Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy Acacia Mining should merge with Endeavour

The potential merger between Acacia Mining (ACA) and Toronto-listed Endeavour Mining (EDV:TSX) looks positive in our view.

Although still at the discussion stage and lacking information on deal structure, we do believe a combined business would be highly attractive to any investor seeking a mid-cap gold producer with multiple projects.

‘Endeavour has near-term growth; Acacia adds stable production and exploration upside,’ summarises investment bank Canaccord Genuity.

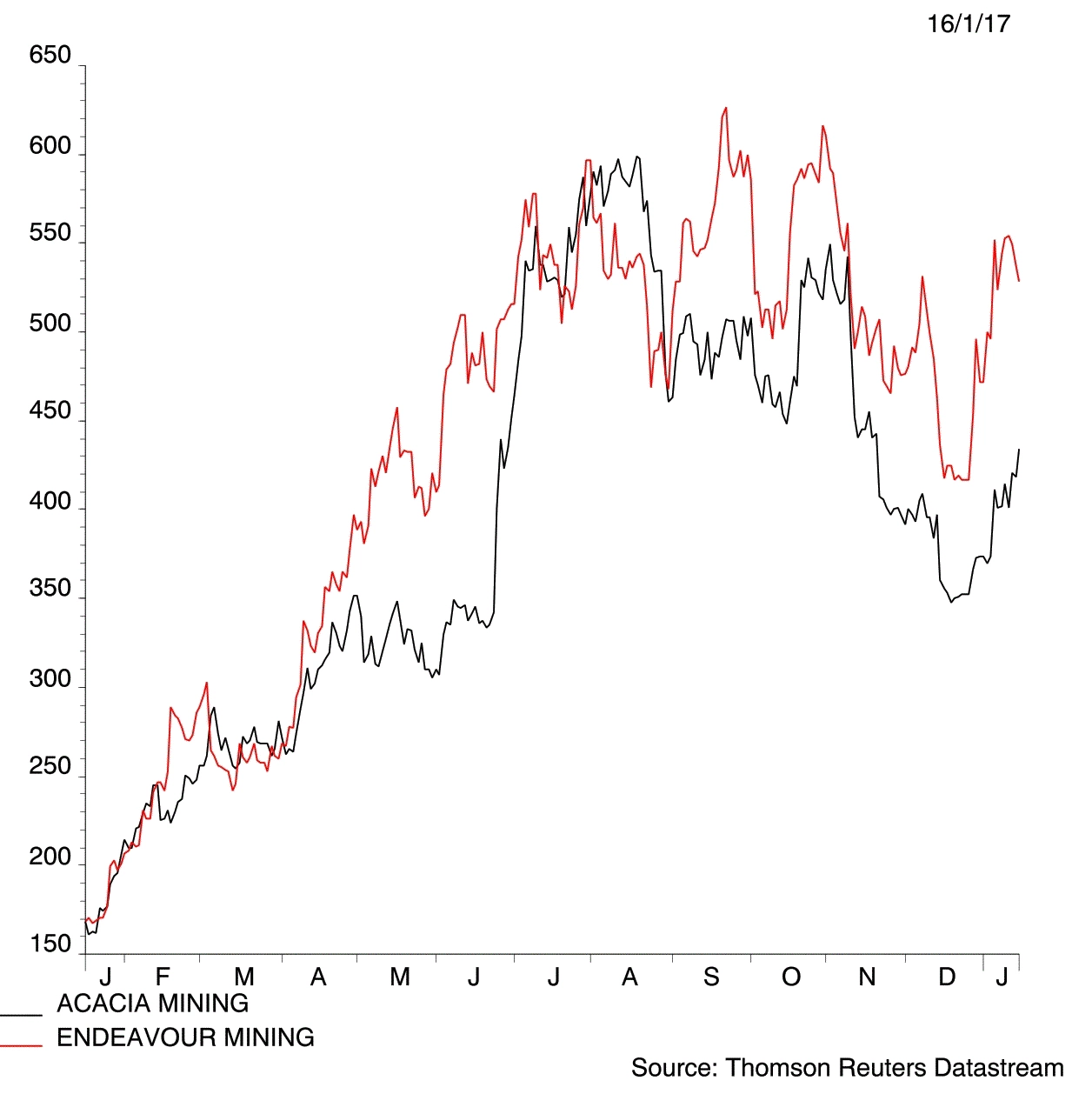

Market applauds the news

Acacia confirmed rumours last weekend that it is talking to Endeavour over a potential merger. Its share price jumped 4.2% to 435.92p on 16 January, the first chance for the market to react to the news.

The gold miners have a combined market value of £3.1bn. That would make the enlarged business the ninth biggest miner on the London stock market, overtaking copper producer KAZ Minerals (KAZ) and iron ore-to-aluminium miner Vedanta Resources (VED) in size.

A deal could also see the combined Acacia/Endeavour valued nearly as much as Russian gold and silver producer Polymetal (POLY). That’s assuming it chooses London as the listing venue for the enlarged business, as we’d largely expect.

Getting rid of share overhang

One of the immediate benefits to an Acacia/Endeavour corporate merger could be the removal of a long-standing share overhang.

Acacia was spun out of miner Barrick Gold (ABX:TSX) in 2010 under the name of African Barrick Gold. The parent company has since been very vocal about wanting to find a buyer for its remaining 64% stake in the business, now called Acacia.

Chinese state-owned miner China National Gold tried and failed to buy Acacia four years ago. Talks collapsed in January 2013 after neither side were able to agree on a suitable valuation.

Rumours then went round the City in 2016 that Barrick had been talking to several South African miners about selling its investment in Acacia.

Four ways for the miners to join hands

Peel Hunt analyst Michael Stoner believes there could be four possible scenarios in terms of deal structure.

1. Merger of equals. Barrick would therefore own 32% of the combined group. That stake could then be placed with institutional investors far more easily than the current 64% stake.

‘Paper in the combined group will be more liquid so Barrick can more easily trade out,’ says Stoner. ‘This is our preferred option which stands to preserve the most value for both sets of shareholders. In making a deal mutually beneficial to both parties it is far more likely to be sanctioned by the market.’

2. Acacia bids for Endeavour with an all-share or cash and shares offer – another way to dilute Barrick’s position.

3. Endeavour bids for Acacia by raising some money in the market and getting the Sawiris family to buy Barrick’s 64% stake. The Egyptian family have a natural resource investment vehicle called La Mancha which owns 30% of Endeavour.

4. Endeavour bids for part of the Barrick stake to become a minority shareholder in Acacia. ‘Barrick could then place out the balance of its position,’ says Stoner. ‘This seems the least likely option as Endeavour would not gain any operating control in this scheme.’

What would the enlarged company look like?

A combined Acacia and Endeavour would essentially have a portfolio of mines roughly balanced between East and West Africa.

Acacia has three gold mines in Tanzania and exploration projects in Burkina Faso, Mali and East Africa.

Endeavour has five producing mines and another set to begin operating this year.

Investment bank Jefferies says production could hit 1.7m ounces of gold in 2018 at an all-in sustaining cost (AISC) of $830 per ounce. That’s a favourable cost for the gold industry and represents all the costs associated with extraction and keeping mines operational.

Acacia/Endeavour’s projected AISC also implies decent profit margins against the current gold price of $1,200 per ounce.

Downside to endeavour

Stoner at Peel Hunt says Endeavor’s weakness is having relatively short mine lives versus Acacia and other London-quoted miners such as Centamin (CEY). He believes Acacia’s long life Bulyanhulu mine would be the core focus of an enlarged group.

Acacia had $203m net cash as of 30 September 2016. In comparison, Endeavour had $14m net debt. Putting the two companies together would theoretically mean Acacia’s strong balance sheet could help to finance some of Endeavour’s development plans.

Endeavour had $580m funding requirements as of the end of the third quarter of 2016. Approximately $271m is needed for remaining project costs on Hounde, a mine in Burkina Faso which should start to pour gold in the fourth quarter of 2017.

The miner also needs $306m for project costs to upgrade processing capabilities on its Ity mine in Cote d’Ivoire.

‘The assets, and management teams, would appear to complement one another,’ comments Canaccord. ‘In our view, on a qualitative basis, a deal would make sense; it all comes down to relative valuation and, as both companies have said, discussions may or may not result in agreement of a transaction.’ (DC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.