Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineGo under the radar with investment trusts

Investors tend to flock to the most popular options when it comes to choosing investment funds and trusts. This herd mentality means many people are missing out on some first-class investments simply because they are under the radar.

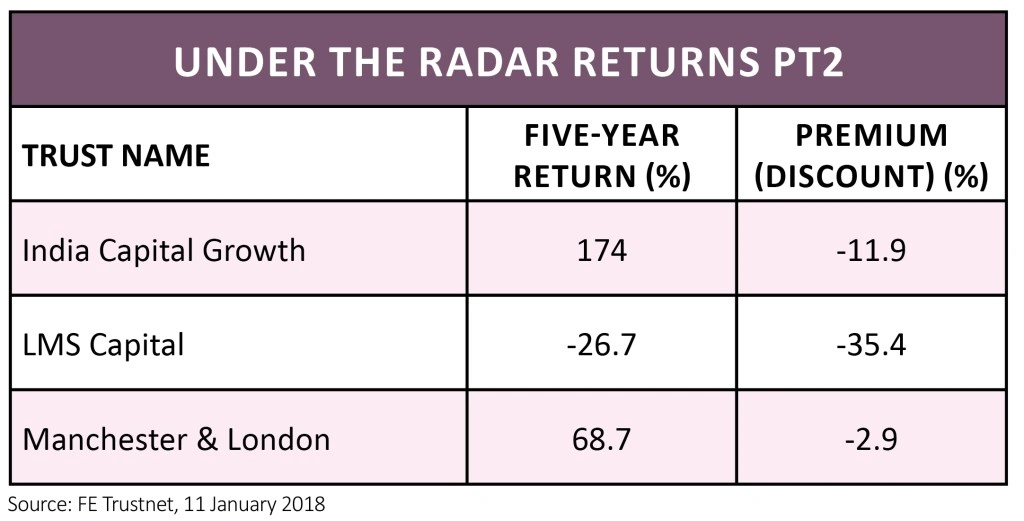

But seeking out these lesser-known names could provide a serious boost to your returns; several investment trusts which would have tripled your money over the past five years are still trading on hefty discounts, managing relatively tiny amounts of investors’ cash compared to the behemoths of the sector.

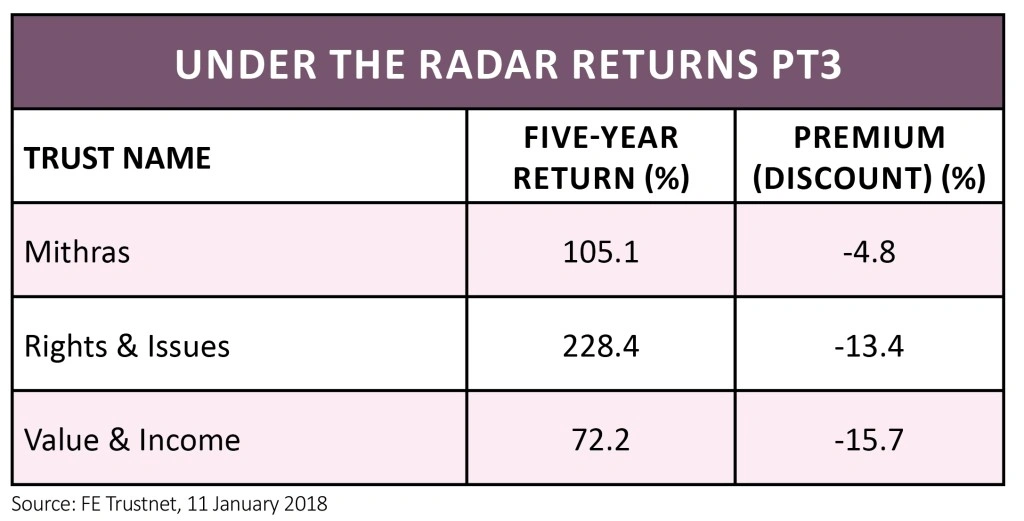

The Rights & Issues (RII) investment trust, for example, has delivered an impressive 228.4% over five years – it would have turned £10,000 into £32,840 in that time – yet trades on a discount of more than 13%.

NARROWING DISCOUNTS CAN BOOST RETURNS

Backing an investment while it’s still under the radar can enhance your return if the discount to net asset value narrows. If you buy at a discount of 10%, for example, and it moves to trade at par, even if the trust delivers no capital growth, you have still made a 10% profit as other investors are willing to pay more for the shares than you did.

But buying a lesser-known trust can be risky, too. Investments with fewer assets can be more difficult to buy and sell, and you could find yourself stuck in a trust you want to get out of, or suffering if the discount falls even further. Yet with the right research, experts say there are gems to be found.

Investors in the India Capital Growth (ICG) trust would have seen a 174% return on their money over the past five years. Yet, despite such stellar performance, the trust still trades at a discount of 11.9% and has assets of little more than £100m.

India has become an increasingly popular emerging market investment choice in recent years as structural reforms and a growing middle class in the country have driven its economy forward. David Cornell, chief investment officer at Ocean Dial, says: ‘Everything in India is growing but it’s about finding well-managed companies which are run by honest people and not just growth for growth’s sake.’

He backs businesses which protect their balance sheet and look after their shareholders’ interests. The trust’s largest holding is in mortgage finance company Dewan Housing.

Mortgage lending in India is currently only around 10% of its gross domestic product – in the UK it’s closer to 100% – but it has been growing steadily and default rates are low. ‘The cost of borrowing is coming down and that is stimulating demand. Dewan is not targeting the affluent but the emerging middle class,’ says Cornell.

INCREASING APPEAL OF INDIA

Innes Urquhart, research analyst at Winterflood Securities, says the trust’s focus on small and mid-cap companies differentiates it from its rivals. But while the trust’s total return has outperformed its peers he points out that subscription share issues have had a dilutive effect on its net asset value, which has grown just 148.1% over five years. Urquhart adds: ‘The trust is now of a size where it may appeal to a broader range of potential investors and this could lead to a further narrowing of the discount.’ It has already narrowed from 20% in August 2017.

Managing director of the Independent Investment Trust (IIT) Max Ward says last year was ‘a wonderful year for stock pickers’. The ‘global’ trust has some 88% of its assets in the UK where Ward says the best opportunities are to be found in the small and mid-cap space. Standout holdings in the portfolio include Blue Prism (PRSM:AIM), which designs and rents software robots.

The firm has seen its share price grow from just 78p when it floated in 2016 to an incredible £12.60 today. ‘We think this market is absolutely in its infancy; it is one of the best companies in its industry and could grow at a rapid rate for some time to come,’ says Ward.

The trust has returned an impressive 249.1% over the past five years but Ward says he never feels confident. After such a strong year with so few companies producing disappointing results he is concerned that 2018 could bring a reversal in fortunes.

Certainly, a concentrated portfolio with significant exposure to technology and smaller companies could bring volatility, points out Urquhart. But he likes that board of the trust has significant ‘skin in the game’ and that it is one of the lowest cost investment trusts available with an ongoing charge of just 0.34%.

FROM LITTLE ACORNS

Investors who put £1,000 into Acorn Income (AIF) when it launched in February 1999 would have more than £14,000 today if they had reinvested their income. The trust has delivered a return of 142.1% over the past five years – that’s despite its focus on UK smaller companies being a drag in the aftermath of the Brexit vote.

Currently some 83% of the portfolio is held in smaller businesses; Nigel Sidebottom, head of closed-end funds at Premier Asset Management says that despite Brexit uncertainties there are still a wealth of opportunities in this part of the market; just 11% of its assets are currently in fixed income investments.

Acorn has no more than 50 holdings at a time and Sidebottom says these are chosen based on in-depth knowledge of each company. Top holdings include cosmetics company Warpaint London (W7L:AIM), tech firm Discoverie (DSCV), and packaging business Macfarlane (MACF). Such is Sidebottom’s conviction that there are several investment opportunities that in December the trust received shareholder approval to issue new shares up to 20% of its existing capital.

Charles Cade, research analyst at Numis Securities, says: ‘Acorn Income has an impressive, long-term track record. Manager Paul Smith has an opportunistic approach that seeks to exploit short-term trading opportunities and invest in specialist, less widely followed securities that can be mispriced.’

Gearing of 40% means the trust is likely to perform well in rising markets, but could suffer if there is a stock market set back this year. Although Cade points out that a focus on high quality companies and an allocation to fixed interest helps mitigate this.

BEST THINGS DO NOT ALWAYS COME IN SMALL PACKAGES

But small is not always beautiful. LMS Capital (LMS) invests in small, private UK companies such as software business Entuity and marketing firm Elateral. Yet, while the average investment trust in the private equity sector has delivered a return of 75.9% over the past five years, LMS Capital is down 26.7% over that period.

Such underperformance saw a new external manager – Gresham House – appointed in August 2016, which has implemented a restructuring plan including a review of the trust’s assets, cost savings and appointing a new investment committee. The trust trades at a discount of 35%.

Cade says the trust has had a ‘difficult history’. He explains: ‘It had adopted a wind-up strategy, but in July 2016 put forward reconstruction proposals.’ While the new investment team and strategy have delivered capital back to investors, Cade still has some concerns: ‘There are still some legacy investments and 43.1% of the fund is held by the family of the previous manager.’

Gresham House chief executive Tony Dalwood says: ‘The new investment committee has initiated a process to revitalise the business and have delivered a return of capital ahead of our original plans.’ (HB)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Dollar hits three-year low

- Premier plays down Batchelors sale chatter

- Melrose launches GKN charm offensive

- The winners and losers from Carillion’s demise

- JD says profit will be better than expected

- Savills CEO steps down after nearly 40 years at firm

- Sting in the tail for BP on Deepwater Horizon oil spill

- Dividend downgrades for Card Factory