Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFour lessons to draw from 18¼ years of precisely zero from UK stocks

A potential takeover bid for a fourth FTSE 100 stock this year is helping the index to try to cling on to the 7,000 mark, as Takeda’s plan to consider an offer for drug manufacturer Shire (SHP) adds to the offers for GKN (GKN), Smurfit Kappa (SKG) and Sky (SKY).

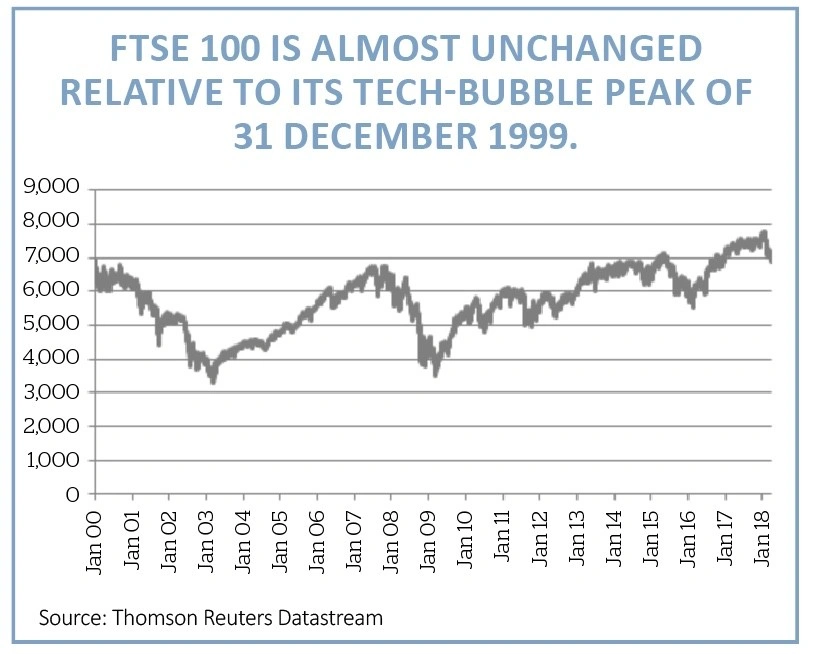

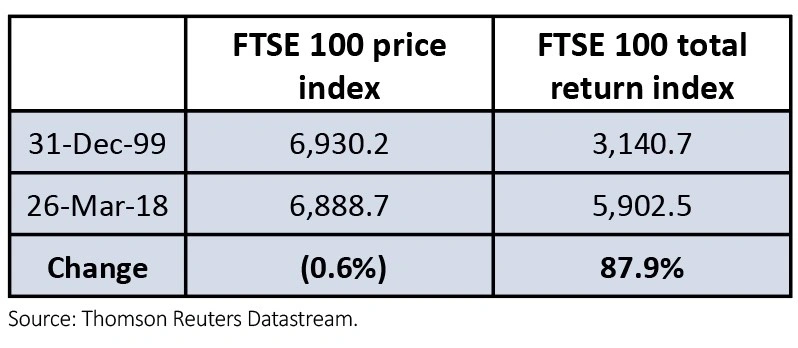

But that 7,000 mark is still awfully close to the 6,930.2 mark reached on 31 December 1999. At the time, the latter level represented a new all-time high for the FTSE 100 and turned out to be the very peak for the benchmark index, as air promptly started to leak out of the technology, media and telecoms (TMT) bubble.

Comparing that level to today’s position, the UK’s premier index has effectively gone nowhere for just over 18 years. At its year-to-date closing low on 26 March of 6,889 it had even contrived to record a small loss over that period.

For patient portfolio builders, that could make for depressing reading, but even in the face of such apparent adversity it is possible to draw four valuable lessons when it comes to portfolio construction and asset allocation.

1. The price paid for an investment really does matter

Since 31 December 1999 high of 6,930, the FTSE 100 has seen two bear markets (2001-03 and 2007-09) and two bull markets (2003-07 and 2009 onwards).

Having lost that peak, it took the benchmark until 2015 to reach it again and on 26 March 2018 it stood around half-a-percent below it at 6,889.

The message here is three-fold. At first glance, this makes ‘buy-and-hold’ strategies look a bit sick (but more of that in a moment).

Those investors who eschewed ‘buy-and-hold’ could have got into even worse trouble, if they did not resist the powerful temptation to be dragged in at the top (when all seems rosy) and flee at the bottom (when all seems bleak) which can be awfully hard to resist.

Those investors who did try to time the market therefore needed to heed Warren Buffett’s aphorism about being ‘fearful when others are greedy and greedy when others are fearful’.

When greed is dominant, valuations are likely to be bubbly and sitting at unsustainable levels. When fear is dominant, valuations are likely to be cheap and build in a margin of safety.

So the price paid for an investment really is a key determinant of the long-term return, where it is an index, fund or individual stock or bond.

2. Picking stocks can pay off (but it isn’t easy)

Another way to try and get around the poor headline capital return from the FTSE 100 would be to try and pick individual winning stocks and dodge the losers (or pay a fund manager to do it for you, if the time and research effort involved are simply too much).

The good news is this could have paid off handsomely. No fewer than 56 of the 100 firms that made up the FTSE 100 in 1999 recorded a better return than the broader index.

The bad news is that only 51 still survive to this day and of those only 32 have offered a positive capital return since the end of 1999.

And of the 100 firms in total, 22 fell by more than 50% and seven by more than 90%, inflicting real pain on any fund manager or investor who picked out those as the new millennium dawned.

In other words, spotting the winners (that either survived or were taken over for a fat price) was no easier than avoiding the disasters (that went broke, dished out profit warnings and share price collapses or were snapped up at lower prices following wider market declines).

PATIENCE CAN STILL BE REWARDED

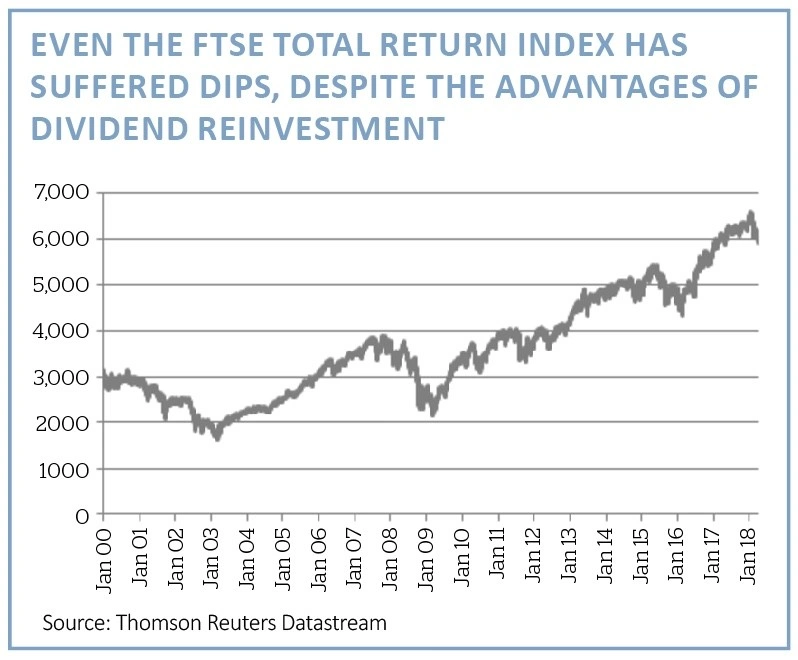

Thankfully patience can get its reward and it comes in the form of dividends. These precious payments mean that holding a passive index tracker can pay off, as can operating a buy-and-hold strategy (providing investors’ portfolios are capable to withstanding the ups and downs in capital values in between).

This can be demonstrated by looking at the performance in the FTSE 100 in purely capital returns and total return terms. In the latter case, dividends are harvested and then reinvested.

The difference is startling – but again, it must be remembered that even the total return index suffered two large falls during the 2001-03 and 2007-09 bear markets, even if they were not as pronounced as the declines in the headline index.

BEWARE HOME BIAS

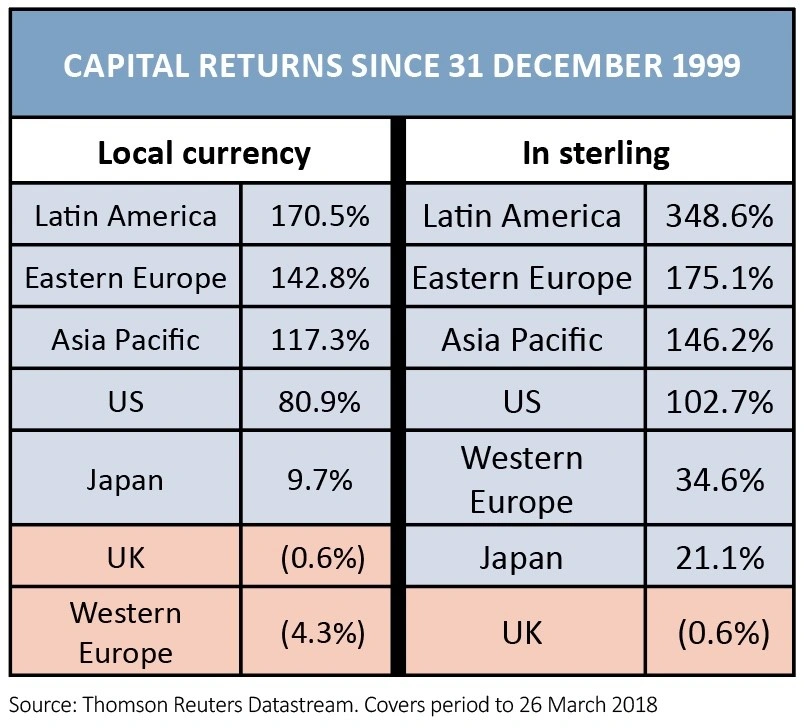

One way of getting around the UK’s disappointing headline performance since the end of the 1990s bull-run would have been to fight any natural home-leaning bias and diversify by looking overseas.

In capital terms the UK has lagged all major overseas geographies in local currencies.

A drop in the pound over the period has further boosted returns from overseas arenas (although none of these trends are guaranteed to repeat themselves in the future).

UK HAS DONE BADLY RELATIVE TO KEY OVERSEAS MARKETS SINCE THE END OF 1999

The UK’s generally superior dividend yield helps a little in total return terms but the showing relative to international options has still generally been poor.

UK HAS DONE BADLY RELATIVE TO KEY OVERSEAS MARKETS SINCE THE END OF 1999 EVEN ALLOWING FOR ITS SUPERIOR DIVIDEND YIELD

Russ Mould, investment director, AJ Bell

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.