Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineContrarian calls from two canny trusts

Contrarian investors look for companies whose potential for share price growth or recovery has been overlooked by the market. This style requires nerves of steel; humans have evolved to like to belong to a group or feel a part of something bigger, so taking a contrarian stance is uncomfortable and you have to be patient as the investment case unfolds.

For this reason it can be better to adopt a contrarian approach through an experienced fund manager.

The Scottish goes shopping

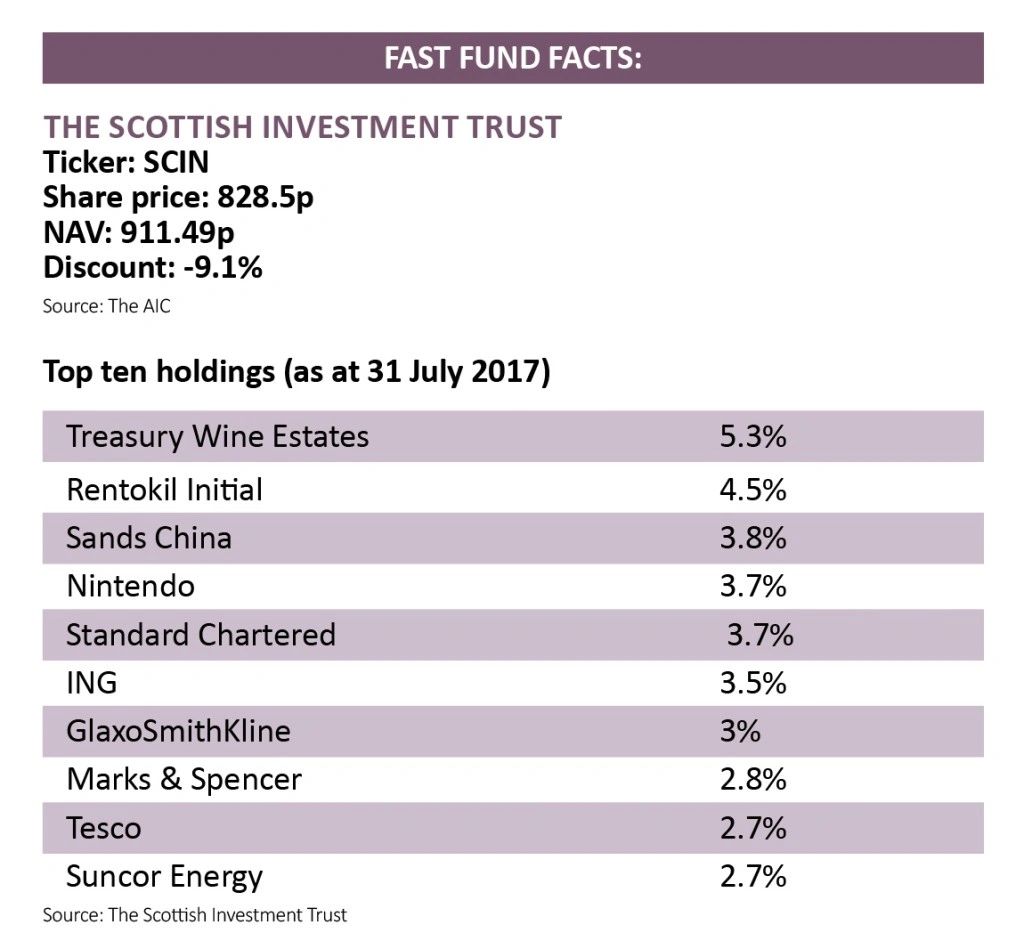

One well-established fund with a contrarian approach is The Scottish Investment Trust (SCIN), currently trading at a 9.1% discount to net asset value.

Investing globally with the aim of achieving capital appreciation and inflation-beating dividend growth, the trust’s four-strong management team led by Alasdair McKinnon uses behavioural finance techniques to exploit investors’ tendency to ‘follow the crowd’. By focusing on stocks that are very unloved, those with operational improvements that have been overlooked, and more popular stocks that can continue to do better, the managers build in a margin of safety.

McKinnon has made two contrarian calls in the unloved retail sector, where headwinds include falling consumer spending, rising costs from sterling’s weakness, a potentially reduced supply of workers post-Brexit and the impact of rapid structural change.

‘E-commerce is putting margins under pressure, and many retailers are finding that much of their floor space is redundant,’ says McKinnon. ‘And many traditional high-street stalwarts are coming under fire from discount chains. We shouldn’t be surprised, then, that many investors prefer to look elsewhere.’

The Scottish Investment Trust doesn’t see this as the right approach. ‘We’re contrarian to our core and believe that the best opportunities arise when the market overreacts. It’s then that the “wisdom of the crowd” gives way to herd instinct and groupthink.’ McKinnon believes investors are overlooking the potential for the Bank of England and the government to take some of the pressure off consumers.

The astute stockpicker adds ‘it is also possible that the Brexit negotiations will be smoother than expected. Despite all noise from both sides, a pragmatic approach may well prevail once the process is in full swing. Similarly, we think that concerns about the UK consumer may be overcooked.

‘Consumer spending could be curbed by some of the potential Brexit outcomes. But so far, consumers have been carrying on as normal. Following the Bank of England’s interest-rate cut last summer, cheaper mortgages and loans have encouraged consumers to borrow and spend. With interest rates likely to remain low, the combination of low unemployment and higher wages would help to keep the retail sector on a steady footing as it faces up to its structural challenges.’

McKinnon sees ‘the most current opportunities in UK retail as “ugly ducklings” – unloved shares that most investors shun. Because their operating performance has been poor for some time, their shares are very much out of favour. But we see potential for them to defy the market’s expectations and turn their circumstances around. And while we wait for our ugly ducklings to become swans, most of them offer higher-than-average dividend yields.’

Marks & Spencer (MKS) ‘is a classic “ugly duckling”. Its clothing division has been struggling for some time. But under CEO Steve Rowe, it has begun to turn things round through a better pricing strategy. Meanwhile, the company’s food division is still market leading, and its investments in IT and infrastructure are creating a multi-channel offering that can succeed in today’s digital environment. And while we wait for its shares to reflect this, Marks & Spencer offers a sustainable dividend yield of 5.5% – and 7% with this year’s special dividend.’

‘Another “ugly duckling” is Tesco (TSCO), where CEO Dave Lewis is aiming to rebuild profitability, restore market share and regain the trust of consumers and investors. And he is making positive progress. Lewis is focusing on growth in the core UK business and has sold off peripheral assets at home and abroad.’ The acquisition of food wholesaler Booker is designed to secure Tesco’s position as the UK’s largest food business, better pricing and an enhanced customer offering have led to improved same-store sales. ‘Meanwhile, a £1.5bn cost-cutting programme should support margins, which are currently the lowest among UK supermarkets,’ adds McKinnon.

Alex Wright, manager of Fidelity Special Values

The Wright stuff

Alex Wright, manager of Fidelity Special Values (FSV) , follows a value-contrarian philosophy centred around buying unloved companies in out of favour sectors and holding them until their potential value is recognised by the wider market. Wright invests in companies with exceptionally cheap valuations or some kind of asset that should prevent the share price dropping below a certain level, such as inventory or intellectual property, which gives him a margin of safety.

Like McKinnon, Wright is willing to put money to work in sectors that divide opinion among investors and has increased the trust’s allocation to banks with the addition of two new ideas. As Matthew Jennings, investment director for UK equities, Fidelity International, explains:

‘While IPOs do not usually meet our contrarian criteria, the recent IPO of Allied Irish Banks (AIB) is something of an exception. AIB and Bank of Ireland (BoI) have around 60% combined market share each in the Republic of Ireland, creating a very attractive industry structure in an economy which has seen a strong recovery and could outperform other European economies for years to come. However, unlike BoI, AIB has a low quality loan book - around 16% in bad loans compared to 5% at BoI. This makes the market wary of the company, and undoubtedly makes it more exposed to the macroeconomic situation in Ireland.’

The positive news is the bank ‘is extremely well capitalised, with a 16% Core Tier 1 Ratio, which gives it a good deal of protection against further write-downs. If management is able to continue reducing the bank’s exposure to bad loans, it will free up large amounts of capital for distribution to shareholders.’

Another new position for Fidelity Special Values is Royal Bank of Scotland (RBS). ‘Up until now, Alex has avoided RBS in preference of other banks where the recovery is more advanced,’ says Jennings. ‘However, an attractive balance of risk and reward is now emerging.

There is considerable uncertainty hanging over the company as it awaits a decision from the US Department of Justice regarding the size of the fine RBS faces, meaning most investors have preferred to invest in banks with fewer uncertainties.

If the fine is at the upper end of expectations, RBS remains well capitalised - if it is at the lower end, it is very well capitalised, and in a strong position to begin the process of capital distribution to shareholders and resume dividend payments.

RBS has been thorough and arduous process of portfolio restructuring and investment bank downsizing, but we are now beginning to glimpse the light at the end of the tunnel.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.