Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy now is the perfect time to buy BHP Billiton

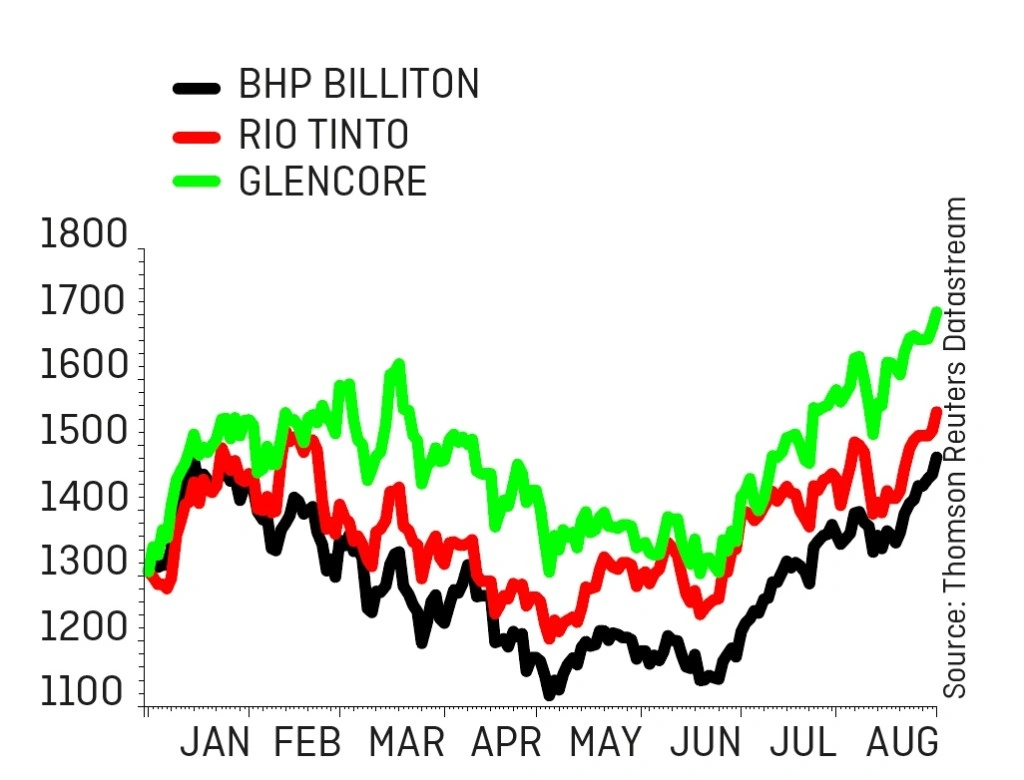

Despite all the publicity around an activist investor trying to shake up BHP Billiton (BLT), it is the worst performing stock among the FTSE 100 diversified miners this year.

That’s not to say shareholders have lost money; in fact a near-50% share price gain actually makes BHP the eighth best performing stock in the FTSE 100.

We think there is merit in owning the shares on a long-term basis. Many analysts are also positive on the stock, judging by several bullish research notes since its full year results on 22 August.

Why is BHP back in favour?

The financial results contained a few positive surprises. Investors didn’t seem to mind its post-tax profit was 5% below expectations. Instead, they focused on other factors including a better than expected net debt at $16.3bn versus $18bn forecast by analysts.

The market was relieved that BHP said it would delay a production decision on the very large Jansen potash project. There is growing speculation that BHP may now sell part of its stake in Jansen.

Also deemed good news was BHP’s confirmation that it would put its onshore US shale oil and gas assets up for sale. Investment bank Investec values those assets at $5.1bn.

What does that mean for investors?

Lower debt and potential cash injection from asset sales bodes well for future returns for shareholders, be it via dividends or share buybacks.

They would enhance an already-strong situation where BHP enjoys high profit margins from low-cost assets, delivering strong cash flow that can be reinvested in the business and be used for dividends.

We note with interest that BHP’s large net debt position is forecast to be eliminated within the next three years. UBS forecasts it will go from a peak of $26.1bn in June 2016 to a net cash position of $343m in June 2020, rising to £7.8bn net cash a year later.

The cash generation strength is evident in the bank’s forecasts which include a 10.7% free cash flow yield this year, progressing to 13.9% on 2021’s estimates. A figure above 10% is generally deemed to be very attractive. Free cash flow is the amount of cash generated from operations minus capital expenditure.

On paper BHP looks to be an attractive investment opportunity. The key risk to consider is that commodity prices are impossible to accurately predict. Financial models can produce wildly different results depending on commodity price assumptions.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.