Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineShould trusts sell assets to fund dividends?

Investment trusts are starting to embrace a technique to ensure shareholders receive dividends every year or enjoy a better yield than in the past. It’s caused some controversy in the market and could become a hot topic over the coming months.

The strategy involves selling little chunks of an investment portfolio to fund dividends. The technical description is paying dividends out of capital.

The term capital refers to assets in the investment trust including underlying holdings and proceeds derived from selling assets.

JP Morgan Global Growth & Income (JPGI) has just adopted this new dividend technique; and International Biotechnology Trust (IBT) will soon do the same.

Eating your investments

Historically investment trusts have relied on income from underlying assets to fund dividends. They’ve also been able to keep 15% of income each year in a rainy day fund to pay dividends in more difficult market conditions.

Dipping into capital is allowed, so trusts aren’t doing anything wrong going down that route. However, it is essentially like pinching bits off a cake where eventually there would be nothing left on the plate.

Why is paying dividends out of capital ‘controversial’?

At the most extreme, it implies dividends are unsustainable unless there is always an increase in the value of the trust’s capital every year.

The market has been nervous for some time about the ability of specific individual companies to sustain their dividend payments including BP (BP.), Royal Dutch Shell (RDSB) and GlaxoSmithKIine (GSK) due to cash flow pressures.

Imagine if the broader investment community started fretting about funds’ ability to pay dividends.

Where to find information on how dividends are funded

With this in mind, investors should look closer than before at financial accounts to see where investment trusts obtain money to fund dividends, says James de Sausmarez, head of investment trusts at Henderson Global Investors.

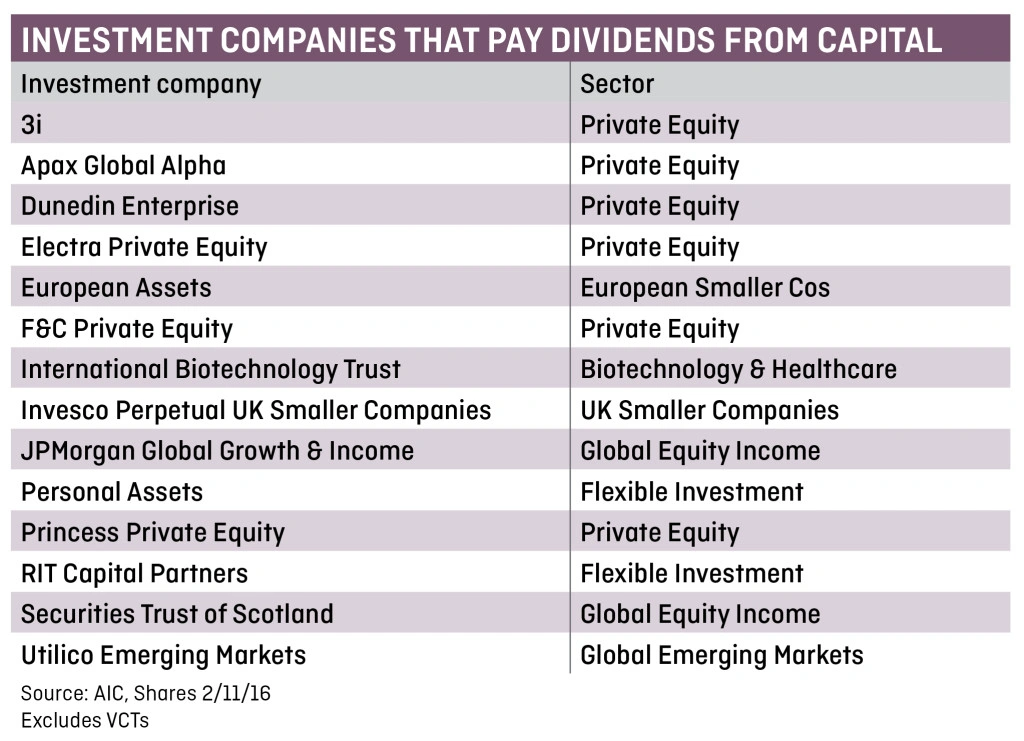

He says industry body The Association of Investment Companies (AIC) has been encouraging trusts to explicitly state the split of dividends from income or capital, in order to help investors.

How many trusts have gone down this route?

UK-domiciled trusts were first allowed four years ago to use capital to fund dividends but only a handful of trusts have so far adopted the more flexible dividend policy.

We believe there could be a step change in the market over the coming months as it becomes harder to get a decent yield from the market.

Investment trusts may find themselves having to use different methods to top up dividend payments including capital. They may increase the use of gearing where they borrow money to make more investments, thereby having a greater asset base from which to derive income to fund dividends.

It is also worth considering that dividends are a good selling point for investment trusts looking to attract new customers.

Having a (relatively) new way by which to pay dividends could encourage more investment trusts to use capital in order to make them look more attractive.

Our view on the matter

We’ve got an open mind towards paying dividends out of capital. You need to look at the make-up of each investment trust and their stated investment strategy.

Some fund managers say dividends should only be paid from income; and capital should be restricted to investments.

However, some investment trusts hold assets that aren’t necessarily big dividend payers and so they may not generate a big income.

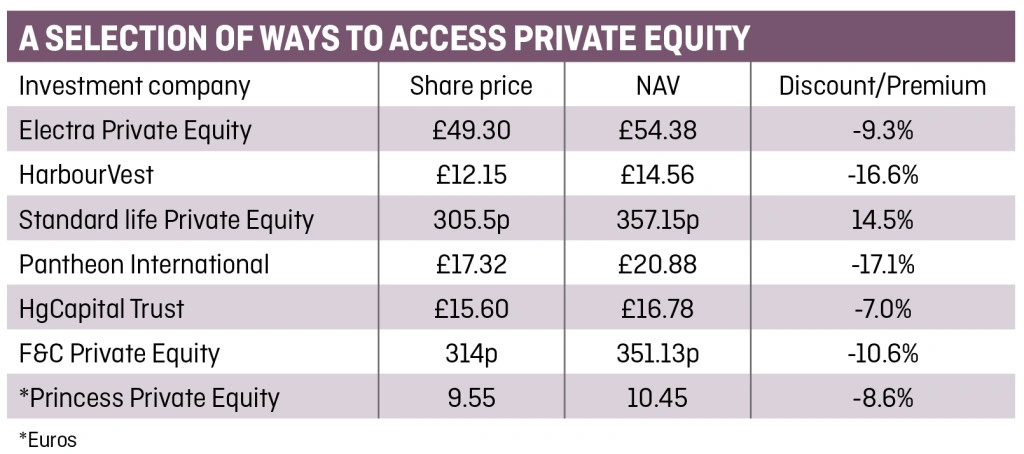

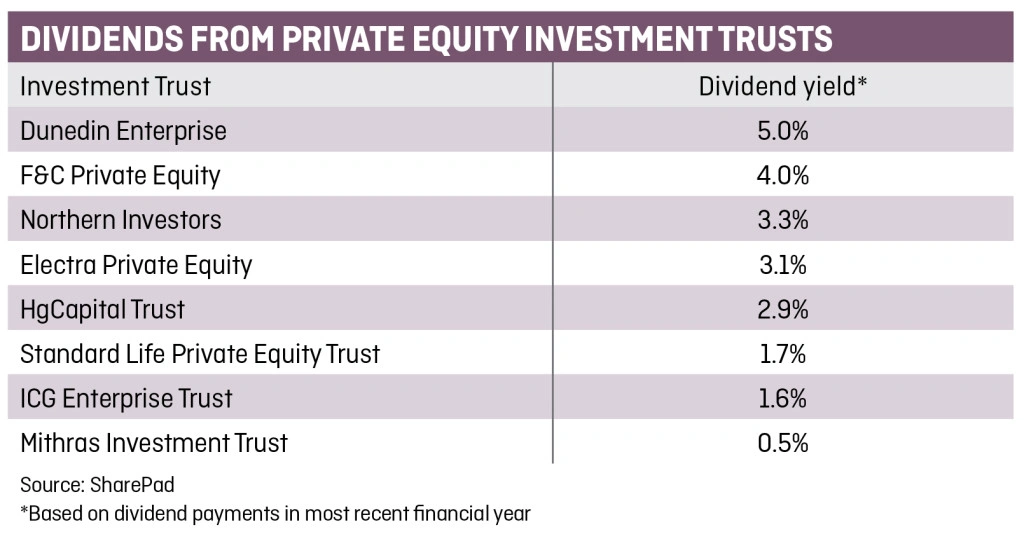

The biggest group of trusts that already pay dividends out of capital is private equity. That makes sense as most of their underlying assets won’t be paying dividends. The trusts realistically have no choice but to fund payments to shareholders out of capital.

As a counter argument, you could suggest that investment trusts that don’t have underlying income shouldn’t be paying dividends in the first place.

What the experts think

Investment trust analysts at financial services group Winterflood have voiced reservations about International Biotechnology Trust’s plan to use capital to help fund dividends.

However, their concerns are only related to that specific trust. They say biotech is a volatile asset class so there is a risk of selling investments to funds dividends at the point when share prices are weak, thereby significantly reducing the opportunity for long

term returns.

Overall, Winterflood’s analysts say the capital policy could be beneficial in certain cases. ‘We do not believe the practice is necessarily a good thing in all circumstances but given the voracious demand for income in the current low interest rate environment, it would seem like a sensible option for some funds.

‘In particular we believe it is beneficial as a tool for smoothing out dividends, in the same way that revenue reserves have traditionally been used,’ adds Winterflood.

‘For example, where a fund expects a shortfall in revenue for a certain period or where revenue is expected to ramp up and capital can be used to increase dividends immediately. In addition, we believe that using a small amount of capital to boost a dividend to an attractive level can also be positive.’

Putting the policy into practice

Securities Trust of Scotland (STS) recently adopted the capital funding policy to boost its dividend. Chairman Rachel Beagles said it was one of the factors that enabled an 18% hike in its shareholder payout during its past financial year.

‘Many pensioners are now taking more control of their income in retirement, and one of our priorities as a board is to make Securities Trust of Scotland as attractive as possible to investors,’ says Beagles. ‘Currently yielding 3.7%, the trust offers a high level of income compared to many other savings products in this low rate environment.’

Personal Assets Trust (PNL) says it has always paid a dividend and never cut it, yet admits it has become hard to earn a decent income in the current environment. The 2013/2014 financial year was the first time it didn’t earn enough income from its portfolio to fund dividends, says executive director Robin Angus.

‘We had a choice: increase the dividend on the portfolio (investing in higher risk stocks) or use capital to help fund the dividend. We felt capital was the most conservative option for us, in line with how the investment trust is run.’

Angus says the trust has pledged to pay back all money taken from capital for dividends as soon as it is possible in the future.

Saying ‘no’ to the capital route

Another conservatively-run investment trust has shunned the capital route, saying it is not in shareholders’ best interests. Ruffer Investment Company (RICA) warned in its 2016 annual report it may have to cut its dividend over the following 12 months as income had fallen below the level of dividend distributions.

JP Morgan Global Growth & Income’s shareholders last week approved changes to the way it pays dividends, to include money from capital. JP Morgan’s head of investment trusts Simon Crinage says this is part of a broader change for the product that used to be called JPMorgan Overseas Investment Trust.

‘The fund manager won’t change the way the trust is run. But the dividend has been set differently by the board,’ he explains. ‘The trust will endeavour to pay dividends equal to 4% of net asset value (NAV) at the start of the year, with distributions every quarter.’

Crinage says investors shouldn’t view this as a progressive dividend as the amount of money paid to shareholders could fall if there is a decline in NAV. ‘In a stock market downturn, it would pay 4% on the reduced net asset value figure.’

The dividend change went down well with retail shareholders, says Crinage. He notes the trust’s discount to NAV has also narrowed since the strategy announcement, implying positive market interest.

Second nature for one product

F&C-run European Assets Trust (EAT) has used capital to help fund dividends for more than 15 years. It falls under different rules to UK-domiciled investment trusts because it is Dutch-domiciled.

‘In the UK, there are two distinct pots for accounting purposes – one for revenue, one for capital,’ says Simon Cordery, head of investor relations and business development for investment trusts at F&C. ‘For us, there is only one pot under Dutch laws so we have been able to distribute from capital for a long time.’

He says the trust’s investors are fully aware of how the product works, adding that some people actually chose not to invest in European Assets because of its dividend process.

‘The trust focuses on small and medium-sized companies. Smaller companies aren’t really an income asset class, but over the long term they can outperform larger companies. Over the market cycle, if you are getting better total return, a trust can still pay out a bit to shareholders from capital as dividends and still deliver both capital growth and income.’ (DC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.