important that a stark warning was issued last week by the Bank of England that inflation was about to accelerate in the UK. It predicts inflation will move from 1.3% this year to 2.7% in 2017 and 2018.

We now explain what inflation means for shares, funds, your pension as well as everyday costs of living. We also give suggestions for investments to beat inflationary pressures.

Stocks and funds to buy when inflation is rising

Investments suitable for an inflationary environment include commodity producers and real estate, in our opinion. They should protect your capital at worst, and grow the value of your money at best.

You should look for stocks that grow dividends at least in line with inflation such as utility companies National Grid (NG.) or SSE (SSE). A good fund for dividend growth is Perpetual Income & Growth (PLI).

Inflation-linked bonds may also appeal, although these are quite expensive to buy at present. You might find it easier to buy a fund or investment trust that already has a wide range of these bonds in its portfolio. A good example is Capital Gearing Trust (CGT).

We explain the different ways to buy gold as that has historically been a hedge against inflation. Our top gold mining pick is Centamin (CEY).

It is also worth backing companies with pricing power. This is the ability to pass on extra input costs to customers through higher selling prices and not see a massive deterioration in demand as a result of this action.

Investment fund Evenlode Income (GB00B42KPP53) has plenty of top quality stocks in its portfolio that have pricing power like Tampax tampon seller Procter & Gamble (PG:NYSE) and baby powder-to-medical devices giant Johnson & Johnson (JNJ:NYSE).

Why is inflation rising in the UK?

The slump in the pound as a result of the UK’s decision to leave the European Union has made imported goods much more expensive. Households are starting to feel a pinch; next year we’ll really see inflation hit our wallets.

UK inflation shot up in September this year to 1% versus 0.6% in August, according to the Office for National Statistics (ONS). The general consensus is that inflation will keep rising over the next year or two.

‘The direct impact of sterling’s depreciation on CPI inflation will ultimately prove temporary,’ says Mark Carney, governor of the Bank of England. ‘In the MPC’s (Monetary Policy Committee) judgement, attempting to offset it fully with tighter monetary policy would be excessively costly in terms of foregone output and employment growth.

‘The MPC is choosing a period of somewhat higher consumer price inflation in exchange for a more modest increase in unemployment.’

This is not entirely new territory. Peel Hunt economic strategist Ian Williams says there is a reasonably recent precedent for the Bank of England’s analysis in the shape of the 25% depreciation that sterling suffered during the 2007/08 financial crisis.

That was a contributory factor to an extended period of CPI inflation running ahead of target in subsequent years, he explains.

How inflation will hit your shopping bill

Your weekly shopping bill is likely to rise. Milk and petrol prices are going up faster than at any time during the past three years. Even making a cup of tea will be more pricey soon.

Popular consumer electronics look likely to follow with phones and laptops expected to become even more expensive. You may want to buy Christmas presents earlier than normal to beat any price hikes.

We are nervous about the retail sector if inflation remains elevated. Retailers may have to cut prices to stimulate sales – that would mean lower profit margins.

The only situation to make us reconsider this cautious stance would be an increase in wage inflation across the UK.

It is hard to predict if wages will go up, given that employers will also feel the pain of inflation. For example, software giant Microsoft (MSFT:NDQ) plans to raise prices by up to 22% for its online cloud services and push through price hikes for many of its software product lines. These actions will directly hit thousands of UK businesses.

Winners and losers in retail sector

General retailers can either pass inflation on to customers, take the hit in reduced margins or seek to mitigate the impact through the supply chain.

Structural winners are better placed to mitigate the impact than structurally-challenged operators, since the formers’ volume growth means suppliers will be willing to share the currency pain with them.

In a recent Peel Hunt note – ‘The impact of rising UK inflation’ – retail analysts John Stevenson and Jonathan Pritchard point out that the good shopkeepers tend to get stronger when conditions are tough.

Their key differentiators include ‘market leadership/pricing power, elasticity of demand and the ability to mitigate cost pressures, be that by finessing the product, or by simply having strong underlying volume growth anyway’.

High street clothing colossus Next (NXT) has said it it expects to push up prices in its core range by about 5% next year, though Associated British Foods’ (ABF) retail chain Primark has stated it won’t pass on the price hike to customers and will instead mitigate the impact or take the margin hit.

Among the winners identified by Peel Hunt are budget greetings cards seller Card Factory (CARD), whose vertical integration gives it scope to hold down prices and boost its value for money credentials in a category with low demand elasticity.

Possible losers include department store Debenhams (DEB), as rising rent and wage costs will compound its ability to mitigate another cost pressure.

Does the pound rebound mean inflation could go away?

The pound has staged a minor rally of about 3% in the past week or so. Key to this event has been the High Court ruling that Parliament must vote on when to start the Brexit process.

We believe investors should continue to expect inflation as the pound has a long way to go before it recovers lost territory. As such, we still believe inflation will push up the cost of living and is a major threat. Other market commentators are more optimistic.

‘While Carney will doubtless be relieved to see too much inflation rather than too little, he is now on alert for too high an overshoot (versus the Bank of England’s 2% target),’ says Russ Mould, investment director at share dealing specialist AJ Bell.

‘This suggests he may not be displeased by the rebound in the pound, which could help limit inflation and remove any need to consider an interest rate hike.’

Kallum Pickering, senior UK economist at investment bank Berenberg, believes the lower risk of a hard Brexit will take some of the downward pressure off the pound near-term.

‘If sterling appreciates a little over the coming months inflation may not rise as high next year as previously thought – a positive for real spending and near-term growth,’ he says.

What's going up?

Rebounding oil prices versus weak year-on-year comparatives are a big part of the latest CPI data, with housing, utilities and fuel, and transport worth 27% of the overall CPI basket of goods.

A 6%-plus jump between August and September in clothing prices was a major upside influence, but this is broadly in line with typical seasonal trends after prices fell earlier in the year, claims Ian Williams at stockbroker Peel Hunt.

The cost of staying in a hotel was another riser albeit against weak comparatives, while food prices had a deflationary impact.

‘Consumer food prices have been in a declining trend from their peak in 2014, reflecting prior sterling strength and the intensely competitive pricing environment in the food retail markets, as the hard discounters (Lidl and Aldi in particular) have taken a growing share of the market,’ explains Williams.

What inflation means for your pension.

Given super low interest rates, inflation is a double whammy for pensioners sitting on a large pile of cash in the bank.

A 2.7% rise in inflation versus a typical 0.7% interest rate on cash in the bank would mean the real value of your savings falls by 2% in a year. Your money wouldn’t buy you as much as it did in the past, so your standard of living could fall.

‘Rising inflation should act as a wake-up call to anyone who has used the pension freedoms to cash in their pension and stuck the money in a low or zero-interest paying bank account,’ explains AJ Bell senior analyst Tom Selby.

‘With interest rates unlikely to increase any time soon, such an investment strategy will guarantee their spending power will be eroded as inflation rises,’ he adds.

‘For people approaching retirement, the combination of rising inflation and low interest rates creates a difficult decision between an annuity or income drawdown.’ (SF, JC)

TIME TO BUY GOLD

Gold is traditionally seen as a hedge against inflation. It is generally considered to be an asset that holds its value in real terms in times of unease. You aren’t guaranteed to make a profit if inflation rises; but there is a good argument to warrant having it as part of a diversified portfolio.

You can get exposure to gold through various different ways.

1. Shares in gold miners.

The historical trend has been for gold miners to outperform a rising gold price. The higher the value of the metal, the more income a miner gets from selling its gold. Should the miner make an exploration discovery or exceed its production targets, then its share price is likely to get an additional kick upwards.

Gold miners with high levels debt could get a further boost as the market prices in a lower risk of defaulting on borrowings. Theoretically the miner would have greater profit margins by which to service repayments.

Our top pick: Centamin (CEY) at 165.1p

2. Gold mining funds

Funds and investment trusts are ideal for anyone who wants the upside of backing a gold miner but does not want to buy individual stocks. You can get exposure to multiple companies through a single product.

Our top pick: BlackRock Gold & General D Acc (GB00B5ZNJ896) at £11.98

3. Exchange-traded products

You can get a wide range of products that track the gold price. You should expect to pay a small annual charge circa 0.3% to 0.4% in exchange for a fund that moves in line with the value of gold.

Go for the ones that actually own gold bars rather than use derivative contracts to get exposure to gold. Look for the ‘physical’ name in the product description, not ‘synthetic’. If you invest £500, for example, the ETF provider would hold £500 worth of gold bars in a vault on your behalf.

Our top pick: Source Physical Gold P-ETC (SGLP) at £101.47

4. Physical coins and bars

If you want to buy physical gold, we would suggest going to a reputable dealer or using the services of the Royal Mint which has an online trading platform. You can get gold sent in the post or stored in one of the Royal Mint’s vaults.

5. Margin trading and covered Warrants

You can trade gold via derivatives such as spread betting, contracts for difference (CFDs) and covered warrants. Apart from the latter, there is a risk you can lose more than you initially invest. Covered warrants come with the risk of volatility which means you could see the value of the product temporarily fall even if gold rises.

We do not recommend you go down the margin trading or covered warrants route unless you are a sophisticated investor and fully understand the products and services. (DC)

WHAT HAPPENS IF THERE ISN’T SOARING INFLATION?

Expectations of future inflation are now firmly established in the UK but what if the price surge turns out to be lower than expected?

Even today, most forecasters say inflation in excess of 2% in the years ahead will be a temporary, rather than permanent, result of a weaker currency.

Asset manager Ruffer’s investment strategy is based on preparing for higher prices. It admits inflation in the UK is not a foregone conclusion in some economic and political scenarios.

Pay close attention to Europe

While the immediate impact of the UK’s vote to leave the EU is a weaker currency and inflation, this outcome could reverse if Europe itself starts to struggle.

‘We have always maintained that it is easy to bring about inflation when conditions, as they are today, are horribly deflationary,’ wrote Ruffer in an August commentary.

‘It does however mean a fundamental compromise of the currency – not something done lightly, but, like virtue, jettisoned advisedly when the alternatives are sufficiently unattractive. Expect the EU to pump liquidity – the mot du jour is “helicopter money” – into the system.

‘The place to look at the moment is what is happening in Italy, and, in particular, the Italian banks, which are being bailed out in a way which will be the first of many such instances. The markets will turn on such behaviour, sooner or later – and when that happens, the euro will prove very remarkably weak.

‘Alas, when the euro is weak, expect sterling to lose its competitive advantage as it strengthens. The tensions in the financial system are every bit as worrisome as those in the political arena, and it might just be that the lasting legacy of Brexit is financial turmoil – not political.’

Ruffer runs open-ended funds as well as Ruffer Investment Company (RICA), a listed investment company which trades at a slight premium to net asset value. The fund’s main investments are inflation-linked government bonds and Japanese bank stocks.

Pay close attention to commodity prices

Other factors which could UK stop inflation dead in its tracks are weaker commodity prices. For example, oil prices have gained from February lows of $27 per barrel but there remains potential downside if key producers fail to agree on output curbs.

A decline from today’s $44 a barrel would apply similar deflationary pressure to the UK economy as it did over the past two years when consumer prices turned negative in November 2015.

Inflation in the years ahead also assumes sterling stays weak for the entire period. While this is possible, there is upside potential to sterling if the economy performs better than expected, if interest rates are forced higher or if the UK’s trade deficit improves, among other potential outcomes. (WC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.